Chapter 15: Investment and finance

This chapter should be cited as:

Kreibiehl, S., T. Yong Jung, S. Battiston, P. E. Carvajal, C. Clapp, D. Dasgupta, N. Dube, R. Jachnik, K. Morita, N. Samargandi, M. Williams, 2022: Investment and finance. In IPCC, 2022: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change[P.R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, J. Malley, (eds.)]. Cambridge University Press, Cambridge, UK and New York, NY, USA. doi: 10.1017/9781009157926.017

Executive Summary

Finance to reduce net greenhouse gas (GHG) emissions and enhance resilience to climate impacts represents a critical enabling factor for the low carbon transition. Fundamental inequities in access to finance as well as its terms and conditions, and countries’ exposure to physical impacts of climate change overall result in a worsening outlook for a global just transition (high confidence) . Decarbonising the economy requires global action to address fundamental economic inequities and overcome the climate investment trap that exists for many developing countries. For these countries the costs and risks of financing often represent a significant challenge for stakeholders at all levels. This challenge is exacerbated by these countries’ general economic vulnerability and indebtedness. The rising public fiscal costs of mitigation, and of adapting to climate shocks, are affecting many countries and worsening public indebtedness and country credit ratings at a time when there were already significant stresses on public finances. The COVID-19 pandemic has made these stresses worse and tightened public finances still further. Other major challenges for commercial climate finance include: the mismatch between capital and investment needs, 1 home bias 2 considerations, differences in risk perceptions for regions, as well as limited institutional capacity to ensure safeguards represent. {15.2, 15.6.3}

Investors, central banks, and financial regulators are driving increased awareness of climate risk. This increased awareness can support climate policy development and implementation (high confidence) . Climate-related financial risks arise from physical impacts of climate change (already relevant in the short term), and from a disorderly transition to a low-carbon economy. Awareness of these risks is increasing leading also to concerns about financial stability. Financial regulators and institutions have responded with multiple regulatory and voluntary initiatives by to assess and address these risks. Yet despite these initiatives, climate-related financial risks remain greatly underestimated by financial institutions and markets limiting the capital reallocation needed for the low-carbon transition. Moreover, risks relating to national and international inequity – which act as a barrier to the transformation – are not yet reflected in decisions by the financial community. Stronger steering by regulators and policy makers has the potential to close this gap. Despite the increasing attention of investors to climate change, there is limited evidence that this attention has directly impacted emission reductions. This leaves high uncertainty, both near-term (2021–30) and longer-term (2021–50), on the feasibility of an alignment of financial flows with the Paris Agreement ( high confidence). {15.2, 15.6}

Progress on the alignment of financial flows with low GHG emissions pathways remains slow. There is a climate financing gap which reflects a persistent misallocation of global capital (high confidence) . Persistently high levels of both public and private fossil-fuel related financing continue to be of major concern despite recent commitments. This reflects policy misalignment, the current perceived risk-return profile of fossil fuel-related investments, and political economy constraints ( high conf idence). {15.3}

Estimates of climate finance flows – which refers to local, national, or transnational financing from public, private,multilateral, bilateral and alternative sources, to support mitigation and adaptation actions addressing climate change – exhibit highly divergent patterns across regions and sectors and a slowing growth. {15.3}

When the perceived risks are too high the misallocation of abundant savings persists. Investors refrain from investing in infrastructure and industry in search of safer financial assets, even earning low or negative real returns. {15.2, 15.3}

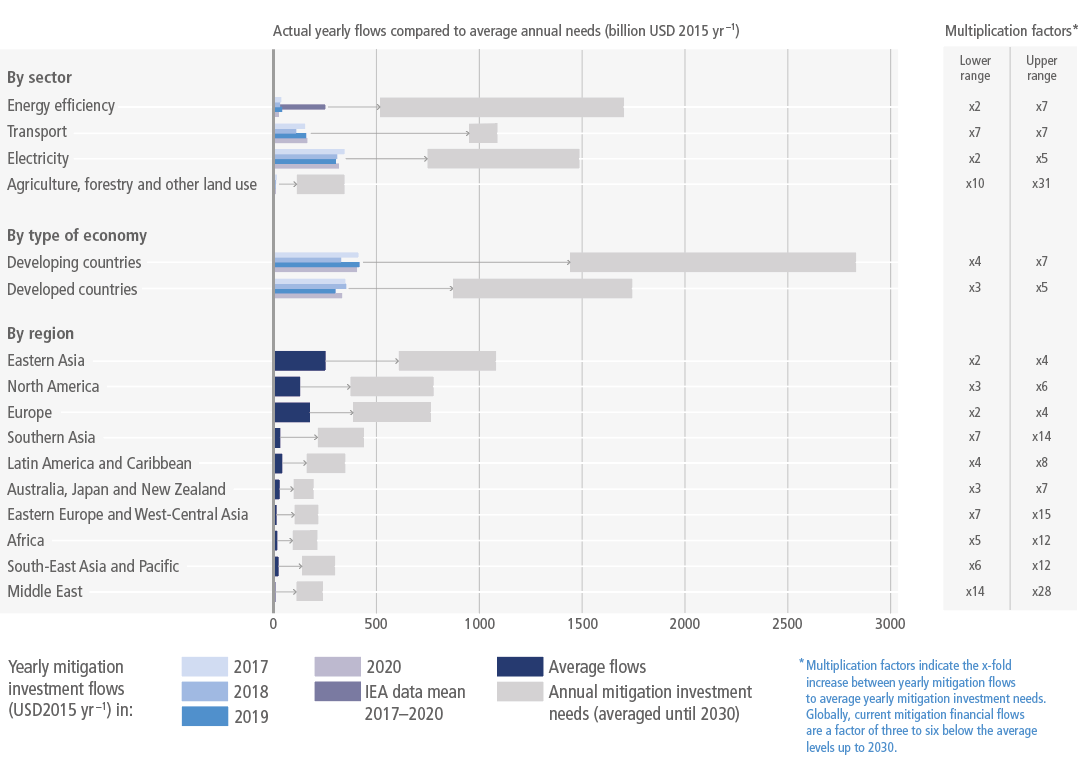

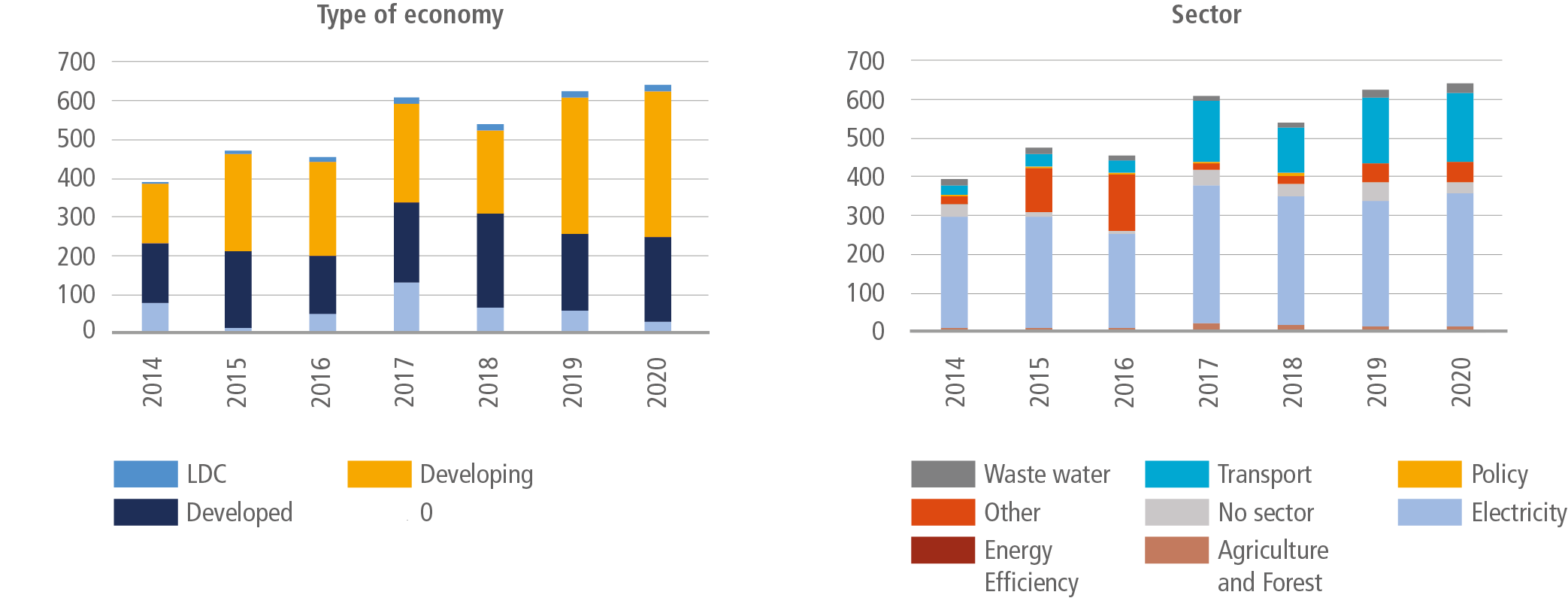

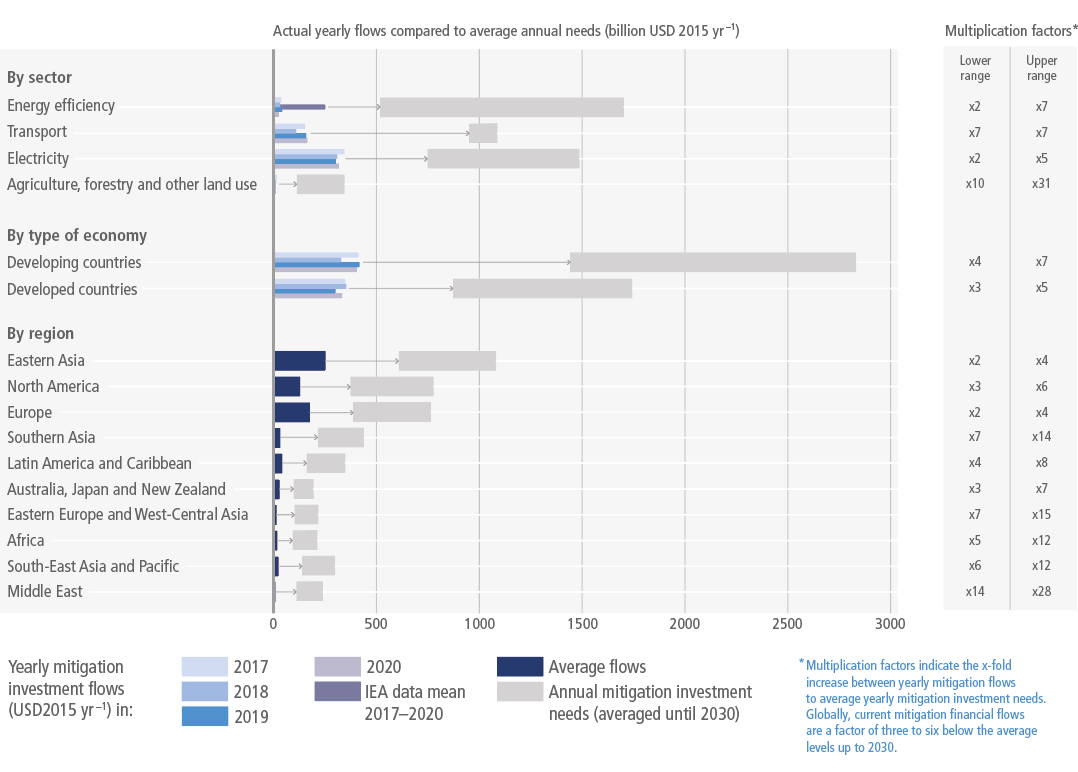

Global climate finance is heavily focused on mitigation (more than 90% on average between 2017–2020). This is despite the significant economic effects of climate change’s expected physical impacts, and the increasing awareness of these effects on financial stability. To meet the needs for rapid deployment of mitigation options, global mitigation investments are expected to need to increase by the factor of 3 to 6 (medium confidence). The gaps are wide for all sectors and represent a major challenge for developing countries, 3 especially Least-Developed Countries (LDCs), where flows have to increase by factor 4 to 7, for specific sectors like agriculture, forestry and other land use (AFOLU) in relative terms, and for specific groups with limited access to, and high costs of, climate finance ( high confidence). {15.4, 15.5}

The actual size of sectoral and regional climate financing gaps is only one component driving the magnitude of the challenge, with financial and economic viability, access to capital markets, investment requirements for adaptation, reduction of losses and damages, climate-responsive social protection, appropriate regulatory frameworks and institutional capacity to attract and facilitate investments and ensure safeguards being decisive to scale-up financing. Financing needs for the creation and strengthening of regulatory environment and institutional capacity, upstream financing needs as well as R&D and venture capital for development of new technologies and business models are often overlooked despite their critical role to facilitate the deployment of scaled-up climate finance ( high confidence). {15.4.1, 15.5.2}

The relatively slow implementation of commitments by countries and stakeholders in the financial system to scale up climate finance reflects neither the urgent need for ambitious climate action, nor the economic rationale for ambitious climate action (high confidence) . Delayed climate investments and financing – and limited alignment of investment activity with the Paris Agreement – will result in significant carbon lock-ins, stranded assets, and other additional costs. This will particularly impact urban infrastructure and the energy and transport sectors ( high confidence). A common understanding of debt sustainability and debt transparency, including negative implications of deferred climate investments on future GDP, and how stranded assets and resources may be compensated, has not yet been developed (medium conf idence). {15.6}

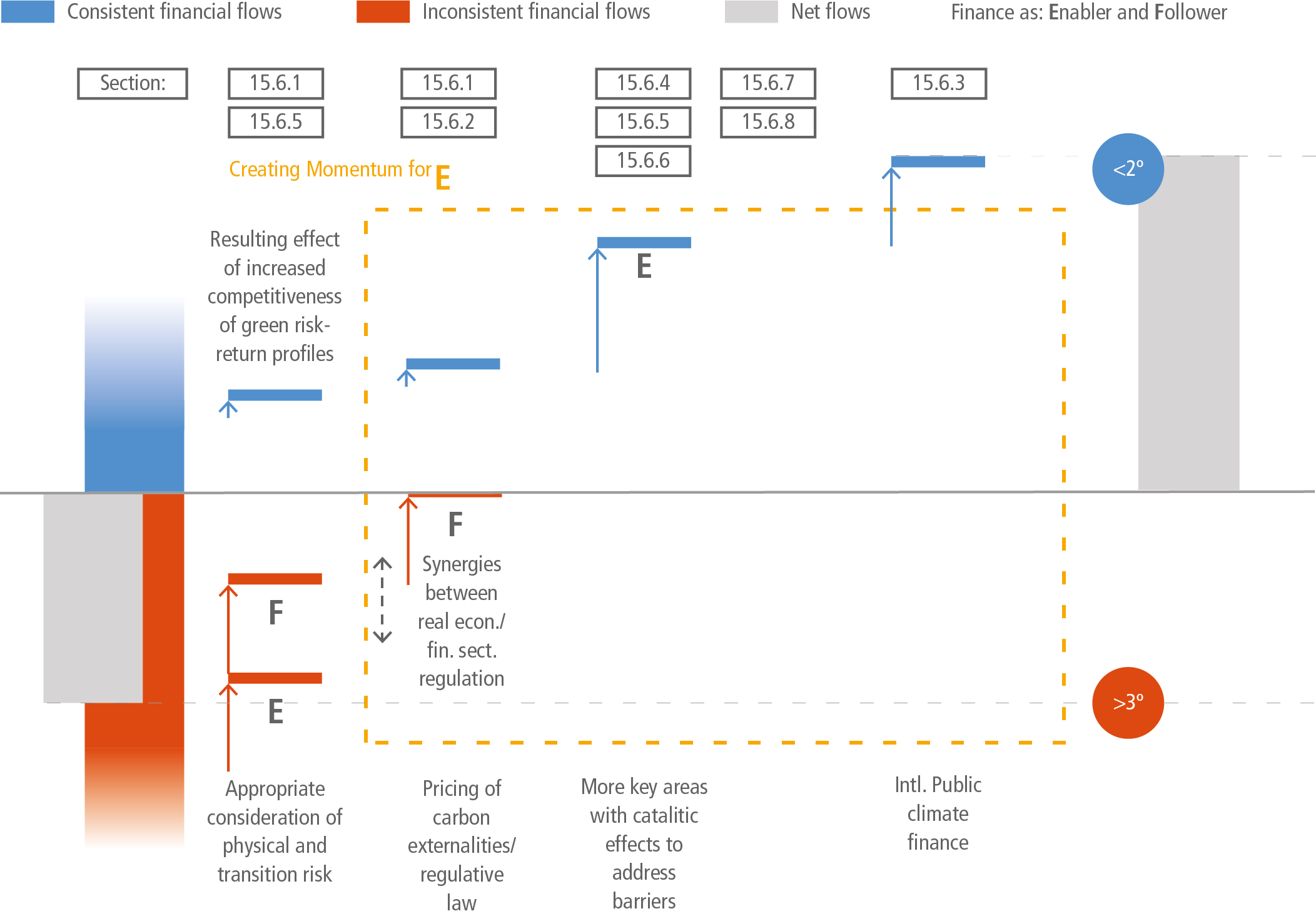

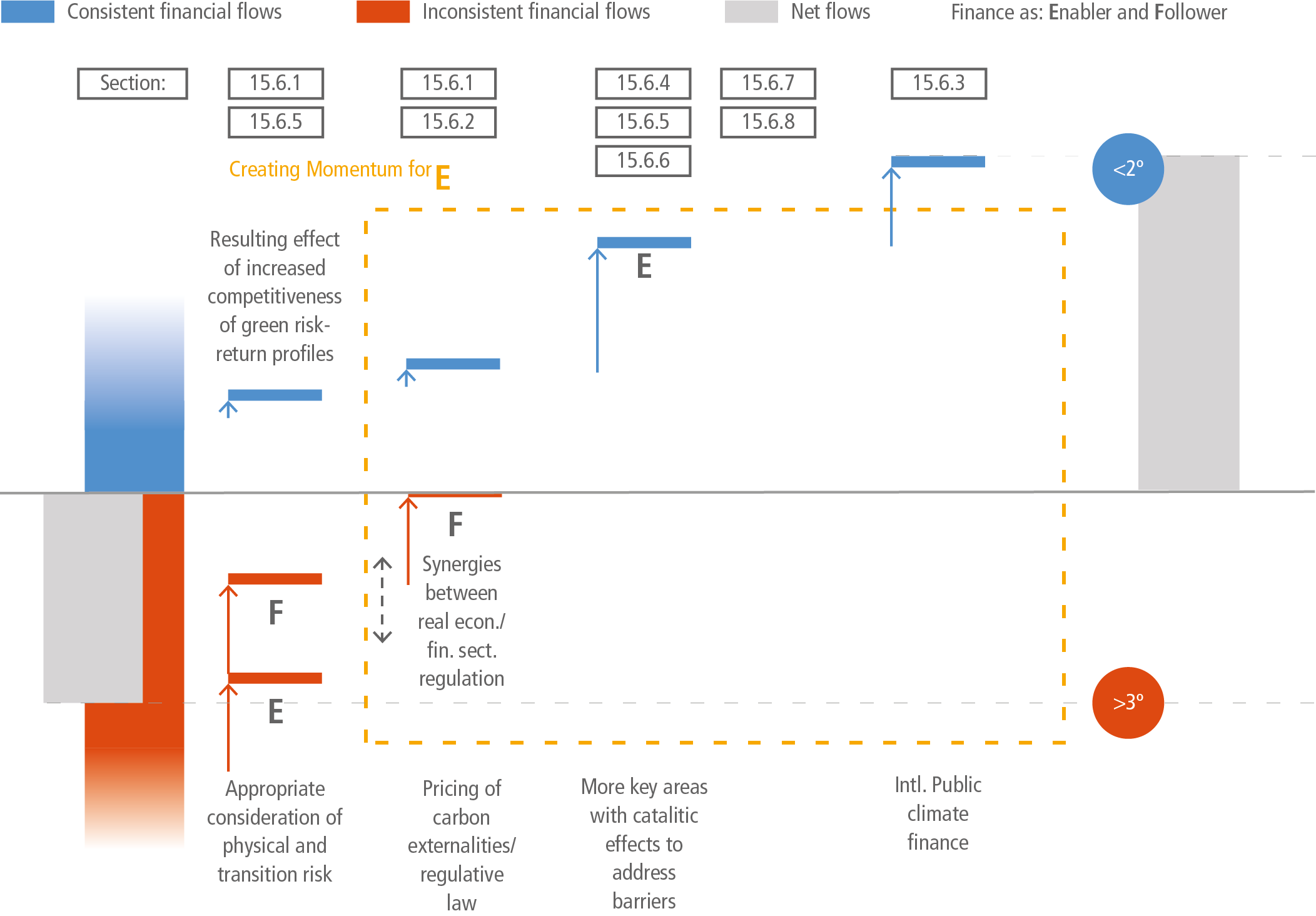

The greater the urgency of action to remain on a 1.5°C pathway the greater need for parallel investment decisions in upstream and downstream parts of the value chain. Greater urgency also reduces the lead times to build trust in regulatory frameworks. Consequently, many investment decisions will need to be made based on the long-term global goals. This highlights the importance of trust in political leadership which, in turn, affects risk perception and ultimately financing costs ( high confidence). {15.6.1, 15.6.2}

There is a mismatch between capital availability in the developed world and the future emissions expected in developing countries. This emphasises the need to recognise the explicit and positive social value of global cross-border mitigation financing. A significant push for international climate finance access for vulnerable and poor countries is particularly important given these countries’ high costs of financing, debt stress and the impacts of ongoing climate change ( high confidence). {15.2, 15.3.2.3, 15.5.2, 15.6.1, 15.6.7}

Ambitious global climate policy coordination and stepped-up (public) climate financing over the next decade (2021–2030) can help address macroeconomic uncertainty and alleviate developing countries’ debt burden post-COVID-19. It can also help redirect capital markets and overcome challenges relating to the need for parallel investments in mitigation and the up-front risks that deter economically sound low carbon projects. (high confidence). Providing strong climate policy signals helps guide investment decisions. Credible and clear signalling by governments and the international community reduce uncertainty for financial decision-makers and help reduce transition risk. In addition to indirect and direct subsidies, the public sector’s role in addressing market failures, barriers, provision of information, and risk sharing (equity, various forms of public guarantees) can encourage the efficient mobilisation of private sector finance ( high confidence). {15.2, 15.6.1, 15.6.2}

The mutual benefits of coordinated support for climate mitigation and adaptation in the next decade for both developed and developing regions could potentially be very high in the post-COVID-19 era. Climate compatible stimulus packages could significantly reduce the macro-financial uncertainty generated by the pandemic and increase the sustainability of the world economic recovery. {15.2, 15.3.2.3, 15.5.2, 15.6.1, 15.6.7}

Political leadership and intervention remain central to addressing uncertainty as a fundamental barrier for a redirection of financial flows. Existing policy misalignments – for example in fossil fuel subsidies – undermine the credibility of public commitments, reduce perceived transition risks and limit financial sector action ( high confidence). {15.2, 15.3.3, 15.6.1, 15.6.2, 15.6.3}

Innovative financing approaches could help reduce the systemic underpricing of climate risk in markets and foster demand for Paris-aligned investment opportunities. Approaches include de-risking investments, robust ‘green’ labelling and disclosure schemes, in addition to a regulatory focus on transparency and reforming international monetary system financial sector regulations (medium confidence) . Markets for green bonds, ESG (environmental, social, and governance), and sustainable finance products have grown significantly since the Fifth Assessment Report of the Intergovernmental Panel on Climate Change (IPCC AR5) and the landscape continues to evolve. Underpinning this evolution is investors’ preference for scalable and identifiable low-carbon investment opportunities. These relatively new labelled financial products will help by allowing a smooth integration into existing asset allocation models ( high confidence). Markets for green bonds, ESG (environmental, social, and governance), and sustainable finance products have also increased significantly since AR5, but challenges nevertheless remain, in particular there are concerns about ‘greenwashing’ and the limited application of these markets to developing countries. New business models (e.g., pay-as-you-go) can facilitate the aggregation of small-scale financing needs and provide scalable investment opportunities with more attractive risk-return profiles. Support and guidance for enhancing transparency can promote capital markets’ climate financing by providing quality information to price climate risks and opportunities. Examples include Sustainable Development Goals (SDG) and environmental, social and governance (ESG) disclosure, scenario analysis and climate risk assessments, including the Task Force on Climate-Related Financial Disclosures (TCFD). The outcome of these market-correcting approaches on capital flows cannot be taken for granted, however, without appropriate fiscal, monetary and financial policies. Mitigation policies will be required to enhance the risk-weighted return of low-emission and climate-resilient options, and – supported by progress in transparent and scientifically based projects’ assessment methods – to accelerate the emergence and support for financial products based on real projects, such as green bonds, and phase out fossil fuel subsidies. Greater public-private cooperation can also encourage the private sector to increase and broaden investments, within a context of safeguards and standards, and this can be integrated into national climate change policies and plans. {15.1, 15.2.4, 15.3.1, 15.3.2, 15.3.3, 15.5.2, 15.6.1, 15.6.2, 15.6.6, 15.6.7, 15.6.8}.

The following policy options can have important long-term catalytic benefits (high confidence) . (i) Stepped-up both the quantum and composition of financial, technical support and partnership in low-income and vulnerable countries alongside low-carbon energy access in low-income countries, such as in sub-Saharan Africa, which currently receives less than 5% of global climate financing flows; (ii) continued strong role of international and national financial institutions, including multilateral, especially location-based regional, and national development banks; (iii) de-risking cross-border investments in low-carbon infrastructure, development of local green bond markets, and the alignment of climate and non-climate policies, including direct and indirect supports on fossil fuels, consistent with the climate goals; (iv) lowering financing costs including transaction costs and addressing risks through funds and risk-sharing mechanisms for under-served groups; (v) accelerated finance for nature-based solutions, including mitigation in the forest sector (REDD+), and climate-responsive social protection; (vi) improved financing instruments for loss and damage events, including risk-pooling-transfer-sharing for climate risk insurance; (vii) economic instruments, such as phasing in carbon pricing and phasing out fossil fuel subsidies in a way that addresses equity and access; and (viii) gender-responsive and women-empowered programmes. {15.2.3, 15.2.4, 15.3.1, 15.3.2.2, 15.3.3, 15.4.1, 15.4.2, 15.4.3, 15.5.2, 15.6, 15.6.2, 15.6.4, 15.6.5, 15.6.6, 15.6.7, 15.6.8.2}

15.1Climate Finance – Key Concepts and Scope

Finance for climate action (or climate finance), environmental finance (which also covers other environmental priorities such as water, air pollution and biodiversity), and sustainable finance (which encompasses issues relating to socio-economic impacts, poverty alleviation and empowerment) are interrelated rather than mutually exclusive concepts (UNEP Inquiry 2016a; ICMA 2020a). Their combination is needed to align mitigation investments with multiple SDGs, and at a minimum, minimise the conflicts between climate targets and SDGs not being targeted. From a climate policy perspective, climate finance refers to finance ‘whose expected effect is to reduce net GHG emissions and/or enhance resilience to the impacts of climate variability and projected climate change’ (UNFCCC 2018a). However, as pinpointed in the AR5, significant room for interpretation and context-specific considerations remains. Further, such definition needs to be put in perspective with the expectations of investors and financiers (see Box 15.2).

Specifying the scope of climate finance requires defining two terms: what qualifies as ‘finance’ and as ‘climate’ respectively. In terms of what type of finance to consider, options include considering investments or total costs (Box 15.1), stocks or flows, gross or net (the latter taking into account reflows and/or depreciation), and domestic or cross-border, public or private (Box 15.2). In terms of what may be considered as ‘climate’, a key difference relates to measuring climate-specific finance (only accounts for the portion of finance resulting in climate benefits) or climate-related finance (captures total project costs and aims to measure the mainstreaming of climate considerations). One should even consider the investments decided for reasons unrelated with climate objectives but which contribute to these objectives (hydroelectricity, rail transportation).

In many cases, the scope of what may be considered as ‘climate finance’ will also depend on the context of implementation such as priorities and activities listed in countries’ Nationally Determined Contributions (NDCs) under the Paris Agreement (UNFCCC 2019a) as well as national development plans more broadly targeting the achievement of SDGs. Hence, rather than opposing the different options listed above, the choice of one or the other depends on the desired scope of measurement, which in turn depends on the policy objective being pursued. The increasingly diverse initiatives and body of grey literature address a range of different information needs. They provide analyses at the levels of domestic finance flows (e.g., UNDP 2015; Hainaut and Cochran 2018), international flows (e.g. OECD 2016; AfDB et al. 2018), global flows (UNFCCC 2018a; Buchner et al. 2019), the financial system (e.g., UNEP Inquiry 2016a) or specific financial instruments such as bonds (e.g., CBI 2018). Common frameworks, reporting transparency are, however, necessary in order to identify overlaps, commonalities and differences between these different measurements in terms of scope and underlying definitions. In that regard, the developments of national and international taxonomies, definitions and standards can help, as further discussed in Section 15.6, and Chapter 17 in AR6 WGII report.

Beyond the need to scale up levels of climate finance, the Paris Agreement provides a broad policy environment and momentum for a more systemic and transformational change in investment and financing strategies and patterns. Article 2.1c, which calls for ‘making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development’, positions finance as one of the Agreement’s three overarching goals (UNFCCC 2015). This formulation is a recognition that the mitigation and resilience goals cannot be achieved without finance, both in the real economy and in the financial system, being made consistent with these goals (Zamarioli et al. 2021). It has in turn contributed to the development of the concept of alignment (with the Paris Agreement) used in the financial sector (banks, institutional investors), businesses, and public institutions (development banks, public budgets). As a result, since AR5, in addition to measuring and analysing climate finance, an increasing focus has been placed on assessing the consistency or alignment, as well as respectively the inconsistency or misalignment, of finance with climate policy objectives, as for instance illustrated by the multilateral development banks’ joint framework for aligning their activities with the goals of the Paris Agreements (MDBs 2018).

Assessing climate consistency or alignment implies looking at all investment and financing activities, whether they target, contribute to, undermine or have no particular impact on climate objectives. This all-encompassing scope notably includes remaining investments and financing for high-GHG emission activities that may be incompatible with remaining carbon budgets, but also activities that may play a transition role in climate mitigation pathways and scenarios (Section 15.3.2.3). As a result, any meaningful assessment of progress requires the use of different shades to assess activities based on their negative, neutral (‘do no harm’) or positive contributions, (e.g., CICERO 2015; Cochran and Pauthier 2019; Natixis 2019). Doing so in practice requires the development of robust definitions, assessment methods and metrics, an area of work and research that remained under development at the time of writing. A range of financial sector coalitions and civil society organisations as well as commercial services providers to the financial industry have developed frameworks, approaches and metrics, mainly focusing on investment portfolios (Institut Louis Bachelier et al.. 2020; IIGCC 2021; TCFD Portfolio Alignment Team 2021; UN-Convened Net-Zero Asset Owner Alliance 2021), and, to a lesser extent for real economy investments (Micale et al. 2020; Jachnik and Dobrinevski 2021).

Key findings from AR5 and other IPCC publications. For the first time the IPCC in AR5 (Clarke et al. 2014) elaborated on the role of finance in a dedicated chapter. In the following year, the Paris Agreement (UNFCCC 2015) recognised the transformative role of finance, as a means to achieving climate outcomes, and the need to align financial flows with the long-term global goals even as implementation issues were left unresolved (Bodle and Noens 2018). AR5 noted the absence of a clear definition and measurement of climate finance flows, a difficulty that continues (Weikmans and Roberts 2019) (Sections 15.2 and 15.3). The approach taken in AR5 was to report ranges of available information on climate finance flows from diverse sources, using a broad definition of climate finance, as in the Biennial Assessments in 2014 and again in 2018 (UNFCCC 2014a, 2018a) of the Standing Committee under the UNFCCC: Climate finance is taken to refer to local, national or transnational financing – drawn from public, private and alternative sources of financing – that seeks to support mitigation and adaptation actions that address climate change (UNFCCC 2014b). For this chapter, while the focus is primarily on mitigation, adaptation, resilience and loss and damage financing needs cannot be entirely separated because of structural relationships, synergies, trade-offs and policy coherence requirements between these sub-categories of climate finance (Box 15.1).

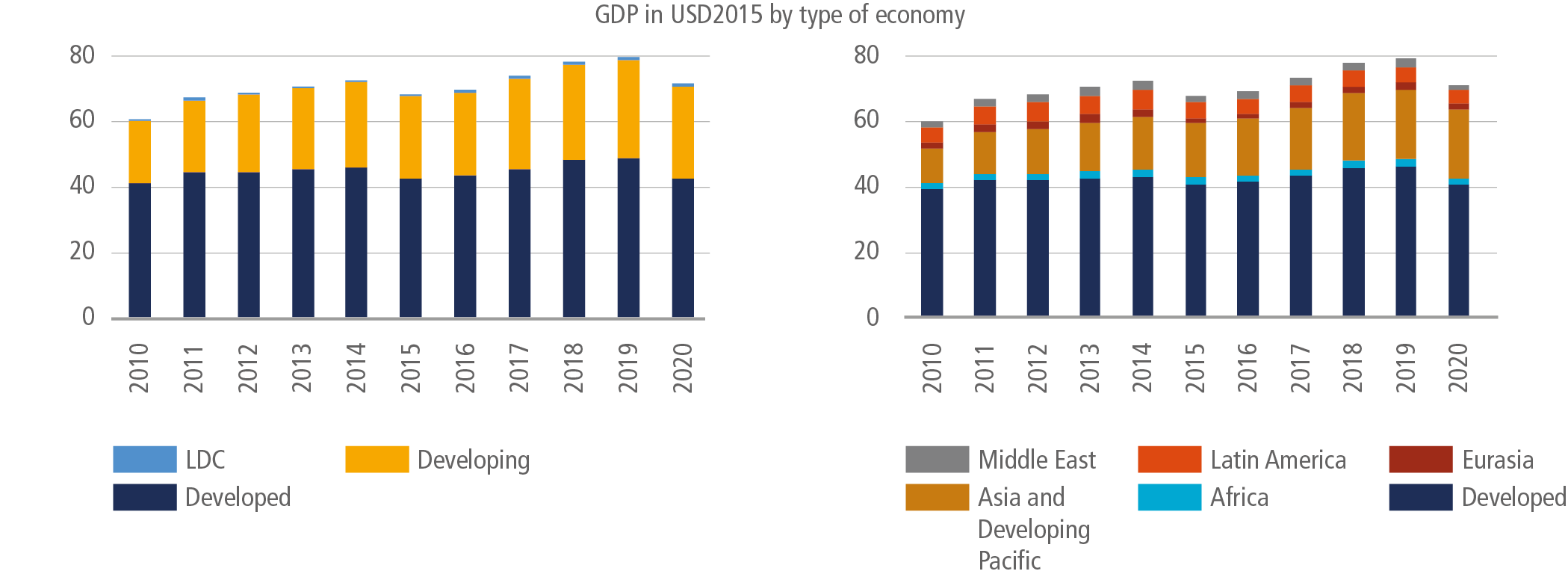

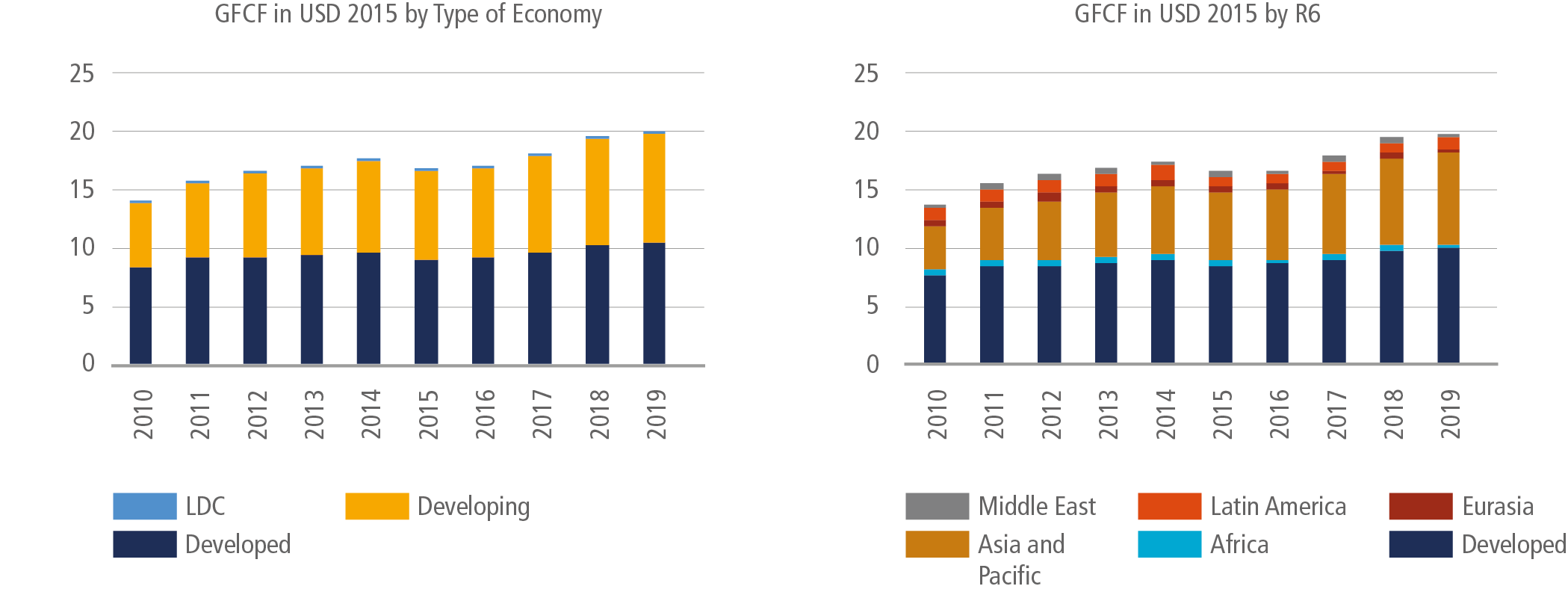

The AR5 concluded that published assessments of financial flows whose expected effect was to reduce net greenhouse gas (GHG) emissions and/or to enhance resilience to climate change aggregated USD343–385 billion 4 yr –1 globally between 2010 and 2012 (medium confidence). Most (95% of total) went towards mitigation, which was nevertheless underfinanced and adaptation even more so. Measurement of progress towards the commitment by developed countries to provide USD100 billion yr –1 by 2020 to developing countries, for both mitigation and adaptation (Bhattacharya et al. 2020) – a narrower goal than overall levels of climate finance – continued to be a challenge, given the lack of clear definition of such finance, although there remain divergent perspectives (Section 15.2.4). As against these flows, annual need for global aggregate mitigation finance between 2020 and 2030 was cited briefly in the AR5 to be about USD635 billion (mean annual), both public and private, implying that the reported ‘gap’ in mitigation financing of estimated flows during 2010 to 2012 was slightly under one-half of that required (IPCC 2014).

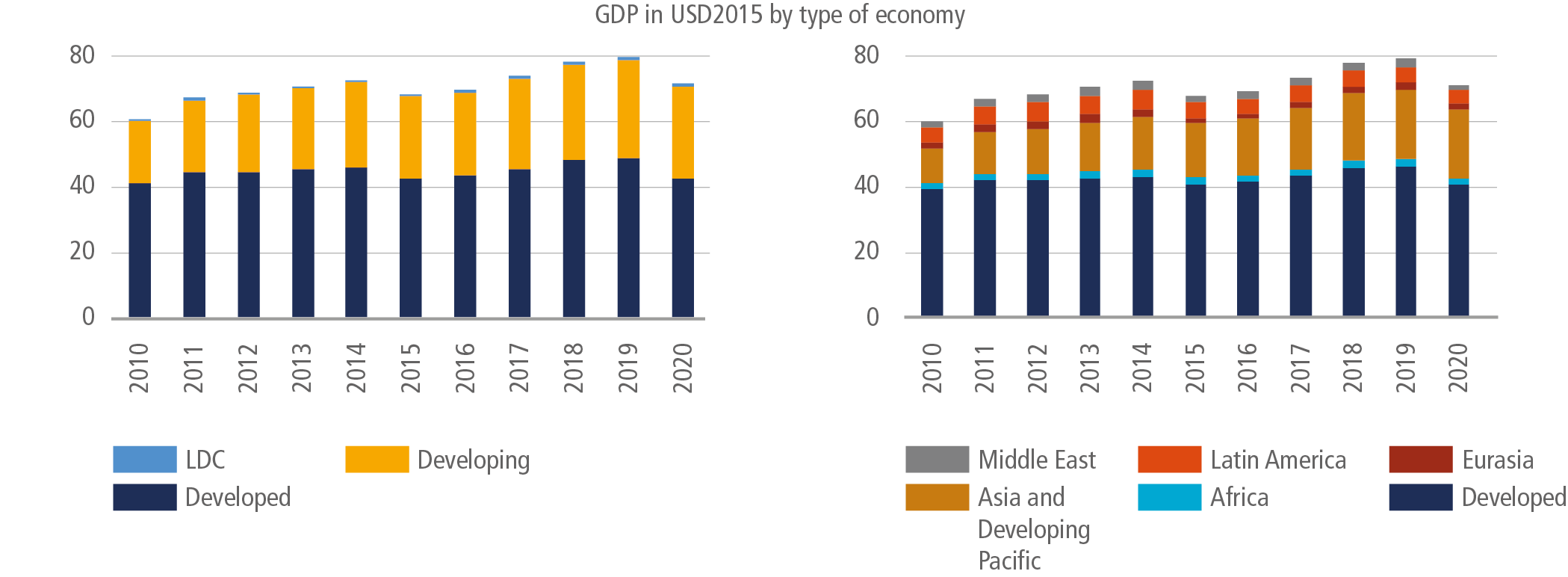

More recent published data from the Biennial Assessments (UNFCCC 2018a) and the Special Report on Global Warming of 1.5°C (IPCC 2018) have revised upwards the needs of financing between 2020 and 2030 to 2035 to contain global temperature rise to below 2°C and 1.5°C respectively by 2100: USD1.7 trillion yr –1 (mean) in the Biennial Assessment 2018 for the former, and for the latter, USD2.4 trillion yr –1 (mean) for the energy sector alone (and three times higher if transport and other sectors were to be included). The resulting estimated gaps in annual mitigation financing during 2014 to 2017, using reporting of climate financing from published sources, was about 67% for 2015, and 76% for the energy sector alone in 2017 (medium confidence), and greater if other sectors were to be included. While the annual reported flows of climate financing showed some moderate progress (Section 15.3), from earlier USD364 billion (mean 2010/2011) to about USD600 billion (mean 2017/2020), with a slowing in the most recent period 2014 to 2017, the gap in financing was reported to have widened considerably (Sections 15.4 and 15.5). In the context of policy coherence, it is also important to note that reported annual investments going into the fossil fuel sectors, oil and gas upstream and coal mining, during the same period were about the same size as global climate finance, although the absence of alternative financing and access to low-carbon energy is a complicating factor.

Adaptation financing needs, meanwhile, were rising rapidly. The Adaption Gap Report 2020 (UNEP 2021) reported that the current efforts are insufficient to narrow the adaptation finance gap, and additional adaptation finance is necessary, particularly in developing countries. The gap is expected to be aggravated by COVID-19 ( high confidence). It reaffirmed earlier assessments that by 2030 (2050) the estimated costs of adaptation ranges between USD140 and 300 billion yr –1 (USD280 and 500 billion yr –1). Against this, the reported actual global public finance flows for adaptation in 2019/2020 were estimated at 46 billion (Naran et al. 2021). The costs of climate disasters meanwhile continued to rise, affecting low-income developing countries the most. Climate natural disasters – not all necessarily attributable to climate change – caused some USD300 billion yr –1 economic losses and well-being losses of about USD520 billion yr –1 (Hallegatte et al. 2017).

Box 15.2 | Box 15.1 | Core Terms

This box defines some core terms used in this chapter as well as in other chapters addressing finance issues: cost, investment, financing, public and private. The chapter makes broad use of the term finance to refer to all types of transactions involving monetary amounts. It avoids the use of the terms funds and funding to the extent possible, which should otherwise be understood as synonyms for money and money provided.

Cost, investment and financing: different but intertwined concepts. Cost encompasses capital expenditures (CAPEX or upfront investment value leveraged over the lifetime of a project) operating and maintenance expenditures (OPEX), as well as financing costs. Note that some projects e.g., related to technical assistance may only involve OPEX (e.g., staff costs) but no CAPEX, or may not incur direct financing costs (e.g., if fully financed via own funds and grants).

Investment , in an economic sense, is the purchase of (or CAPEX for) a physical asset (notably infrastructure or equipment) or intangible asset (e.g., patents, IT solutions) not consumed immediately but used over time. For financial investors, physical and intangible assets take the form of financial assets such as bonds or stocks which are expected to provide income or be sold at a higher price later. In practice, investment decisions are motivated by a calculation of risk-weighted expected returns that takes into account all expected costs, as well as the different types of risks, discussed in Section 15.6.1, that may impact the returns of the investment and even turn them into losses.

Incremental cost (or investment ) accounts for the difference between the cost (or investment value) of a climate project compared to the cost (or investment value) of a counterfactual reference project (or investment). In cases where climate projects and investments are more cost effective than the counterfactual, the incremental cost will be negative.

Financing refers to the process of securing the money needed to cover an investment or project cost. Financing can rely on debt (e.g., through bond issuance or loan subscription), equity issuances (listed or unlisted shares), own funds (typically savings or auto-financing through retained earnings), as well as on grants and subsidies

Public and private: statistical standard and grey zones. International statistics classify economic actors as pertaining to the public or private sectors. Households always qualify as private and governmental bodies and agencies as public. Criteria are needed for other types of actors such as enterprises and financial institutions. Most statistics rely on the majority ownership and control principle. This is the case for the Balance of Payment, which records transactions between residents of a country and the rest of the world (IMF 2009).

Such a strict boundary between public and private sectors may not always be suitable for mapping and assessing investment and financing activities. On the one hand, some publicly owned entities may have a mandate to operate on a fully- or semi-commercial basis, for example state-owned enterprises, commercial banks, and pension funds, as well as sovereign wealth funds. On the other hand, some privately owned or controlled entities can pursue not-for-profit objectives, e.g., philanthropies and charities. The present chapter considers these nuances to the extent made possible by available data and information.

Box 15.2 | International Climate Finance Architecture

International climate finance can flow through different bilateral, multilateral, and other channels, involving a range of different types of institutions both public (official) and private (commercial) with different mandates and focuses. In practice, the architecture of international public climate finance is rapidly evolving, with the creation by traditional donors of new public sources and channels over the years (Watson and Schalatek 2019), as well as emergence of new providers of development co-operation, both bilateral (Benn and Luijkx 2017) and multilateral (e.g., Asian Infrastructure Investment Bank), as well as of non-governmental actors such as philanthropies (OECD 2018a).

The operationalisation of the Green Climate Fund (GCF), which channels the majority of its funds via accredited entities, has notably attracted particular attention since AR5. Section 14.3.2 (in Chapter 14) provides a further assessment of progress and challenges of financial mechanisms under the United Nations Framework Convention on Climate Change (UNFCCC), such as the GCF, the Global Environment Facility (GEF) and the Adaptation Fund (AF).

The multiplication of sources and channels of international climate finance can help address growing climate-related needs, and partly results from increased decentralisation as well financial innovation, which in turn can increase the effectiveness of finance provided. There is, however, also evidence that increased complexity implies transaction costs (Brunner and Enting 2014), in part due to bureaucracy and intra-governmental factors (Peterson and Skovgaard 2019), which constitutes a barrier to low-carbon projects and are often not accounted for in assessments of international climate finance. On the ground, activities by international providers operating in the same countries may overlap, with sub-optimal coordination and hence duplication of efforts, both on the bilateral and multilateral sides (Ahluwalia et al. 2016; Gallagher et al. 2018; Humphrey and Michaelowa 2019), as well as risks of fragmentation of efforts (Watson and Schalatek 2020) which slows down coordination with international providers, national development banks and other domestic institutions.

Box 15.3 | Mitigation, Adaptation and Other Related Climate Finance Merit Joint Examination

Mitigation finance deals with investments that aim to reduce global carbon emissions, while adaptation finance deals with the consequences of climate change (Lindenberg and Pauw 2013). Mitigation affects the scale of adaptation needs and adaptation may have strong synergies and co-benefits as well as trade-offs with mitigation (Grafakos et al. 2019). If mitigation investments are inadequate to reducing global warming (as in the last decade) with asymmetric adverse impacts in lower latitudes and low-lying geographies, the scale of adaptation investments has to rise and the benefits of stronger adaptation responses may be high (Markandya and González-Eguino 2019). If adaptation investments build greater resilience, they might even moderate mitigation financing costs. Similar policy coherence considerations apply to disaster risk reduction financing, the scale of which depends on success with both adaptation and mitigation (Mysiak et al. 2018). The same financial actors, especially governments and the private sector, decide at any given time on their relative allocations of available financing for mitigation, adaptation and disaster-risk reduction from a constrained common pool of resources. The trade-offs and substitutability between closely-linked alternative uses of funds, therefore, make it essential for a simultaneous assessment of needs – as in parts of this chapter. Climate finance versus the financing of other Sustainable Development Goals (SDGs) faces a similar issue. A key agreement was that climate financing should be ‘new and additional’ and not at the cost of SDGs. Resources prioritising climate at the cost of non-climate development finance increase the vulnerability of a population for any given level of climate shocks, and additionality of climate financing is thus essential (Brown et al. 2010). Policy coherence is also the reason why mitigation finance cannot be separated from consideration of spending and subsidies on fossil fuels. Climate change may additionally cause the breaching of physical and social adaptation limits, resulting in climate-related residual risks (i.e., potential impacts after all feasible mitigation, adaptation, and disaster risk reduction measures have been implemented) (Mechler et al. 2020). Because these residual losses and damages from climate-related risks are related to overall mitigation and adaptation efforts, the magnitude of potential impacts is related to the overall quantum of mitigation, adaptation, and disaster risk reduction finance available (Frame et al. 2020). All categories of climate finance thus need to be considered together in discussions around climate finance.

15.2Background Considerations

The institutions under climate finance in this chapter refer to the set of financial actors, instruments and markets that are recognised to play a key role in financing decisions on climate mitigation and adaptation. For a definition of climate financial stock and flows see further Section 15.3 and the Glossary. The issue of climate finance is closely related to the conversation on international cooperation and the question of how cross-border investments can support climate mitigation and adaptation in developing countries. However, the issue is also related to more general questions of how financial institutions, both public and private, can assess climate risks and opportunities from all investments, and what roles states, policymakers, regulators and markets can play in making them more sustainable. In particular, the question of the respective roles of the public and private financial actors has become important in deliberations on climate finance in recent years. The broader macroeconomic context is an important starting point. Four major events and macro trends mark the developments in climate finance in the previous five years and likely developments in the near term.

•First, the 2015 Paris Agreement, with the engagement of the financial sector institutions in the climate agenda, has been followed by a series of related developments in financial regulation in relation to climate change and in particular to the disclosure of climate-related financial risk ( high confidence) (Section 15.2.1).

• Second, the last five years have been characterised by a series of interconnected ‘headwinds’ (Section 15.2.2), including rising private and public debt and policy uncertainty which work against the objective of filling the climate investment gap ( high confidence).

•Third, the 2020 COVID-19 pandemic crisis has put enormous additional strain on the global economy, debt and the availability of finance, which will be longer lasting (Section 15.2.3). At the same time, while it is still too early to draw positive conclusions, this crisis highlights opportunities in terms of political and policy feasibility and behavioural change in respect of realigning climate finance (medium confidence).

•Fourth, the sharp rise in global inequality and the effects of the pandemic have brought into renewed sharp focus the need for a Just Transition (Section 15.2.4) and a realignment of climate finance and policies that would be beneficial for a new social compact towards a more sustainable world that addresses energy equity and environmental justice ( high confidence).

15.2.1Paris Agreement and the Engagement of the Financial Sector in the Climate Agenda

This is the first IPCC Assessment Report chapter on investment and finance since the 2015 Paris Agreement, which represented a landmark event for climate finance because for the first time the key role of aligning financial flows to climate goals was spelled out. Since then, the financial sector has recognised the opportunity and has stepped up to centre-stage in the global policy conversation on climate change. While before the Paris Agreement, only few financial professionals and regulators were acquainted with climate change, today climate change is acknowledged as a strategic priority in most financial institutions. This is a major change in the policy landscape from AR5. However, this does not mean that finance necessarily plays an adequate enabling role for climate investments. On the contrary, the literature shows that without appropriate conditions, finance can represent a barrier to filling the climate investment gap (Hafner et al. 2020). Indeed, despite the enormous acceleration in policy initiatives (e.g., NGFS 2020) and coalitions of the willing in the private sectors, the effect in terms of closing the investment gap identified already in AR5 has been limited (Section 15.5.2).

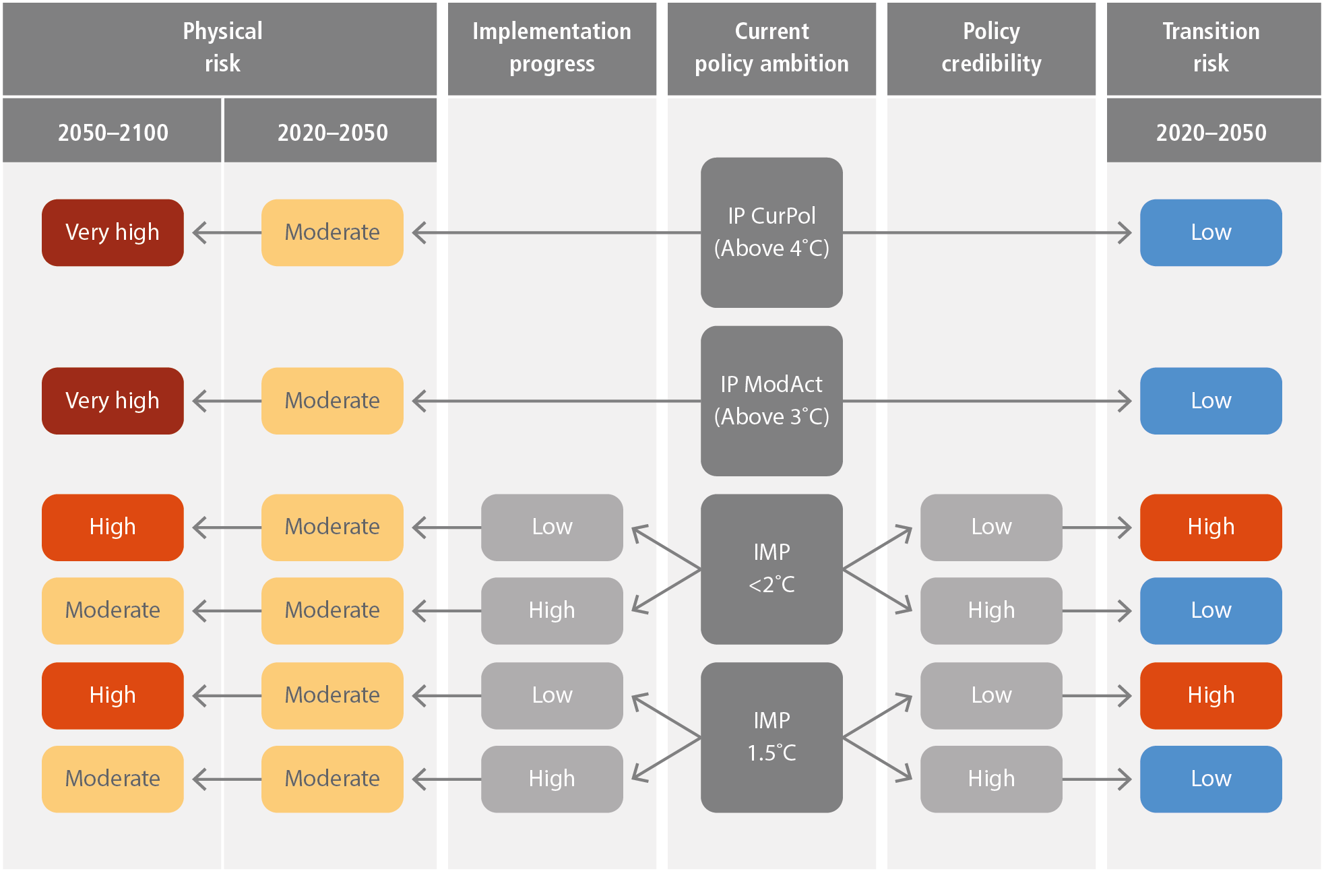

Financial investors have started to account for climate risk in some contexts but they do so only to a limited extent (Monasterolo and de Angelis 2020; Alessi et al. 2021; Bolton and Kacperczyk 2021) and the reasons for these remain unclear. Two aspects are relevant here. The first is the endogenous nature of climate financial risk and opportunities (with the term ‘risk’ meaning here the potential for adverse financial impact, whether or not the distribution of losses is known). Academics and practitioners in finance are aware that financial risk can in certain contexts be endogenous, that is, the materialisation of losses is affected by the action of financial players themselves. However, the standard treatment of risk both in financial valuation models and in asset pricing assumes that risk is exogenous. In contrast, endogeneity is a key feature of climate risk because today’s perception of climate risk affects climate investment, which in turn affects directly the future risk. This endogeneity leads to the fact that multiple and rather different mitigation scenarios are possible (Chapter 3). Moreover, the likelihood of occurrence of each alternative scenario is very hard to estimate. Further, the assessment of climate-related financial risk requires to combine information related to mitigation scenarios as well as climate impact scenarios, leaving open an important knowledge gap for the next years (Section 15.6.1).

The second aspect is that the multiplicity of equilibria results in a coordination problem whereby the majority of investors wait to move and reallocate their investments until they can follow a clear signal. Despite the initial momentum of the Paris Agreement, for many investors, both public and private, the policy signal seems not strong enough to induce them to align their investment portfolios to climate goals.

Analyses of the dynamics of the low-carbon transition suggest that it does not occur by itself and that it requires a policy signal credible enough in the perception of market players and investors (Battiston et al. 2021b). Credibility could require a policy commitment device (Brunner et al. 2012). The commitment would also need to be large enough (analogous to the ‘whatever it takes’ statement by the European Central Bank during the 2011–2012 European sovereign crisis (Kalinowski and Chenet 2020)). In principle, public investments in low-carbon infrastructures (or private-public partnerships) as well as regulation could provide credible signals if their magnitude and time horizon are appropriate (past experiences with feed-in-tariffs (FiTs) models across countries provide useful lessons).

15.2.2Macroeconomic Context

Entering 2020, the world already faced large macroeconomic headwinds to meeting the climate finance gap in the near term – barring some globally coordinated action. While an understanding of the disaggregated country-by-country, sector-by-sector, project-by-project, and instrument-by-instrument approach to raising climate finances analysed in the later parts of this chapter remains important, macroeconomic drivers of finance remain crucial in the near term.

Near-term finance financial flows in aggregate often show strong empirically observed cycles over time, especially in terms of macroeconomic and financial cycles. By near-term, we mean here the likely cycle over the next five to ten years (2020–2025 and 2020–2030), as influenced by global macroeconomic real business cycles (output, investment and consumption), with periodic asymmetric downside impacts and crises (Gertlerand Kiyotaki 2010; Borio 2014; Jordà et al. 2017; Borio et al. 2018). Financial cycles typically have strong co-movements (asset prices, credit growth, interest rates, leverage, risk factors, market fear, macro-prudential and central bank policies) (Coeurdacier and Rey 2013), they have large consequences for all types of financial flows such as equity, bond and banking credit markets, which in turn are likely to impact climate finance flows to all sub-sectors and geographies (with greater expected volatility in more risky and more leveraged regions). This is in contrast to longer-term trend considerations (2020–2050) that typically focus the attention on drivers of disaggregated flows of climate finance and policies. The upward trends of the cycles tend to favour speculative bubbles like real estates at the expense of investment in production and infrastructures whereas the asymmetric downsides raise uncertainty and risks for longer-term investments on newer climate technologies, and favour a flight to near-term safety (e.g., lowest risk non-climate short-term treasury investments, highest creditworthy countries, and away from cross-border investments (Section 15.5) – making the challenge of longer-term low-carbon transition more difficult. In this respect, the impact of financial regulation is unclear. On the one hand, it could be argued that the tighter bank regulations under Basel III, combined with an economic environment with higher uncertainty and flatter yield curve, can push banks to retrench from climate finance projects (Blended Finance Taskforce, 2018a), since banks tend to limit loan maturity to five or eight years, while infrastructure projects typically require the amortisation of debt over 15 to 20 years (Arezki et al. 2016). On the other hand, other studies report that stricter capital requirements are not a driving factor for moving away from sustainability projects (CISL and UNEP FI 2014).

Four key aspects of the global macroeconomy, each slightly different, pointed in a cascading fashion towards a deteriorating environment for stepped-up climate financing over the next crucial decade (2020–2030), even before COVID-19. The argument is often made that there is enough climate financing available if the right projects and enabling policy actions (‘bankable projects’) present themselves (Cuntz et al. 2017; Meltzer 2018). The attention to ‘bankability’ does not however address access and equity issues (Bayliss and Van Waeyenberge 2018). Some significant gains in climate financing at the sectoral and microeconomic levels were nevertheless happening in specific segments, such as solar energy financing and labelled green bonds (although how much of such labelled financing is incremental to unlabelled financing that might have happened anyway remains uncertain) (Tolliver et al. 2019). Issues of ‘labelling’ (Cornell 2020) apply even more to ESG (environmental, social and governance) investments, which started to grow rapidly after 2016 (Section 15.6.5). Overall, these increments for climate finance remained, however, small in aggregate relative to the size of the shifts in climate financing required in the coming decade. Annual energy investments in developing regions (other than China) which account for two-thirds of the world population, with least costs of mitigation per tonne of emissions (one-half that in developed regions), and for the bulk of future expected global GHG emissions, saw a 20% decline since 2016, and only a one-fifth share of global clean energy investment, reflecting persistent financing problems and costs of mobilising finance towards clean energy transition, even prior to the pandemic (IEA 2021a). In the words of a macroeconomic institution, ‘tangible policy responses to reduce greenhouse gas emissions have been grossly insufficient to date’ (IMF 2020a). The reason is in part global macroeconomic headwinds, which show a relative stagnation since 2016 and limited cross-border flows in particular (Yeo 2019).

Slowing and more unstable GDP growth. The first headwind was more unstable and slowing GDP growth at individual country levels and in aggregate because of worsening climate change impact events (Donadelli et al. 2019; Kahn et al. 2019). As each warmer year keeps producing more negative impacts – arising from greater and rising variability and intensity of rainfall, floods, droughts, forest fires and storms – the negative consequences have become more macro-economically significant, and worst for the most climate-vulnerable developing countries ( high confidence). Paradoxically, while these effects should have raised the social returns and incentives to invest more in future climate mitigation, a standard public policy argument, these macroeconomic shocks may work in the opposite direction for private decisions by raising the financing costs now (Cherif and Hasanov 2018). With some climate tipping points, potentially in the near-term reach (see AR6 WGI Chapter 4) the uncertainty with regard to the economic viability and growth prospects of selected macroeconomically critical sectors increases significantly (AR6 WGII Chapters 8 and 17). Taking account of other behavioural failures, this was creating a barrier for proactive and accelerated mitigation and adaptation action.

Public finances. The second headwind was rising public fiscal costs of mitigation and adapting to rising climate shocks affecting many countries, which were negatively impacting public indebtedness and country credit ratings (Cevik and Jalles 2020; Klusak et al. 2021) at a time of growing stresses on public finances and debt (Benali et al. 2018; Kling et al. 2018; Kose et al. 2020) ( high confidence). Every climate shock and slowing growth puts greater pressures on public finances to offset these impacts. Crucially, the negative consequences were typically greater at the lower end of income distributions everywhere (Acevedo et al. 2018; Aggarwal 2019). As a result, the standard prescription of raising distributionally adverse carbon taxes and reducing fossil fuel subsidies to raise resources faced political pushback in several countries (Copland 2020; Green 2021), and low rates elsewhere. Reduced taxes on capital, by contrast, was viewed as a way to improve growth (Bhattarai et al. 2018; Font et al. 2018), and working against broader fiscal action. Progress with carbon pricing remained modest across 44 OECD and G20 countries, with 55–70% of all carbon emissions from energy use entirely unpriced as of 2018 (OECD 2021a). Climate-vulnerable countries meanwhile faced sharply rising cost of sovereign debt. Buhr et al. (2018) calculate the additional financing costs of Climate Vulnerable Forum countries of USD40 billion 5 on government debt over the past 10 years and USD62 billion for the next 10 years. Including private financing cost, the amount increases to USD146–168 billion over the next decade.

Credit risks. The third headwind is rising financial and insurance sector risks and stresses (distinct from real ‘physical’ climate risks above) arising from the impacts of climate change, and systematically affecting both national and international financial institutions and raising their credit risks ( high confidence) (Dafermos et al. 2018; Rudebusch 2019; Battiston et al. 2021a). Central banks are beginning to take notice (Carney 2019; NGFS 2019). It is also the case that, even if at greater risk from stranded assets in the future, the large-scale financing of new fossil fuel projects by large global financial institutions rose significantly since 2016, because of perceived lower private risks and higher private returns in these investments and other factors than in alternative but perceived more risky low-carbon investments.

Global growth. The fourth headwind entering 2020 was the sharply slowing global macroeconomic growth, and prospects for near-term recession (which occurred in the pandemic). During global real and financial cycle downturns (Jordà et al. 2019), the perception of general financial risk rises, causing financial institutions and savers to reallocate their financing to risk-free global assets ( high confidence). This ‘flight to safety’ was evident even before the recent pandemic, marked by an extraordinary tripling of financial assets to about USD16.5 trillion in negative-interest earning ‘safer’ assets in 2019 in world debt markets – enough to have nearly closed the total financing gap in climate finance over a decade.

15.2.3Impact of COVID-19 Pandemic

The macroeconomic headwinds have worsened dramatically with the onset of COVID-19. Almost two years after the pandemic started, it is still too uncertain and early to conclude impacts of the pandemic until 2025–2030, especially as they affect climate finance. Multiple waves of the pandemic, new virus mutations, accumulating human toll, and growing vaccine coverage but vastly differing access across developed versus developing regions, are evident. They are causing divergent impacts across sectors and countries, which combined with the divergent ability of countries and regions to mount sufficient fiscal and monetary policy actions imply continued high uncertainty on the economic recovery paths from the crisis. The situation remains more precarious in middle- and low-income developing countries (IMF 2021a). While recovery is happening, the job losses have been large, poverty rates have climbed, public health systems are suffering long-term consequences, education gains have been set back, public debt levels are higher (5–10% of GDP higher), financial institutions have come under longer-term stress, a larger number of developing countries are facing debt distress, and many key high-contact sectors, such as tourism and trade, will take time to recover (Eichengreen et al. 2021). The implication is negative headwinds for climate finance with public attention focused on pandemic relief and recovery and limited (and divergent) fiscal headroom for a low-carbon transition, with considerable uncertainties ahead (Hepburn et al. 2020b; Maffettone and Oldani 2020; Steffen et al. 2020).

The larger and still open public policy choice question that COVID-19 now raises is whether there is room for public policy globally and in respect of their individual economies to integrate climate more centrally to their growth, jobs and sustainable development strategies worldwide for ecological and economic survival. The outcomes will depend on the robustness of recovery from the pandemic, and the still evolving public policy responses to the climate agenda in the recovery process. Private equity and asset markets have recovered surprisingly rapidly during the pandemic (in response to the massive fiscal and central bank actions generating large excess savings with very low or negative yields boosting stock markets). On public spending, some early studies suggest that the immediate economic recovery packages were falling well short of being sufficiently climate sustainable (Gosens and Jotzo 2020; Kuzemko et al. 2020; O’Callaghan 2021) but several governments have also announced intentions to spend more on a green recovery, ‘build back better’ and Just Transition efforts (Section 15.2.4), although outcomes remain highly uncertain (Lehmann et al. 2021; Markandya et al. 2021).

An important immediate finding from the COVID-19 crisis was that the slowdown in economic activity is illustrating some of these choices: immediately after the onset, more costly and carbon-intensive coal use for energy use tumbled in major countries such as China and the USA, while the forced ‘stay-at-home’ policies adopted around the major economies of the world led to a –30–35% decline in individual country GDP, and was in turn associated with a decrease in daily global CO2 emissions by –26% at their peak in individual countries, and –17% globally (–11 to –25% for ±1σ) by early April 2020 compared with the mean 2019 levels, with just under half coming from changes in surface transport, city congestion and country mobility (Le Quéré et al. 2020). Along with the carbon emissions drop was a dramatic improvement in other parameters such as clean air quality. Moreover, longer-term behavioural impacts are also possible: a dramatic acceleration of digital technologies in communications, travel, retail trade and transport. The question however is whether the world might revert to the earlier carbon-intensive path of recovery, or to a different future, and the choice of policies in shaping this future. Studies generally suggest that the gains from long-term impacts of the pandemic on future global warming will be limited and depend more on the nature of public policy actions and long-term commitments by countries to raise their ambitions, not just on climate but on sustainable development broadly (Barbier 2020; Barbier and Burgess 2020; Forster et al. 2020; Gillingham et al. 2020; Reilly et al. 2021). The positive lesson is clear: opportunities exist for accelerating structural change, and for a re-orientation of economic activity modes to a low-carbon use strategy in areas such as coal use in energy consumption and surface transport, city congestion and in-country mobility, for which lower-cost alternatives exist and offer potentially dramatic gains (Hepburn et al. 2020b).

A new consensus and compact towards such a structural change and economic stimulus instruments may therefore need to be redrawn worldwide, where an accelerated low-carbon transition is a priority; and accelerated climate finance to spur these investments may gain by becoming fully and rapidly integrated with near-term economic stimulus, growth and macroeconomic strategies for governments, central banks, and private financial systems alike. If that were to happen, COVID-19 may well be a turning point for sustainable climate policy and financing. Absent that, a return to ‘business-as-usual’ modes will mean a likely down-cycle in climate financing and investments in the near term.

Expectations that the recovery package stimulus will increase economic activity rely on the assumption that increased credit investment will have a positive effect on demand, the so-called demand-led policy (Mercure et al. 2019). The argument for a green recovery also draws on the experience from the post-global financial crisis in 2008–2009 recovery, in which large economies such as China, South Korea, the USA and the EU observed that green investments propelled the development of new industrial sectors. Noticeably, this had a positive net effect on job creation when compared to the investment in traditional infrastructure (UKERC 2014; Vona et al. 2018; Jaeger et al. 2020). For a more in-depth discussion on macroeconomic-finance possible response see Section 15.6.3. Here, we conclude with the options for reviving a better globally coordinated macroeconomic climate action. The options are some combinations of five possible elements:

1. Reaffirmation of a strong financial agenda in future UNFCCC Conference of Parties meetings, and a new collective finance target, which will need to be undertaken by 2025. Given that the shortfalls in financing are likely to be acute for developing regions and especially the more debt-stressed and vulnerable (Dibley et al. 2021; Elkhishin and Mohieldin 2021; Laskaridis 2021; Umar et al. 2021), developed countries may wish to step up their collective support (Resano and Gallego 2021). One possibility is to expedite the new Special Drawing Rights (SDR) issuance allocation rules for the USD650 billion recently (2021) approved, most of which will go to increase the reserves of G7 and other high-income countries unless voluntarily reallocated towards the needs of the most vulnerable low-income countries, raising resources potentially ‘larger than the Marshall Plan in today’s money’ (IMF 2021b; Jensen 2021; Obstfeld and Truman 2021), with decisions to be taken. Ameli et al. (2021a) note the climate investment trap of the current high cost of finance that effectively lowers green electricity production possibilities in Africa for a cost optimal pathway. Other initiatives could also include G7 and G20 governments (especially with the lead taken by the developed members for cross-border support to avoid over-burdening public resources in developing countries) running coordinated fiscal deficits to accelerate the financing of low carbon investments (‘green fiscal stimulus’).

2. Introducing new actions, including regulatory, to take some of the risks off the table from institutional financial players investing in climate mitigation investment and insurance. This could include the provision of larger sovereign guarantees to such private finance, primarily from developed countries but jointly with developing countries to create a level playing field (Dafermos et al. 2021) backed by explicit and transparent recognition of the ‘social value of mitigation actions’ or SVMAs, as fiscally superior (because of bigger ‘multipliers’ of such fiscal action to catalyse private investment than direct public investment) and the bigger social value of such investments (Article 108, UNFCCC) (Hourcade et al. 2018; Krogstrup and Oman 2019).

3. Facilitating and incentivising much larger flows of cross-border climate financing which is especially crucial for such investments to happen in developing regions, where as much as two-thirds of collective investment may need to happen (IEA 2021a), and where the role of multilateral, regional and global institutions such as the International Monetary Fund (IMF) (including the expansion in availability of climate SDRs referred to earlier) could be important.

4. Global central banks acting in coordination to include climate finance as an intrinsic part of their monetary policy and stimulus (Carney 2019; Jordà et al. 2019; Hilmi et al. 2021; Schoenmaker 2021; Svartzman et al. 2021).

5. An acceleration of Just Transition initiatives, outlined further below (Section 15.2.4).

15.2.4Climate Finance and Just Transition

Climate financein support of a Just Transition is likely to be a key to a successful low-carbon transition globally ( high confidence). Ambitious global climate agreements are likely to work far better by maximising cooperative arrangements (IPCC 2018; Gazzotti et al. 2021) with greater financing support from developed to developing regions in recognition of ‘common but differentiated responsibilities and respective capabilities’ and a greater ethical sense of climate justice (Khan et al. 2020; Sardo 2020; Warner 2020; Pearson et al. 2021). While Just Transition issues apply within developed countries as well (see later discussion), these are of relatively second-order significance to addressing climate justice issues between richer and poorer countries – given the scale of financing and existing social safety nets in the former and their absence in the latter. For example, over the past three decades drought in Africa has caused more climate-related mortality than all climate-related events combined from the rest of the world (Warner 2020). These issues can however serve both as a bridge and a barrier to greater cooperation on climate change. The key is to build greater mutual trust with clearer commitments and well-structured key decisions and instruments (Sardo 2020; Pearson et al. 2021).

The Just Transition discussion has picked up steam. It was explicitly recognised in the Paris Agreement and the 2018 Just Transition Declaration signed by 53 countries at COP24, which ‘recognised the need to factor in the needs of workers and communities to build public support for a rapid shift to a zero-carbon economy.’ Originally proposed by global trade unions in the 1980s, the recent discourse has become broader. It has coalesced into a more inclusive process to reduce inequality across all three areas of energy, environment and climate (McCauley and Heffron 2018; Bainton et al. 2021). It seeks accelerated public policy support to ensure environmental sustainability, decent work, social inclusion and poverty eradiation (Burrow 2017), widely shared benefits, and protection of indigenous rights, and livelihoods of communities and workers who stand to lose (including workers in fossil fuel sectors such as coal and oil and gas) (UNFCCC 2018b; EBRD 2020; Jenkins et al. 2020). Because the process involves ‘climate justice’ and equity within and across generations, it involves difficult political trade-offs (Newell and Mulvaney 2013). The implications for a Just Transition in climate finance are clear: expanding equitable and greater access to climate finance for vulnerable countries, communities and sectors, not just for the most profitable private investment opportunities, and a larger role for public finance in fulfilling existing finance commitments (Bracking and Leffel 2021; Kuhl 2021; Long 2021; Roberts et al. 2021).

Large shocks such as pandemics, and slow-growing ones such as climate, are typically known to worsen inequality (IMF and World Bank 2020 ). Evidence from 133 countries between 2001–2018 suggests that such shocks can cause social unrest, and migration pressures, especially when starting inequality is high and social transfers are low (Saadi Sedik and Xu 2020). Additionally, climate policies are more politically difficult to implement when the setting is one of high inequality but much less politically costly where incomes are more evenly distributed with stronger social safety nets (Furceri et al. 2021). A redrawn social compact incorporating climate (Beck et al. 2021) that would adopt redistributive taxes and lower carbon consumption, and strengthen state capacity to deliver safety nets, health and education with accelerated climate and environmental sustainability within and across countries, is increasingly recognised as important. Countries, regions and coordination bodies of the larger countries (G7, G20) have already begun such a shift to financing of a Just Transition, but primarily focused on the developed countries, although gaps remain (Krawchenko and Gordon 2021).

Such a redrawing of a social compact has happened significantly in the past, for example, after the 1860s ‘gilded age of capital’ with the enlargement of the franchise in democratisation waves in Europe and the Americas (Dasgupta and Ziblatt 2015, 2016). Not only was social conflict avoided but growth outcomes became more equitable and faster. Similarly, comprehensive modern social safety nets and progressive taxation, which started in the Great Depression and was extended in the post-war period, had both a positive pro-growth and lower inequality effects (Brida et al. 2020).

There are three levels at which policy attention on climate financing now may need to be focused. The first is the need to address the global equity issues in climate finance in a more carefully constructed globally cooperative public policy approach. The second is to address issues appropriately with enhanced support, at the national level. The third is to work it down further, to addressing needs at local community levels. Because private investors and financing mostly deal with allocation to climate finance at a global portfolio level, then to allocation by countries, and finally to individual projects, the challenge for them is to refocus attention to Just Transition issues at the country level, but also globally as well as locally (in other words, at all three levels).

Climate finance will likely face greater challenges in the post-pandemic context (Hanna et al. 2020; Henry et al. 2020). Evidence from the COVID-19 pandemic suggests that those in greatest vulnerability often had the least access to human, physical, and financial resources (Ruger and Horton 2020). It has also left in in its wake divergent prospects for economic recovery, with rising constraints on credit ratings and costly debt burden in many developing countries contrasted with the exceptionally low interest rate settings in developed economies driving the limited fiscal space in the former groups (Benmelech and Tzur-Ilan 2020). Similarly, monetary policies are likely to be much tighter in developing countries in part structurally because of the absence of ‘exceptional privilege’ of global reserve currencies in developed economies.

The result is a divergence in recovery prospects in the aftermath of the pandemic, with output losses (compared to potential) set to worsen in developing economies (excluding China) as compared to developed countries (IMF 2020b). In these circumstances, a coordinated and cooperative approach, instead of unilateralism, might work better (McKibbin and Vines 2020). In the case of climate, simulations clearly suggest the need and advantages of better coordinated climate action with stepped-up Paris Agreement envisaged transfers (IMF 2020b). Several options in international climate finance arrangements to support a Just Transition are both available and urgent.

As a first priority, measures might need to accelerate a mix of equitable financial grants, low-interest loans, guarantees and workable business models access across countries and borders, from developed countries to low-income countries. A big push on low-carbon energy access globally, especially in large low-income regions such as Africa, with accelerated financial transfers, makes sense (Boamah 2020). For about one billion people globally at the base of the pyramid without access to modern low-carbon energy access, such an action, with enormous immediate leap-frogging potential, would be a key pathway to achieve the SDGs, ensure that high-carbon energy use is avoided, such as the burning of biomass and forests for charcoal, and improve air quality and public health, especially women’s health (van der Zwaan et al. 2018; Nathwani and Kammen 2019; Dalla Longa and van der Zwaan 2021; Michaelowa et al. 2021; Osabuohien et al. 2021).

A second priority is to accelerate the implementation of the USD100 billion a year (and likely more, given growing financing gaps) in climate finance commitments expressed in the Copenhagen Agreement Accord (and reiterated since) from developed to developing countries, and to build greater confidence by agreeing rapidly on key definitions. Shifting to a grant equivalent net flows definition of climate finance, which is now universally accepted for all other aid flows by all parties since 2014 and which took effect since 2019 on every other public international good finance provision (under the SDGs), with the sole exception of climate finance, would resolve many uncertainties: the disbursement of climate finance flows on a grant equivalent basis that is comparable across institutions, instruments and countries, and measurement with greater accuracy about the effective transfer of resources. The journey to get to a clear and precise definition of net official overseas development assistance (ODA) took time. The original proposal was first initiated in the 1960s (Pincus 1963) but it was not till multilateral development banks (MDBs) and others laid out the compelling reasons why (Chang et al. 1998) that this was accomplished: especially to resolve decades of confusion and inconsistency between different types of financial flows and hence the perennial measurement problems and ‘the compromise between political expediency and statistical reality’ (Bulow and Rogoff 2005; Hynes and Scott 2013; Scott 2015, 2017).

A third related and increasingly crucial priority is to expedite the operational definition of blended finance and promote the use of public guarantee instruments. Private flows to accelerate the low-carbon transition in developing countries would benefit enormously, by gaining clearer access to public international funds and support defined on a grant equivalent basis, provided development and climate finance operational definitions and procedures were improved on an urgent basis (Blended Finance Taskforce 2018a; OECD-DAC 2021). When blended and supported by public finance and policy, the grant equivalency measure can easily and more accurately measure the value and benefit of blended public and private finance by comparing the effective interest cost (and volume) gain with such financing, against the benchmark costs without such blending. Here again, a pressing challenge is to improve the operational definitions of what counts as ODA within blended finance. Blended finance remains very poorly defined and accounted (Pereira 2017; Andersen et al. 2019; Attridge and Engen 2019; Basile and Dutra 2019). Guarantees are expressly not included in the definition of ODA (Garbacz et al. 2021). As a result, bilateral and multilateral agencies have no incentive or limited authority and basis to use such instruments, while multilateral development banks continue to approach guarantees with great caution because of the limits of their original charters (World Bank 2009) and require counter-indemnities by recipient countries, internal and historic agency inertia, perceived loss of control over the use of funds (compared to their preferred direct project-based lending) and employ restrictive accounting rules for capital provisioning of guarantees at 100% of their face value to maintain AAA ratings with credit rating agencies (Humphrey 2017; Pereira dos Santos and Kearney 2018; Bandura and Ramanujam 2019; Hourcade et al. 2021a). Largely because of such official uncertainty the actual flows of blended finance and guarantees continue to remain a very small share (typically, less than 5%) of official and multilateral finance flows to lower project risks and costs, and hence the potential for large-scale accelerated low-carbon private investments in developing countries. Public guarantees can offer a fifteen times multiplier effect on the scale of low-carbon investments generated with such support, compared to a 1:1 ratio in direct financing (Hourcade et al. 2021a).

It makes sense to expedite these operational procedures (Khan et al. 2020) which cannot be otherwise explained except in terms of avoiding responsibilities, even where the benefits would be high (Klöck et al. 2018). It also causes (unnecessary) fragmentation and complexity and often ‘strategic’ ambiguity by many actors (Pickering et al. 2017), which worsens the possibilities for international cooperation, a critical requirement to achieve the Paris goals (IPCC 2018). The world would gain collectively if these issues were to be decided soon. The absence of such a collective decision continues to be exceptionally costly for the implementation of the Paris Agreement because of the fractious and seemingly insoluble negotiating climate and a breakdown of trust that this has created (Roberts and Weikmans 2017).

A fourth priority is expanding jobs and dealing with job losses in the global low-carbon transition (Carley and Konisky 2020; Crowe and Li 2020; Pai et al. 2020; Cunningham and Schmillen 2021; Hanto et al. 2021), especially in coal and other sectors, as well as land and other effects for indigenous communities (Zografos and Robbins 2020). Many countries, especially low-income countries, remain dependent on fossil fuels for their energy and exports and jobs, and support for their transition to a low-carbon future will be essential. Global recovery from the pandemic will take longer than initially envisaged (IMF 2021c; OECD 2021b) and an accelerated climate action for a Build Back Better global infrastructure plan with better and more resilient jobs might play a key role as part of the Just Transitions. Already, there is substantial evidence (Sulich et al. 2020; Dell’Anna 2021; Dordmond et al. 2021) that a more sustainable climate path would generate many more net productive jobs (with much higher employment multipliers and mutual gains from given spending) than would any other large-scale alternative. But this would nevertheless require a carefully managed transition globally, including access to much larger volumes of climate financing in developing economies (Muttitt and Kartha 2020). The multilateral finance institutions have generally played a supportive role, expanding their financing to developing countries during the pandemic (even as bilateral aid flows have fallen sharply), but have been hampered by the constraints on their mandates and instruments (as noted earlier). Political leadership and direction will be again crucial to enhance their roles. The recent expansion of SDR quotas at the IMF similarly might help, but the current distributions of quota benefits flow primarily to the developed countries and do little to expand investment flows on a longer-term basis for a global expansion in growth and job opportunities in the low-carbon transition.

As a fifth priority, transformative climate financing options based on equityand global sustainability objectives may also need to consider a greater mix of public pricing and taxation options on the consumption side (Arrow et al. 2004; Folke et al. 2021). Two-thirds of global GHG emissions directly or indirectly are linked to household consumption, with average per capita carbon footprint of North America and Europe of 13.4 and 7.5 tCO2-eq per capita, respectively, compared to 1.7 in Africa and Middle East (Gough 2020) and as high as 200 tCO2-eq per capita among the top 1% in some high-income geographies versus 0.1 tCO2-eq at the other end of the income distribution in some least-developed countries (Chancel and Piketty 2015). Globally, the highest-expenditure households account for eleven times the per capita emissions of lowest-expenditure households, with rising carbon income elasticities that suggest ‘redistribution of carbon shares from global elites to global poor’ as welfare efficient (Chancel and Piketty 2015; Hubacek et al. 2017). Within countries and regions,and within sectors, similar patterns hold. The top 10% of the population with the highest per capita footprints account for 27% of the EU carbon footprint, and the top 1% have a carbon footprint of 55 tCO2-eq per capita, with air transport the most elastic, unequal and carbon-intensive consumption (Ivanova and Wood 2020). Similarly, within sectors, there are large differences in carbon-intensity in the building sector in North America (Goldstein et al. 2020) and across cities where consumption-based GHG emissions vary widely across the world (ranging from 1.8 to 25.9 tCO2-eq per capita).

Numerous options exist (Broeks et al. 2020; Nyfors et al. 2020) for such carbon consumption reduction measures, while potentially improving societal well-being, for example: (i) inner-city zoning restrictions on private cars and promoting walking/bicycle use and improved shared low-carbon transport infrastructure; (ii) advertising regulation and carbon taxes and fees on high-carbon luxury status goods and services; (iii) subsidies and exemptions for low-carbon options, higher value-added taxes on specific high-carbon products and services, subsidies for public low-carbon options such as commuter transport, and other behavioural nudges (Reisch et al. 2021); and (iv) framing options (emphasising total cost of car over lifetimes), mandatory smart metering, collective goods and services (leasing, renting, sharing options) and others. Finally, reducing subsidies on fossil fuels, raising the progressivity of taxes and raising overall wealth taxes on the richest households, which have been sharply falling (Scheuer and Slemrod 2021) even as global income and wealth have risen, with regressive and falling overall taxes (Alvaredo et al. 2020; Saez and Zucman 2020), could effectively generate significant revenues (over 1% of GDP yr –1), about the same size as the proposed global USD50 pertonne carbon price proposed and estimated by the IMF/OECD 2021 report to the G20 (IMF and OECD 2021) to cover expected net interest costs on overall decarbonisation initiatives and financing of green new deals (Schroeder 2021).

These five options identified above on near-term actions and priorities will however, require greater collective political leadership. A review of past crisis episodes suggests that collective actions to avoid large global or multi-country risks work well primarily when the problems are well defined, a small number of actors are involved, solutions are relatively well established scientifically, and public costs to address them are relatively small (Sandler 1998, 2015) (for example, dealing with early pandemic outbreaks such as Ebola, TB, and cholera; extending global vaccination programmes such as smallpox, measles and polio; early warning systems and actions for natural disasters such as tsunamis, hurricanes/cyclones and volcanic disasters; the Montreal Protocol for ozone-depleting refrigerants, and renewables wind and solar energy development). They do not appear to work as well for more complex global collective action problems which concern a number of economic actors, sectors, without inexpensive and mature technological options, and where political and institutional governance is fragmented. Greater political coordination is needed because the impacts are often not near term or imminent, but diffuse, slow moving and long term, and where preventive disaster avoidance is costly even when these costs are low compared to the longer-term damages – till tipping points are reached of the need for reduced ‘stressors’ and increasing ‘facilitators’ (Jagers et al. 2020). But by then, it may be too late.

Private institutional investors equally might equally wish to pay greater attention to the Just Transition finance issues. It would be useful for investors to identify ways to support to such initiatives, and more clearly identify the benefits of such transition measures envisaged by both countries and investment financing proposals, including incorporating Just Transition consideration in their support to broader ESG and green financing initiatives.