Summary for Policymakers

This Summary for Policymakers should be cited as:

IPCC, 2022: Summary for Policymakers. In: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change[P.R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, J. Malley, (eds.)]. Cambridge University Press, Cambridge, UK and New York, NY, USA. doi: 10.1017/9781009157926.001.

A. Introduction and Framing

The Working Group III (WGIII) contribution to the IPCC’s Sixth Assessment Report (AR6) assesses literature on the scientific, technological, environmental, economic and social aspects of mitigation of climate change. 1 Levels of confidence 2 are given in () brackets. Numerical ranges are presented in square [] brackets. References to Chapters, Sections, Figures and Boxes in the underlying report and Technical Summary (TS) are given in {} brackets.

The report reflects new findings in the relevant literature and builds on previous IPCC reports, including the WGIII contribution to the IPCC’s Fifth Assessment Report (AR5), the WGI and WGII contributions to AR6 and the three Special Reports in the Sixth Assessment cycle, 3 as well as other UN assessments. Some of the main developments relevant for this report include {TS.1, TS.2}:

•An evolving international landscape. The literature reflects, among other factors: developments in the UN Framework Convention on Climate Change (UNFCCC) process, including the outcomes of the Kyoto Protocol and the adoption of the Paris Agreement {13, 14, 15, 16}; the UN 2030 Agenda for Sustainable Development including the Sustainable Development Goals (SDGs) {1, 3, 4, 17}; and the evolving roles of international cooperation {14}, finance {15} and innovation {16}.

•Increasing diversity of actors and approaches to mitigation. Recent literature highlights the growing role of non-state and sub-national actors including cities, businesses, Indigenous Peoples, citizens including local communities and youth, transnational initiatives, and public-private entities in the global effort to address climate change {5, 13, 14, 15, 16, 17}. Literature documents the global spread of climate policies and cost declines of existing and emerging low emission technologies, along with varied types and levels of mitigation efforts, and sustained reductions in greenhouse gas (GHG) emissions in some countries {2, 5, 6, 8, 12, 13, 16}, and the impacts of, and some lessons from, the COVID-19 pandemic. {1, 2, 3, 5, 13, 15, Box TS.1, Cross-Chapter Box 1 in Chapter 1}

•Close linkages between climate change mitigation, adaptation and development pathways. The development pathways taken by countries at all stages of economic development impact GHG emissions and hence shape mitigation challenges and opportunities, which vary across countries and regions. Literature explores how development choices and the establishment of enabling conditions for action and support influence the feasibility and the cost of limiting emissions {1, 3, 4, 5, 13, 15, 16}. Literature highlights that climate change mitigation action designed and conducted in the context of sustainable development, equity, and poverty eradication, and rooted in the development aspirations of the societies within which they take place, will be more acceptable, durable and effective {1, 3, 4, 5}. This report covers mitigation from both targeted measures, and from policies and governance with other primary objectives.

•New approaches in the assessment. In addition to the sectoral and systems chapters {3, 6, 7, 8, 9, 10, 11, 12}, the report includes, for the first time in a WGIII report, chapters dedicated to demand for services, and social aspects of mitigation {5, Box TS.11}, and to innovation, technology development and transfer {16}.The assessment of future pathways in this report covers near term (to 2030), medium term (up to 2050), and long term (to 2100) time scales, combining assessment of existing pledges and actions {4, 5}, with an assessment of emissions reductions, and their implications, associated with long-term temperature outcomes up to the year 2100 {3}. 4 The assessment of modelled global pathways addresses ways of shifting development pathways towards sustainability. Strengthened collaboration between IPCC Working Groups is reflected in Cross-Working Group Boxes that integrate physical science, climate risks and adaptation, and the mitigation of climate change. 5

•Increasing diversity of analytic frameworks from multiple disciplines including social sciences. This report identifies multiple analytic frameworks to assess the drivers of, barriers to and options for, mitigation action. These include: economic efficiency, including the benefits of avoided impacts; ethics and equity; interlinked technological and social transition processes; and socio-political frameworks, including institutions and governance {1, 3, 13, Cross-Chapter Box 12 in Chapter 16}. These help to identify risks and opportunities for action, including co-benefits and just and equitable transitions at local, national and global scales. {1, 3, 4, 5, 13, 14, 16, 17}

Section B of this Summary for Policymakers (SPM) assesses Recent developments and current trends, including data uncertainties and gaps . Section C, System transformations to limit global warming, identifies emission pathways and alternative mitigation portfolios consistent with limiting global warming to different levels, and assesses specific mitigation options at the sectoral and system level. Section D addresses Linkages between mitigation, adaptation, and sustainable development . Section E, Strengthening the response, assesses knowledge of how enabling conditions of institutional design, policy, finance, innovation and governance arrangements can contribute to climate change mitigation in the context of sustainable development.

B. Recent Developments and Current Trends

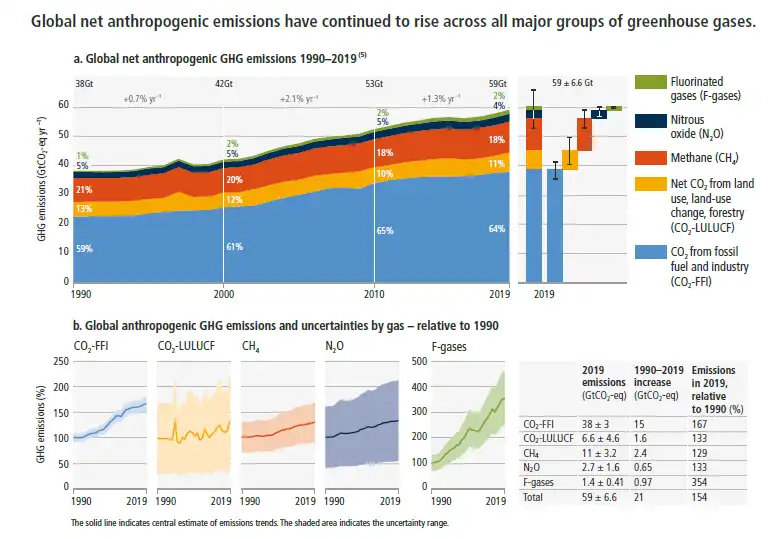

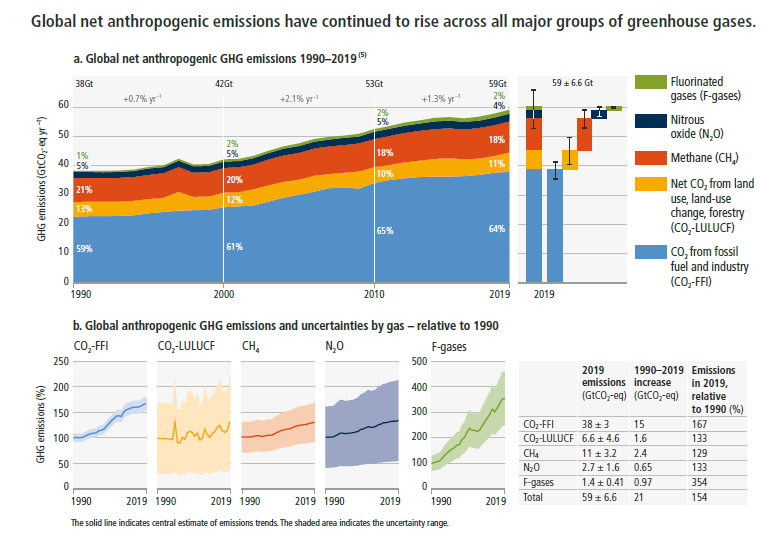

B.1 Total net anthropogenic GHG emissions6have continued to rise during the period 2010-2019, as have cumulative net CO2 emissions since 1850. Average annual GHG emissions during 2010–2019 were higher than in any previous decade, but the rate of growth between 2010 and 2019 was lower than that between 2000 and 2009. (high confidence) Expand Figure SPM.1 Links to chaptersFigure 2.2, Figure 2.5, Table 2.1, 2.2, Figure TS.2

Figure SPM.1 Links to chaptersFigure 2.2, Figure 2.5, Table 2.1, 2.2, Figure TS.2

B.1.1 Global net anthropogenic GHG emissions were 59 ± 6.6 GtCO2-eq 7 , 8 in 2019, about 12% (6.5 GtCO2-eq) higher than in 2010 and 54% (21 GtCO2-eq) higher than in 1990. The annual average during the decade 2010–2019 was 56 ± 6.0 GtCO2-eq, 9.1 GtCO2-eq yr –1 higher than in 2000–2009. This is the highest increase in average decadal emissions on record. The average annual rate of growth slowed from 2.1% yr –1 between 2000 and 2009 to 1.3% yr –1 between 2010 and 2019. (high confidence) (Figure SPM.1) {Figure 2.2, Figure 2.5, Table 2.1, 2.2, Figure TS.2}

B.1.2Growth in anthropogenic emissions has persisted across all major groups of GHGs since 1990, albeit at different rates. By 2019, the largest growth in absolute emissions occurred in CO2 from fossil fuels and industry followed by CH4, whereas the highest relative growth occurred in fluorinated gases, starting from low levels in 1990 (high confidence). Net anthropogenic CO2 emissions from land use, land-use change and forestry (CO2-LULUCF) are subject to large uncertainties and high annual variability, with low confidence even in the direction of the long-term trend. 9 (Figure SPM.1) {Figure 2.2, Figure 2.5, 2.2, Figure TS.2}

B.1.3Historical cumulative net CO2 emissions from 1850 to 2019 were 2400 ± 240 GtCO2 (high confidence). Of these, more than half (58%) occurred between 1850 and 1989 [1400 ± 195 GtCO2], and about 42% between 1990 and 2019 [1000 ± 90 GtCO2]. About 17% of historical cumulative net CO2 emissions since 1850 occurred between 2010 and 2019 [410 ± 30 GtCO2]. 10 By comparison, the current central estimate of the remaining carbon budget from 2020 onwards for limiting warming to 1.5°C with a probability of 50% has been assessed as 500 GtCO2, and as 1150 GtCO2 for a probability of 67% for limiting warming to 2°C. Remaining carbon budgets depend on the amount of non-CO2 mitigation (±220 GtCO2) and are further subject to geophysical uncertainties. Based on central estimates only, cumulative net CO2 emissions between 2010 and 2019 compare to about four-fifths of the size of the remaining carbon budget from 2020 onwards for a 50% probability of limiting global warming to 1.5°C, and about one-third of the remaining carbon budget for a 67% probability to limit global warming to 2°C. Even when taking uncertainties into account, historical emissions between 1850 and 2019 constitute a large share of total carbon budgets for these global warming levels. 11 , 12 Based on central estimates only, historical cumulative net CO2 emissions between 1850 and 2019 amount to about four-fifths 12 of the total carbon budget for a 50% probability of limiting global warming to 1.5°C (central estimate about 2900 GtCO2), and to about two thirds 12 of the total carbon budget for a 67% probability to limit global warming to 2°C (central estimate about 3550 GtCO2). {Figure 2.7, 2.2, Figure TS.3, WGI Table SPM.2}

B.1.4Emissions of CO2-FFI dropped temporarily in the first half of 2020 due to responses to the COVID-19 pandemic (high confidence), but rebounded by the end of the year (medium confidence). The annual average CO2-FFI emissions reduction in 2020 relative to 2019 was about 5.8% [5.1–6.3%], or 2.2 [1.9–2.4] GtCO2 (high confidence). The full GHG emissions impact of the COVID-19 pandemic could not be assessed due to a lack of data regarding non-CO2GHG emissions in 2020. {Cross-Chapter Box 1 in Chapter 1, Figure 2.6, 2.2, Box TS.1, Box TS.1 Figure 1}

Figure SPM.1 | Global net anthropogenic GHG emissions (GtCO2-eqyr–1) 1990–2019. Global net anthropogenic GHG emissions include CO2 from fossil fuel combustion and industrial processes (CO2-FFI); net CO2 from land use, land-use change and forestry (CO2-LULUCF)9; methane (CH4); nitrous oxide (N2O); and fluorinated gases (HFCs, PFCs, SF6, NF3). 6Panel a shows aggregate annual global net anthropogenic GHG emissions by groups of gases from 1990 to 2019 reported in GtCO2-eq converted based on global warming potentials with a 100-year time horizon (GWP100-AR6) from the IPCC Sixth Assessment Report Working Group I (Chapter 7). The fraction of global emissions for each gas is shown for 1990, 2000, 2010 and 2019; as well as the aggregate average annual growth rate between these decades. At the right side of Panel a, GHG emissions in 2019 are broken down into individual components with the associated uncertainties (90% confidence interval) indicated by the error bars: CO2-FFI ±8%; CO2-LULUCF ±70%; CH4±30%; N2O ±60%; F-gases ±30%; GHG ±11%. Uncertainties in GHG emissions are assessed in Supplementary Material 2.2. The single-year peak of emissions in 1997 was due to higher CO2-LULUCF emissions from a forest and peat fire event in South East Asia. Panel b shows global anthropogenic CO2-FFI, net CO2-LULUCF, CH4, N2O and F-gas emissions individually for the period 1990–2019, normalised relative to 100 in 1990. Note the different scale for the included F-gas emissions compared to other gases, highlighting its rapid growth from a low base. Shaded areas indicate the uncertainty range. Uncertainty ranges as shown here are specific for individual groups of greenhouse gases and cannot be compared. The table shows the central estimate for: absolute emissions in 2019; the absolute change in emissions between 1990 and 2019; and emissions in 2019 expressed as a percentage of 1990 emissions. {2.2, Figure 2.5, Supplementary Material 2.2, Figure TS.2}

B.2Net anthropogenic GHG emissions have increased since 2010 across all major sectors globally. An increasing share of emissions can be attributed to urban areas. Emissions reductions in CO2 from fossil fuels and industrial processes (CO2-FFI), due to improvements in energy intensity of GDP and carbon intensity of energy, have been less than emissions increases from rising global activity levels in industry, energy supply, transport, agriculture and buildings. (high confidence) ExpandLinks to chapters2.2, 2.4, 6.3, 7.2, 8.3, 9.3, 10.1, 11.2

B.2.1In 2019, approximately 34% (20 GtCO2-eq) of total net anthropogenic GHG emissions came from the energy supply sector, 24% (14 GtCO2-eq) from industry, 22% (13 GtCO2-eq) from agriculture, forestry and other land use (AFOLU), 15% (8.7 GtCO2-eq) from transport and 6% (3.3 GtCO2-eq) from buildings. 13 If emissions from electricity and heat production are attributed to the sectors that use the final energy, 90% of these indirect emissions are allocated to the industry and buildings sectors, increasing their relative GHG emissions shares from 24% to 34%, and from 6% to 16%, respectively. After reallocating emissions from electricity and heat production, the energy supply sector accounts for 12% of global net anthropogenic GHG emissions. (high confidence) {Figure 2.12, 2.2, 6.3, 7.2, 9.3, 10.1, 11.2, Figure TS.6}

B.2.2Average annual GHG emissions growth between 2010 and 2019 slowed compared to the previous decade in energy supply (from 2.3% to 1.0%) and industry (from 3.4% to 1.4%), but remained roughly constant at about 2% yr –1 in the transport sector (high confidence). Emissions growth in AFOLU, comprising emissions from agriculture (mainly CH4 and N2O) and forestry and other land use (mainly CO2) is more uncertain than in other sectors due to the high share and uncertainty of CO2-LULUCF emissions (medium confidence). About half of total net AFOLU emissions are from CO2-LULUCF, predominantly from deforestation 14 (medium confidence). {Figure 2.13, 2.2, 6.3, 7.2, Figure 7.3, 9.3, 10.1, 11.2, TS.3}

B.2.3The global share of emissions that can be attributed to urban areas is increasing. In 2015, urban emissions were estimated to be 25 GtCO2-eq (about 62% of the global share) and in 2020, 29 GtCO2-eq (67–72% of the global share). 15 The drivers of urban GHG emission are complex and include population size, income, state of urbanisation and urban form. (high confidence) {8.1, 8.3}

B.2.4Global energy intensity (total primary energy per unit GDP) decreased by 2% yr –1 between 2010 and 2019. Carbon intensity (CO2 from fossil fuel combustion and industrial processes (CO2-FFI) per unit primary energy) decreased by 0.3% yr –1, with large regional variations, over the same period mainly due to fuel switching from coal to gas, reduced expansion of coal capacity, and increased use of renewables. This reversed the trend observed for 2000–2009. For comparison, the carbon intensity of primary energy is projected to decrease globally by about 3.5% yr –1 between 2020 and 2050 in modelled scenarios that limit warming to 2°C (>67%), and by about 7.7% yr –1 globally in scenarios that limit warming to 1.5°C (>50%) with no or limited overshoot. 16 (high confidence) {Figure 2.16, 2.2, 2.4, Table 3.4, 3.4, 6.3}

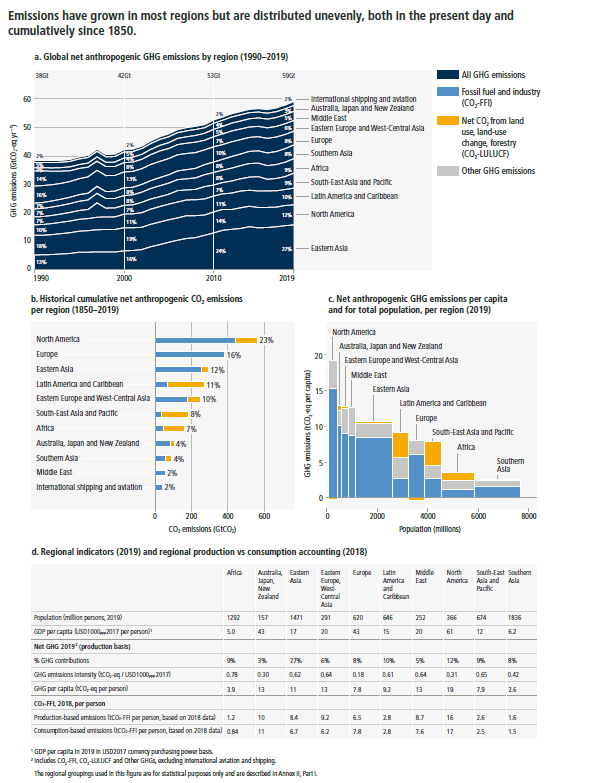

B.3 Regional contributions17 to global GHG emissions continue to differ widely. Variations in regional, and national per capita emissions partly reflect different development stages, but they also vary widely at similar income levels. The 10% of households with the highest per capita emissions contribute a disproportionately large share of global household GHG emissions. At least 18 countries have sustained GHG emission reductions for longer than 10 years. ( high confidence) Expand Figure SPM.2 Links to chaptersFigure 1.1, Figure 2.9, Figure 2.10, Figure 2.25, 2.2, 2.3, 2.4, 2.5, 2.6, Figure TS.4, Figure TS.5

B.3.1GHG emissions trends over 1990–2019 vary widely across regions and over time, and across different stages of development, as shown in Figure SPM.2. Average global per capita net anthropogenic GHG emissions increased from 7.7 to 7.8 tCO2-eq, ranging from 2.6 tCO2-eq to 19 tCO2-eq across regions. Least developed countries (LDCs) and Small Island Developing States (SIDS) have much lower per capita emissions (1.7 tCO2-eq and 4.6 tCO2-eq, respectively) than the global average (6.9 tCO2-eq), excluding CO2-LULUCF. 18 (high confidence) (Figure SPM.2) {Figure1.2, Figure 2.9, Figure 2.10, 2.2, Figure TS.4}

B.3.2Historical contributions to cumulative net anthropogenic CO2 emissions between 1850 and 2019 vary substantially across regions in terms of total magnitude, but also in terms of contributions to CO2-FFI (1650 ± 73 GtCO2-eq) and net CO2-LULUCF (760 ± 220 GtCO2-eq) emissions. 10Globally, the major share of cumulative CO2-FFI emissions is concentrated in a few regions, while cumulative CO2-LULUCF9 emissions are concentrated in other regions. LDCs contributed less than 0.4% of historical cumulative CO2-FFI emissions between 1850 and 2019, while SIDS contributed 0.5%. (high confidence) (Figure SPM.2) {Figure 2.10, 2.2, TS.3, Figure 2.7}

B.3.3In 2019, around 48% of the global population lives in countries emitting on average more than 6 tCO2-eq per capita, excluding CO2-LULUCF. 35% live in countries emitting more than 9 tCO2-eq per capita. Another 41% live in countries emitting less than 3 tCO2-eq per capita. A substantial share of the population in these low-emitting countries lack access to modern energy services. 19 Eradicating extreme poverty, energy poverty, and providing decent living standards 20 to all in these regions in the context of achieving sustainable development objectives, in the near-term, can be achieved without significant global emissions growth. (high confidence) (Figure SPM.2) {Figure 1.2, 2.2, 2.4, 2.6, 3.7, 4.2, 6.7, Figure TS.4, Figure TS.5}

B.3.4Globally, the 10% of households with the highest per capita emissions contribute 34–45% of global consumption-based household GHG emissions, 21 while the middle 40% contribute 40–53%, and the bottom 50% contribute 13–15%. (high confidence) {2.6, Figure 2.25}

B.3.5At least 18 countries have sustained production-based GHG and consumption-based CO2 emission reductions for longer than 10 years. Reductions were linked to energy supply decarbonisation, energy efficiency gains, and energy demand reduction, which resulted from both policies and changes in economic structure. Some countries have reduced production-based GHG emissions by a third or more since peaking, and some have achieved several years of consecutive reduction rates of around 4% yr –1, comparable to global reductions in scenarios limiting warming to 2°C (>67%) or lower. These reductions have only partly offset global emissions growth. (high confidence) (Figure SPM.2) {Figure TS.4, 2.2, 1.3.2}

Figure SPM.2: Regional GHG emissions, and the regional proportion of total cumulativeproduction-basedCO2 emissions from 1850 to 2019. Panel a shows global net anthropogenic GHG emissions by region (in GtCO2-eq yr –1 (GWP100-AR6)) for the time period 1990–2019. 6Percentage values refer to the contribution of each region to total GHG emissions in each respective time period. The single-year peak of emissions in 1997 was due to higher CO2-LULUCF emissions from a forest and peat fire event in South East Asia. Regions are as grouped in Annex II. Panel b shows the share of historical cumulative net anthropogenic CO2 emissions per region from 1850 to 2019 in GtCO2. This includes CO2 from fossil fuel combustion and industrial processes (CO2-FFI) and net CO2 emissions from land use, land-use change, forestry (CO2-LULUCF). Other GHG emissions are not included. 6CO2-LULUCF emissions are subject to high uncertainties, reflected by a global uncertainty estimate of ±70% (90% confidence interval). Panel c shows the distribution of regional GHG emissions in tonnes CO2-eq per capita by region in 2019. GHG emissions are categorised into: CO2-FFI; net CO2-LULUCF; and other GHG emissions (methane, nitrous oxide, fluorinated gases, expressed in CO2-eq using GWP100-AR6). The height of each rectangle shows per capita emissions, the width shows the population of the region, so that the area of the rectangles refers to the total emissions for each region. Emissions from international aviation and shipping are not included. In the case of two regions, the area for CO2-LULUCF is below the axis, indicating net CO2 removals rather than emissions. CO2-LULUCF emissions are subject to high uncertainties, reflected by a global uncertainty estimate of ±70% (90% confidence interval). Panel d shows population, GDP per person, emission indicators by region in 2019 for percentage GHG contributions, total GHG per person, and total GHG emissions intensity, together with production-based and consumption-based CO2-FFI data, which is assessed in this report up to 2018. Consumption-based emissions are emissions released to the atmosphere in order to generate the goods and services consumed by a certain entity (e.g., region). Emissions from international aviation and shipping are not included. {1.3, Figure 1.2, 2.2, Figure 2.9, Figure 2.10, Figure 2.11, Annex II}

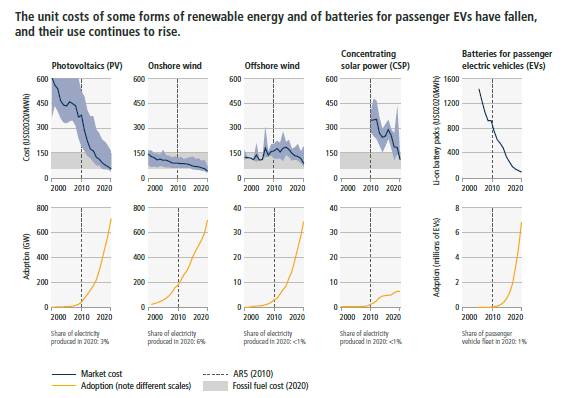

B.4 The unit costs of several low-emission technologies have fallen continuously since 2010. Innovation policy packages have enabled these cost reductions and supported global adoption. Both tailored policies and comprehensive policies addressing innovation systems have helped overcome the distributional, environmental and social impacts potentially associated with global diffusion of low-emission technologies. Innovation has lagged in developing countries due to weaker enabling conditions. Digitalisation can enable emission reductions, but can have adverse side effects unless appropriately governed. (high confidence) Expand Figure SPM.3 Links to chapters2.2, 6.3, 6.4, 7.2, 12.2, 16.2, 16.4, 16.5, Cross-Chapter Box 11 in Chapter 16

Figure SPM.3 | Unit cost reductions and use in some rapidly changing mitigation technologies. The top panel shows global costs per unit of energy (USD per MWh) for some rapidly changing mitigation technologies. Solid blue lines indicate average unit cost in each year. Light blue shaded areas show the range between the 5th and 95th percentiles in each year. Grey shading indicates the range of unit costs for new fossil fuel (coal and gas) power in 2020 (corresponding to USD55–148 per MWh). In 2020, the levelised costs of energy (LCOE) of the four renewable energy technologies could compete with fossil fuels in many places. For batteries, costs shown are for 1 kWh of battery storage capacity; for the others, costs are LCOE, which includes installation, capital, operations, and maintenance costs per MWh of electricity produced. The literature uses LCOE because it allows consistent comparisons of cost trends across a diverse set of energy technologies to be made. However, it does not include the costs of grid integration or climate impacts. Further, LCOE does not take into account other environmental and social externalities that may modify the overall (monetary and non-monetary) costs of technologies and alter their deployment. The bottom panel shows cumulative global adoption for each technology, in GW of installed capacity for renewable energy and in millions of vehicles for battery-electric vehicles. A vertical dashed line is placed in 2010 to indicate the change since AR5. Shares of electricity produced and share of passenger vehicle fleet are indicated in text for 2020 based on provisional data, i.e., percentage of total electricity production (for PV, onshore wind, offshore wind, CSP) and of total stock of passenger vehicles (for EVs). The electricity production share reflects different capacity factors; for example, for the same amount of installed capacity, wind produces about twice as much electricity as solar PV. {2.5, 6.4} Renewable energy and battery technologies were selected as illustrative examples because they have recently shown rapid changes in costs and adoption, and because consistent data are available. Other mitigation options assessed in the report are not included as they do not meet these criteria.

B.4.1From 2010 to 2019, there have been sustained decreases in the unit costs of solar energy (85%), wind energy (55%), and lithium-ion batteries (85%), and large increases in their deployment, e.g., >10× for solar and >100× for electric vehicles (EVs), varying widely across regions (Figure SPM.3). The mix of policy instruments which reduced costs and stimulated adoption includes public R&D, funding for demonstration and pilot projects, and demand pull instruments such as deployment subsidies to attain scale. In comparison to modular small-unit size technologies, the empirical record shows that multiple large-scale mitigation technologies, with fewer opportunities for learning, have seen minimal cost reductions and their adoption has grown slowly. (high confidence) {1.3, 1.5, Figure 2.5, 2.5, 6.3, 6.4, 7.2, 11.3, 12.2, 12.3, 12.6, 13.6, 16.3, 16.4, 16.6}

B.4.2Policy packages tailored to national contexts and technological characteristics have been effective in supporting low-emission innovation and technology diffusion. Appropriately designed policies and governance have helped address distributional impacts and rebound effects. Innovation has provided opportunities to lower emissions and reduce emission growth and created social and environmental co-benefits (high confidence). Adoption of low-emission technologies lags in most developing countries, particularly least developed ones, due in part to weaker enabling conditions, including limited finance, technology development and transfer, and capacity. In many countries, especially those with limited institutional capacities, several adverse side effects have been observed as a result of diffusion of low-emission technology, for example, low-value employment, and dependency on foreign knowledge and suppliers. Low-emission innovation along with strengthened enabling conditions can reinforce development benefits, which can, in turn, create feedbacks towards greater public support for policy. (medium confidence) {9.9, 13.6, 13.7, 16.3, 16.4, 16.5, 16.6, Cross-Chapter Box 12 in Chapter 16, TS.3}

B.4.3Digital technologies can contribute to mitigation of climate change and the achievement of several SDGs (high confidence). For example, sensors, internet of things, robotics, and artificial intelligence can improve energy management in all sectors, increase energy efficiency, and promote the adoption of many low-emission technologies, including decentralised renewable energy, while creating economic opportunities (high confidence). However, some of these climate change mitigation gains can be reduced or counterbalanced by growth in demand for goods and services due to the use of digital devices (high confidence). Digitalisation can involve trade-offs across several SDGs, for example, increasing electronic waste, negative impacts on labour markets, and exacerbating the existing digital divide. Digital technology supports decarbonisation only if appropriately governed (high confidence). {5.3, 10, 12.6, 16.2, Cross-Chapter Box 11 in Chapter 16, TS.5, Box TS.14}

B.5There has been a consistent expansion of policies and laws addressing mitigation since AR5. This has led to the avoidance of emissions that would otherwise have occurred and increased investment in low-GHG technologies and infrastructure. Policy coverage of emissions is uneven across sectors. Progress on the alignment of financial flows towards the goals of the Paris Agreement remains slow and tracked climate finance flows are distributed unevenly across regions and sectors. (high confidence) ExpandLinks to chapters5.6, 13.2, 13.4, 13.5, 13.6, 13.9, 14.3, 14.4, 14.5, Cross-Chapter Box 10 in Chapter 14, 15.3, 15.5

B.5.1The Kyoto Protocol led to reduced emissions in some countries and was instrumental in building national and international capacity for GHG reporting, accounting and emissions markets (high confidence). At least 18 countries that had Kyoto targets for the first commitment period have had sustained absolute emission reductions for at least a decade from 2005, of which two were countries with economies in transition (very high confidence). The Paris Agreement, with near universal participation, has led to policy development and target-setting at national and sub-national levels, in particular in relation to mitigation, as well as enhanced transparency of climate action and support (medium confidence). {14.3, 14.6}

B.5.2The application of diverse policy instruments for mitigation at the national and sub-national levels has grown consistently across a range of sectors (high confidence). By 2020, over 20% of global GHG emissions were covered by carbon taxes or emissions trading systems, although coverage and prices have been insufficient to achieve deep reductions (medium confidence). By 2020, there were ‘direct’ climate laws focused primarily on GHG reductions in 56 countries covering 53% of global emissions (medium confidence). Policy coverage remains limited for emissions from agriculture and the production of industrial materials and feedstocks (high confidence). {5.6, 7.6, 11.5, 11.6, 13.2, 13.6}

B.5.3In many countries, policies have enhanced energy efficiency, reduced rates of deforestation and accelerated technology deployment, leading to avoided and in some cases reduced or removed emissions (high confidence). Multiple lines of evidence suggest that mitigation policies have led to avoided global emissions of several GtCO2-eq yr –1 (medium confidence). At least 1.8 GtCO2-eq yr –1 can be accounted for by aggregating separate estimates for the effects of economic and regulatory instruments. Growing numbers of laws and executive orders have impacted global emissions and were estimated to result in 5.9 GtCO2-eq yr –1 less emissions in 2016 than they otherwise would have been. (medium confidence) (Figure SPM.3) {2.2, 2.8, 6.7, 7.6, 9.9, 10.8, 13.6, Cross-chapter Box 10 in Chapter 14}

B.5.4Annual tracked total financial flows for climate mitigation and adaptation increased by up to 60% between 2013/14 and 2019/20 (in USD2015), but average growth has slowed since 201822 (medium confidence). These financial flows remained heavily focused on mitigation, are uneven, and have developed heterogeneously across regions and sectors (high confidence). In 2018, public and publicly mobilised private climate finance flows from developed to developing countries were below the collective goal under the UNFCCC and Paris Agreement to mobilise USD100 billion per year by 2020 in the context of meaningful mitigation action and transparency on implementation (medium confidence). Public and private finance flows for fossil fuels are still greater than those for climate adaptation and mitigation (high confidence). Markets for green bonds, ESG (environmental, social and governance) and sustainable finance products have expanded significantly since AR5. Challenges remain, in particular around integrity and additionality, as well as the limited applicability of these markets to many developing countries. (high confidence){Box 15.4, 15.3, 15.5, 15.6, Box 15.7}

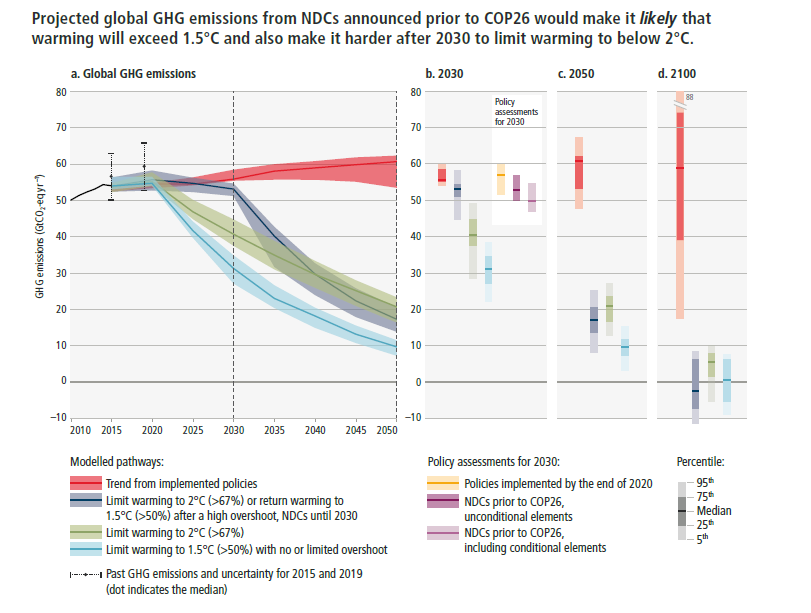

B.6 Global GHG emissions in 2030 associated with the implementation of Nationally Determined Contributions (NDCs) announced prior to COP2623 would make it likely that warming will exceed 1.5°C during the 21st century. 24 Likely limiting warming to below 2°C would then rely on a rapid acceleration of mitigation efforts after 2030. Policies implemented by the end of 202025 are projected to result in higher global GHG emissions than those implied by NDCs. (high confidence) Expand Figure SPM.4 Links to chapters3.3, 3.5, 4.2, Cross-Chapter Box 4 in Chapter 4

B.6.1Policies implemented by the end of 2020 are projected to result in higher global GHG emissions than those implied by NDCs, indicating an implementation gap. A gap remains between global GHG emissions in 2030 associated with the implementation of NDCs announced prior to COP26 and those associated with modelled mitigation pathways assuming immediate action (for quantification see Table SPM.1). 26 The magnitude of the emissions gap depends on the global warming level considered and whether only unconditional or also conditional elements of NDCs 27 are considered. 28 (high confidence) {3.5, 4.2, Cross-Chapter Box 4 in Chapter 4}

Table SPM.1 | Projected global emissions in 2030 associated with policies implemented by the end of 2020 and NDCs announced prior to COP26, and associated emissions gaps. *Emissions projections for 2030 and absolute differences in emissions are based on emissions of 52–56 GtCO2-eq yr –1 in 2019 as assumed in underlying model studies. (medium confidence) {4.2, Table 4.3, Cross-Chapter Box 4 in Chapter 4}

Implied by policies implemented by the end of 2020 (GtCO2-eq yr –1) | Implied by NDCs announced prior to COP26 | ||

Unconditional elements (GtCO2-eq yr –1) | Including conditional elements (GtCO2-eq yr –1) | ||

Median projected global emissions (min–max)* | 57 [52–60] | 53 [50–57] | 50 [47–55] |

Implementation gap between implemented policies and NDCs (median) | 4 | 7 | |

Emissions gap between NDCs and pathways that limit warming to 2°C (>67%) with immediate action | 10–16 | 6–14 | |

Emissions gap between NDCs and pathways that limit warming to 1.5°C (>50%) with no or limited overshoot with immediate action | 19–26 | 16–23 | |

B.6.2Global emissions in 2030 associated with the implementation of NDCs announced prior to COP26 are lower than the emissions implied by the original NDCs 29 (high confidence). The original emissions gap has fallen by about 20% to one-third relative to pathways that limit warming to 2°C (>67%) with immediate action (category C3a in Table SPM.2), and by about 15–20% relative to pathways limiting warming to 1.5°C (>50%) with no or limited overshoot (category C1 in Table SPM.2) (medium confidence). (Figure SPM.4) {3.5, 4.2, Cross-Chapter Box 4 in Chapter 4}

B.6.3Modelled global emission pathways consistent with NDCs announced prior to COP26 that limit warming to 2°C (>67%) (category C3b in Table SPM.2) imply annual average global GHG emissions reduction rates of 0–0.7 GtCO2-eq yr –1 during the decade 2020–2030, with an unprecedented acceleration to 1.4–2.0 GtCO2-eq yr –1 during 2030–2050 (medium confidence). Continued investments in unabated high-emitting infrastructure and limited development and deployment of low-emitting alternatives prior to 2030 would act as barriers to this acceleration and increase feasibility risks (high confidence). {3.3, 3.5, 3.8, Cross-Chapter Box 5 in Chapter 4}

B.6.4Modelled global emission pathways consistent with NDCs announced prior to COP26 will likely exceed 1.5°C during the 21st century. Those pathways that then return warming to 1.5°C by 2100 with a likelihood of 50% or greater imply a temperature overshoot of 0.15°C–0.3°C (42 pathways in category C2 in Table SPM.2). In such pathways, global cumulative net-negative CO2 emissions are –380 [–860 to –200] GtCO230 in the second half of the century, and there is a rapid acceleration of other mitigation efforts across all sectors after 2030. Such overshoot pathways imply increased climate-related risk, and are subject to increased feasibility concerns, 31 and greater social and environmental risks, compared to pathways that limit warming to 1.5°C (>50%) with no or limited overshoot. (high confidence) (Figure SPM.4, Table SPM.2) {3.3, 3.5, 3.8, 12.3; AR6 WGII SPM B.6}

Figure SPM.4: Global GHG emissions of modelled pathways (funnels in Panel a, and associated bars in Panels b, c, d) and projected emission outcomes from near-termpolicy assessments for 2030 (Panel b). Panel a shows global GHG emissions over 2015–2050 for four types of assessed modelled global pathways:

–Trend from implemented policies: Pathways with projected near-term GHG emissions in line with policies implemented until the end of 2020 and extended with comparable ambition levels beyond 2030 (29 scenarios across categories C5–C7, Table SPM.2).

–Limit to 2°C (>67%) or return warming to 1.5°C (>50%) after a high overshoot, NDCs until 2030: Pathways with GHG emissions until 2030 associated with the implementation of NDCs announced prior to COP26, followed by accelerated emissions reductions likely to limit warming to 2°C (C3b, Table SPM.2) or to return warming to 1.5°C with a probability of 50% or greater after high overshoot (subset of 42 scenarios from C2, Table SPM.2).

–Limit to 2°C (>67%) with immediate action: Pathways that limit warming to 2°C (>67%) with immediate action after 202026 (C3a, Table SPM.2).

–Limit to 1.5°C (>50%) with no or limited overshoot: Pathways limiting warming to 1.5°C with no or limited overshoot (C1, Table SPM.2 C1). All these pathways assume immediate action after 2020.

Past GHG emissions for 2010–2015 used to project global warming outcomes of the modelled pathways are shown by a black line 32 and past global GHG emissions in 2015 and 2019 as assessed in Chapter 2 are shown by whiskers. Panels b, c and d show snapshots of the GHG emission ranges of the modelled pathways in 2030, 2050, and 2100, respectively. Panel b also shows projected emissions outcomes from near-term policy assessments in 2030 from Chapter 4.2 (Tables 4.2 and 4.3; median and full range). GHG emissions are in CO2-equivalent using GWP100 from AR6 WGI. {3.5, 4.2, Table 4.2, Table 4.3, Cross-Chapter Box 4 in Chapter 4}

B.7Projected cumulative future CO2 emissions over the lifetime of existing and currently planned fossil fuel infrastructure without additional abatement exceed the total cumulative net CO2 emissions in pathways that limit warming to 1.5°C (>50%) with no or limited overshoot. They are approximately equal to total cumulative net CO2 emissions in pathways that limit warming to 2°C (>67%). (high confidence)ExpandLinks to chapters2.7, 3.3

B.7.1If historical operating patterns are maintained, 33 and without additional abatement, 34 estimated cumulative future CO2 emissions from existing fossil fuel infrastructure, the majority of which is in the power sector, would, from 2018 until the end of its lifetime, amount to 660 [460–890] GtCO2. They would amount to 850 [600–1100] GtCO2 when unabated emissions from currently planned infrastructure in the power sector is included. These estimates compare with cumulative global net CO2 emissions from all sectors of 510 [330–710] GtCO2 until the time of reaching net zero CO2 emissions 35 in pathways that limit warming to 1.5°C (>50%) with no or limited overshoot, and 890 [640–1160] GtCO2 in pathways that limit warming to 2°C (>67%). (high confidence) (Table SPM.2) {2.7, Figure 2.26, Figure TS.8}

B.7.2In modelled global pathways that limit warming to 2°C (>67%) or lower, most remaining fossil fuel CO2 emissions until the time of global net zero CO2 emissions are projected to occur outside the power sector, mainly in industry and transport. Decommissioning and reduced utilisation of existing fossil fuel-based power sector infrastructure, retrofitting existing installations with CCS, 36 switches to low-carbon fuels, and cancellation of new coal installations without CCS are major options that can contribute to aligning future CO2 emissions from the power sector with emissions in the assessed global modelled least-cost pathways. The most appropriate strategies will depend on national and regional circumstances, including enabling conditions and technology availability. (high confidence) (Box SPM.1) {Table 2.7, 2.7, 3.4, 6.3, 6.5, 6.7}

C. System Transformations to Limit Global Warming

C.1Global GHG emissions are projected to peak between 2020 and at the latest before 2025 in global modelled pathways that limit warming to 1.5°C (>50%) with no or limited overshoot and in those that limit warming to 2°C (>67%) and assume immediate action (see Table SPM.2 footnote i). 37 In both types of modelled pathways, rapid and deep GHG emissions reductions follow throughout 2030, 2040 and 2050 (high confidence). Without a strengthening of policies beyond those that are implemented by the end of 2020, GHG emissions are projected to rise beyond 2025, leading to a median global warming of 3.2 [2.2 to 3.5] °C by 210038,39 (medium confidence).Expand Table SPM.2 Figure SPM.4 Figure SPM.5Links to chapters3.3, 3.4

Table SPM.2 Figure SPM.4 Figure SPM.5Links to chapters3.3, 3.4

C.1.1Net global GHG emissions are projected to fall from 2019 levels by 27% [13–45%] by 2030 and 63% [52–76%]40 by 2050 in global modelled pathways that limit warming to 2°C (>67%) and assuming immediate action (category C3a, Table SPM.2). This compares with reductions of 43% [34–60%] by 2030 and 84% [73–98%] by 2050 in pathways that limit warming to 1.5°C (>50%) with no or limited overshoot (C1, Table SPM.2) (high confidence). 41 In modelled pathways that return warming to 1.5°C (>50%) after a high overshoot, 42 GHG emissions are reduced by 23% [0–44%] in 2030 and by 75% [62–91%] in 2050 (C2, Table SPM.2) (high confidence). Modelled pathways that are consistent with NDCs announced prior to COP26 until 2030 and assume no increase in ambition thereafter have higher emissions, leading to a median global warming of 2.8 [2.1–3.4] °C by 2100 (medium confidence). 23 (Figure SPM.4) {3.3}

Table SPM.2 | Key characteristics of the modelled global emissions pathways. Summary of projected CO2 and GHG emissions, projected net zero timings and the resulting global warming outcomes. Pathways are categorised (rows), according to their likelihood of limiting warming to different peak warming levels (if peak temperature occurs before 2100) and 2100 warming levels. Values shown are for the median [p50] and 5th–95th percentiles [p5–p95], noting that not all pathways achieve net zero CO2 or GHGs.

p50 [p5–p95]a | GHG emissions (GtCO2-eqyr–1) g | GHG emissions reductions from 2019 (%) h | Emissions milestonesi, j | Cumulative CO2 emissions (GtCO2) m | Cumulativenet-negativeCO2 emissions (GtCO2) | Global mean temperature changes 50% probability (°C) n | Likelihood of peak global warming staying below (%) o | |||||||||||||

Categoryb, c, d[# pathways] | Category/subset label | WGI SSP & WGIII IPs/IMPsalignment e, f | 2030 | 2040 | 2050 | 2030 | 2040 | 2050 | Peak CO2 emissions (% peak before 2100) | Peak GHG emissions (% peak before 2100) | Net zeroCO2(%net zeropathways) | Net zeroGHGs (%net zeropathways) k, l | 2020 tonet zeroCO2 | 2020–2100 | Year of net zeroCO2to 2100 | at peak warming | 2100 | <1.5°C | <2.0°C | <3.0°C |

Modelled global emissions pathways categorised by projected global warming levels (GWL). Detailed likelihood definitions are provided in SPM Box 1. The five illustrative scenarios (SSPx-yy) considered by AR6 WGI and the Illustrative (Mitigation) Pathways assessed in WGIII are aligned with the temperature categories and are indicated in a separate column. Global emission pathways contain regionally differentiated information. This assessment focuses on their global characteristics. | Projected median annual GHG emissions in the year across the scenarios, with the 5th–95th percentile in brackets. Modelled GHG emissions in 2019: 55 [53–58]GtCO2-eq. | Projected median GHG emissions reductions of pathways in the year across the scenarios compared to modelled 2019, with the 5th–95th percentile in brackets. Negative numbers indicate increase in emissions compared to 2019. | Median 5-year intervals at which projected CO2& GHG emissions peak, with the 5th–95th percentile interval in square brackets. Percentage of peaking pathways is denoted in round brackets. Three dots (…) denotes emissions peak in 2100 or beyond for that percentile. | Median 5-year intervals at which projected CO2& GHG emissions of pathways in this category reachnet zero, with the 5th–95th percentile interval in square brackets. Percentage of net zero pathways is denoted in round brackets. Three dots (…) denotes net zero not reached for that percentile. | Median cumulative net CO2 emissions across the projected scenarios in this category until reachingnet zeroor until 2100, with the5th–95thpercentile interval in square brackets. | Median cumulativenet-negativeCO2 emissions between the year of net zeroCO2and 2100. Morenet-negativeresults in greater temperature declines after peak. | Projected temperature change of pathways in this category (50% probability across the range of climate uncertainties), relative to 1850–1900, at peak warming and in 2100, for the median value across the scenarios and the 5th–95th percentile interval in square brackets. | Median likelihood that the projected pathways in this category stay below a given global warming level, with the 5th–95th percentile interval in square brackets. | ||||||||||||

C1 [97] | limit warming to 1.5°C (>50%) with no or limited overshoot | 31 [21–36] | 17 [6–23] | 9 [1–15] | 43 [34–60] | 69 [58–90] | 84 [73–98] | 2020–2025 (100%) [2020–2025] | 2050–2055 (100%) [2035–2070] | 2095–2100 (52%) [2050–...] | 510 [330–710] | 320 [–210 to 570] | –220 [–660 to –20] | 1.6 [1.4–1.6] | 1.3 [1.1–1.5] | 38 [33–58] | 90 [86–97] | 100 [99–100] | ||

C1a [50] | … withnet zeroGHGs | SSP1–1.9, SP LD | 33 [22–37] | 18 [6–24] | 8 [0–15] | 41 [31–59] | 66 [58–89] | 85 [72–100] | 2070–2075 (100%) [2050–2090] | 550 [340–760] | 160 [–220 to 620] | –360 [–680 to –140] | 1.6 [1.4–1.6] | 1.2 [1.1–1.4] | 38 [34–60] | 90 [85–98] | 100 [99–100] | |||

C1b [47] | … without net zeroGHGs | Ren | 29 [21–36] | 16 [7–21] | 9 [4–13] | 48 [35–61] | 70 [62–87] | 84 [76–93] | …–… [0%] | 460 [320–590] | 360 [10–540] | –60 [–440 to 0] | 1.6 [1.5–1.6] | 1.4 [1.3–1.5] | 37 [33–56] | 89 [87–96] | 100 [99–100] | |||

[…–…] | ||||||||||||||||||||

C2 [133] | return warming to 1.5°C (>50%) after a high overshoot | Neg | 42 [31–55] | 25 [17–34] | 14 [5–21] | 23 [0–44] | 55 [40–71] | 75 [62–91] | 2020–2025 (100%) | 2055–2060 (100%) [2045–2070] | 2070–2075 (87%) [2055–...] | 720 [530–930] | 400 [–90 to 620] | –360 [–680 to –60] | 1.7 [1.5–1.8] | 1.4 [1.2–1.5] | 24 [15–42] | 82 [71–93] | 100 [99–100] | |

[2020–2030] | [2020–2025] | |||||||||||||||||||

C3 [311] | limit warming to 2°C (>67%) | 44 [32–55] | 29 [20–36] | 20 [13–26] | 21 [1–42] | 46 [34–63] | 64 [53–77] | 2020–2025 (100%) | 2070–2075 (93%) [2055–...] | ...–... (30%) [2075–...] | 890 [640–1160] | 800 [510–1140] | –40 [–290 to 0] | 1.7 [1.6–1.8] | 1.6 [1.5–1.8] | 20 [13–41] | 76 [68–91] | 99 [98–100] | ||

[2020–2030] | [2020–2025] | |||||||||||||||||||

C3a [204] | … with action starting in 2020 | SSP1–2.6 | 40 [30–49] | 29 [21–36] | 20 [14–27] | 27 [13–45] | 47 [35–63] | 63 [52–76] | 2020–2025 (100%) [2020–2025] | 2070–2075 (91%) [2055–...] | ...–... (24%) [2080–...] | 860 [640–1180] | 790 [480–1150] | –30 [–280 to 0] | 1.7 [1.6–1.8] | 1.6 [1.5–1.8] | 21 [14–42] | 78 [69–91] | 100 [98–100] | |

C3b [97] | … NDCs until 2030 | GS | 52 [47–56] | 29 [20–36] | 18 [10–25] | 5 [0–14] | 46 [34–63] | 68 [56–82] | 2020–2025 (100%) [2020–2030] | 2065–2070 (97%) [2055–2090] | ...–... (41%) [2075–...] | 910 [720–1150] | 800 [560–1050] | –60 [–300 to 0] | 1.8 [1.6–1.8] | 1.6 [1.5–1.7] | 17 [12–35] | 73 [67–87] | 99 [98–99] | |

C4 [159] | limit warming to 2°C (>50%) | 50 [41–56] | 38 [28–44] | 28 [19–35] | 10 [0–27] | 31 [20–50] | 49 [35–65] | 2080–2085 (86%) [2065–...] | ...–... (31%) [2075–...] | 1210 [970–1490] | 1160 [700–1490] | –30 [–390 to 0] | 1.9 [1.7–2.0] | 1.8 [1.5–2.0] | 11 [7–22] | 59 [50–77] | 98 [95–99] | |||

C5 [212] | limit warming to 2.5°C (>50%) | 52 [46–56] | 45 [37–53] | 39 [30–49] | 6 [–1 to 18] | 18 [4–33] | 29 [11–48] | ...–... (41%) [2080–...] | ...–... (12%) [2090–...] | 1780 [1400–2360] | 1780 [1260–2360] | 0 [–160 to 0] | 2.2 [1.9–2.5] | 2.1 [1.9–2.5] | 4 [0–10] | 37 [18–59] | 91 [83–98] | |||

C6 [97] | limit warming to 3°C (>50%) | SSP2–4.5 ModAct | 54 [50–62] | 53 [48–61] | 52 [45–57] | 2 [–10 to 11] | 3 [–14 to 14] | 5 [–2 to 18] | 2030–2035 (96%) | 2020–2025 (97%) | nonet zero | nonet zero | 2790 [2440–3520] | nonet zero | temperaturedoes not peak by 2100 | 2.7 [2.4–2.9] | 0 [0–0] | 8 [2–18] | 71 [53–88] | |

[2020–2090] | ||||||||||||||||||||

C7 [164] | limit warming to 4°C (>50%) | SSP3–7.0 CurPol | 62 [53–69] | 67 [56–76] | 70 [58–83] | –11 [–18 to 3] | –19 [–31 to 1] | –24 [–41 to –2] | 2085–2090 (57%) | 2090–2095 (56%) | 4220 [3160–5000] | 3.5 [2.8–3.9] | 0 [0–0] | 0 [0–2] | 22 [7–60] | |||||

[2040–...] | ||||||||||||||||||||

C8 [29] | exceed warming of 4°C (≥50%) | SSP5–8.5 | 71 [69–81] | 80 [78–96] | 88 [82–112] | –20 [–34 to –17] | –35 [–65 to –29] | –46 [–92 to –36] | 2080–2085 (90%) [2070–...] | 5600 | 4.2 [3.7–5.0] | 0 [0–0] | 0 [0–0] | 4 [0–11] | ||||||

[4910–7450] | ||||||||||||||||||||

aValues in the table refer to the 50th and [5th–95th] percentile values across the pathways falling within a given category as defined in Box SPM.1. For emissions-related columns these values relate to the distribution of all the pathways in that category. Harmonised emissions values are given for consistency with projected global warming outcomes using climate emulators. Based on the assessment of climate emulators in AR6 WGI (WG1 Chapter 7, Box 7.1), two climate emulators are used for the probabilistic assessment of the resulting warming of the pathways. For the ‘Temperature change’ and ‘Likelihood’ columns, the single upper-row values represent the 50th percentile across the pathways in that category and the median [50th percentile] across the warming estimates of the probabilistic MAGICC climate model emulator. For the bracketed ranges, the median warming for every pathway in that category is calculated for each of the two climate model emulators (MAGICC and FaIR). Subsequently, the 5th and 95th percentile values across all pathways for each emulator are calculated. The coolest and warmest outcomes (i.e., the lowest p5 of two emulators, and the highest p95, respectively) are shown in square brackets. These ranges therefore cover both the uncertainty of the emissions pathways as well as the climate emulators’ uncertainty.

bFor a description of pathways categories see Box SPM.1.

cAll global warming levels are relative to 1850–1900. (See footnote n below and Box SPM.145 for more details.)

dC3 pathways are sub-categorised according to the timing of policy action to match the emissions pathways in Figure SPM.4. Two pathways derived from a cost-benefit analysis have been added to C3a, whilst 10 pathways with specifically designed near-term action until 2030, whose emissions fall below those implied by NDCs announced prior to COP26, are not included in either of the two subsets.

eAlignment with the categories of the illustrative SSP scenarios considered in AR6 WGI, and the Illustrative (Mitigation) Pathways (IPs/IMPs) of WGIII. The IMPs have common features such as deep and rapid emissions reductions, but also different combinations of sectoral mitigation strategies. See Box SPM.1 for an introduction of the IPs and IMPs, and Chapter 3 for full descriptions. {3.2, 3.3, Annex III.II.4}

f The Illustrative Mitigation Pathway ‘Neg’ has extensive use of carbon dioxide removal (CDR) in the AFOLU, energy and the industry sectors to achieve net negative emissions. Warming peaks around 2060 and declines to below 1.5°C (50% likelihood) shortly after 2100. Whilst technically classified as C3, it strongly exhibits the characteristics of C2 high-overshoot pathways, hence it has been placed in the C2 category. See Box SPM.1 for an introduction of the IPs and IMPs.

gThe 2019 range of harmonised GHG emissions across the pathways [53–58 GtCO2-eq] is within the uncertainty ranges of 2019 emissions assessed in Chapter 2 [53–66 GtCO2-eq]. 49 (Figure SPM.1, Figure SPM.2, Box SPM.1)

hRates of global emission reduction in mitigation pathways are reported on a pathway-by-pathway basis relative to harmonised modelled global emissions in 2019 rather than the global emissions reported in SPM Section B and Chapter 2; this ensures internal consistency in assumptions about emission sources and activities, as well as consistency with temperature projections based on the physical climate science assessment by WGI. 49{Annex III.II.2.5}. Negative values (e.g., in C7, C8) represent an increase in emissions.

iEmissions milestones are provided for five-year intervals in order to be consistent with the underlying five-year time-step data of the modelled pathways. Peak emissions (CO2 and GHGs) are assessed for five-year reporting intervals starting in 2020. The interval 2020–2025 signifies that projected emissions peak as soon as possible between 2020 and at latest before 2025. The upper five-year interval refers to the median interval within which the emissions peak or reach net zero. Ranges in square brackets underneath refer to the range across the pathways, comprising the lower bound of the 5th percentile five-year interval and the upper bound of the 95th percentile five-year interval. Numbers in round brackets signify the fraction of pathways that reach specific milestones.

jPercentiles reported across all pathways in that category include those that do not reach net zero before 2100 (fraction of pathways reaching net zero is given in round brackets). If the fraction of pathways that reach net zero before 2100 is lower than the fraction of pathways covered by a percentile (e.g., 0.95 for the 95th percentile), the percentile is not defined and denoted with ‘…’. The fraction of pathways reaching net zero includes all with reported non-harmonised, and/or harmonised emissions profiles that reach net zero. Pathways were counted when at least one of the two profiles fell below 100 MtCO2 yr –1 until 2100.

kThe timing of net zero is further discussed in SPM C2.4 and Cross-Chapter Box 3 in Chapter 3 on net zero CO2 and net zero GHG emissions.

lFor cases where models do not report all GHGs, missing GHG species are infilled and aggregated into a Kyoto basket of GHG emissions in CO2-eq defined by the 100-year global warming potential. For each pathway, reporting of CO2, CH4, and N2O emissions was the minimum required for the assessment of the climate response and the assignment to a climate category. Emissions pathways without climate assessment are not included in the ranges presented here. {See Annex III.II.5}

mCumulative emissions are calculated from the start of 2020 to the time of net zero and 2100, respectively. They are based on harmonised net CO2 emissions, ensuring consistency with the WGI assessment of the remaining carbon budget. 50{Box 3.4}

nGlobal mean temperature change for category (at peak, if peak temperature occurs before 2100, and in 2100) relative to 1850–1900, based on the median global warming for each pathway assessed using the probabilistic climate model emulators calibrated to the AR6 WGI assessment. 12 (See also Box SPM.1) {Annex III.II.2.5; WGI Cross-Chapter Box 7.1}

oProbability of staying below the temperature thresholds for the pathways in each category, taking into consideration the range of uncertainty from the climate model emulators consistent with the AR6 WGI assessment. The probabilities refer to the probability at peak temperature. Note that in the case of temperature overshoot (e.g., category C2 and some pathways in C1), the probabilities of staying below at the end of the century are higher than the probabilities at peak temperature.

C.1.2In modelled pathways that limit warming to 2°C (>67%) assuming immediate action, global net CO2 emissions are reduced compared to modelled 2019 emissions by 27% [11–46%] in 2030 and by 52% [36–70%] in 2040; and global CH4 emissions are reduced by 24% [9–53%] in 2030 and by 37% [20–60%] in 2040. In pathways that limit warming to 1.5°C (>50%) with no or limited overshoot global net CO2 emissions are reduced compared to modelled 2019 emissions by 48% [36–69%] in 2030 and by 80% [61–109%] in 2040; and global CH4 emissions are reduced by 34% [21–57%] in 2030 and 44% [31–63%] in 2040. There are similar reductions of non-CO2 emissions by 2050 in both types of pathways: CH4 is reduced by 45% [25–70%]; N2O is reduced by 20% [–5 to +55%]; and F-gases are reduced by 85% [20–90%]. 43 Across most modelled pathways, this is the maximum technical potential for anthropogenic CH4 reductions in the underlying models (high confidence). Further emissions reductions, as illustrated by the IMP-SP pathway, may be achieved through changes in activity levels and/or technological innovations beyond those represented in the majority of the pathways (medium confidence). Higher emissions reductions of CH4 could further reduce peak warming. (high confidence) (Figure SPM.5) {3.3}

C.1.3In modelled pathways consistent with the continuation of policies implemented by the end of 2020, GHG emissions continue to rise, leading to global warming of 3.2 [2.2–3.5] °C by 2100 (within C5–C7, Table SPM.2) (medium confidence). Pathways that exceed warming of >4°C (≥50%) (C8, SSP5-8.5, Table SPM.2) would imply a reversal of current technology and/or mitigation policy trends (medium confidence). Such warming could occur in emission pathways consistent with policies implemented by the end of 2020 if climate sensitivity is higher than central estimates (high confidence). (Table SPM.2, Figure SPM.4) {3.3, Box 3.3}

C.1.4Global modelled pathways falling into the lowest temperature category of the assessed literature (C1, Table SPM.2) are on average associated with a higher median peak warming in AR6 compared to pathways in the same category in SR1.5. In the modelled pathways in AR6, the likelihood of limiting warming to 1.5°C has on average declined compared to SR1.5. This is because GHG emissions have risen since 2017, and many recent pathways have higher projected emissions by 2030, higher cumulative net CO2 emissions and slightly later dates for reaching net zero CO2 or net zero GHG emissions. High mitigation challenges, for example, due to assumptions of slow technological change, high levels of global population growth, and high fragmentation as in the Shared Socio-economic Pathway SSP3, may render modelled pathways that limit warming to 2°C (>67%) or lower infeasible. (medium confidence) (Table SPM.2, Box SPM.1) {3.3, 3.8, Annex III Figure II.1, Annex III Figure II.3}

Box SPM.1 | Assessment of Modelled Global Emission Scenarios

A wide range of modelled global emission pathways and scenarios from the literature is assessed in this report, including pathways and scenarios with and without mitigation. 44 Emissions pathways and scenarios project the evolution of GHG emissions based on a set of internally consistent assumptions about future socio-economic conditions and related mitigation measures. 45 These are quantitative projections and are neither predictions nor forecasts. Around half of all modelled global emission scenarios assume cost-effective approaches that rely on least-cost emission abatement options globally. The other half look at existing policies and regionally and sectorally differentiated actions. Most do not make explicit assumptions about global equity, environmental justice or intra-regional income distribution. Global emission pathways, including those based on cost-effective approaches, contain regionally differentiated assumptions and outcomes, and have to be assessed with the careful recognition of these assumptions. This assessment focuses on their global characteristics. The majority of the assessed scenarios (about 80%) have become available since the SR1.5, but some were assessed in that report. Scenarios with and without mitigation were categorised based on their projected global warming over the 21st century, following the same scheme as in the SR1.5 for warming up to and including 2°C. {1.5, 3.2, 3.3, Annex III.II.2, Annex III.II.3}

Scenario categories are defined by their likelihood of exceeding global warming levels (at peak and in 2100) and referred to in this report as follows: 46 , 47

•Category C1 comprises modelled scenarios that limit warming to 1.5°C in 2100 with a likelihood of greater than 50%, and reach or exceed warming of 1.5°C during the 21st century with a likelihood of 67% or less. In this report, these scenarios are referred to as scenarios that limit warming to 1.5°C (>50%) with no or limited overshoot. Limited overshoot refers to exceeding 1.5°C global warming by up to about 0.1°C and for up to several decades. 48

•Category C2 comprises modelled scenarios that limit warming to 1.5°C in 2100 with a likelihood of greater than 50%, and exceed warming of 1.5°C during the 21st century with a likelihood of greater than 67%. In this report, these scenarios are also referred to as scenarios that return warming to 1.5°C (>50%) after a high overshoot. High overshoot refers to temporarily exceeding 1.5°C global warming by 0.1°C–0.3°C for up to several decades.

•Category C3 comprises modelled scenarios that limit peak warming to 2°C throughout the 21st century with a likelihood of greater than 67%. In this report, these scenarios are also referred to as scenarios that limit warming to 2°C (>67%).

•Categories C4, C5, C6 and C7 comprise modelled scenarios that limit warming to 2°C, 2.5°C, 3°C, 4°C, respectively, throughout the 21st century with a likelihood of greater than 50%. In some scenarios in C4 and many scenarios in C5–C7, warming continues beyond the 21st century.

•Category C8 comprises modelled scenarios that exceed warming of 4°C during the 21st century with a likelihood of 50% or greater. In these scenarios warming continues to rise beyond the 21st century.

Categories of modelled scenarios are distinct and do not overlap; they do not contain categories consistent with lower levels of global warming, for example, the category of C3 scenarios that limit warming to 2°C (>67%) does not include the C1 and C2 scenarios that limit or return warming to 1.5°C (>50%). Where relevant, scenarios belonging to the group of categories C1–C3 are referred to in this report as scenarios that limit warming to 2°C (>67%) or lower.

Methods to project global warming associated with the scenarios were updated to ensure consistency with the AR6 WGI assessment of physical climate science. 49 {3.2, Annex III.II.2.5; AR6 WGI Cross-Chapter Box 7.1}

These updated methods affect the categorisation of some scenarios. On average across scenarios, peak global warming is projected to be lower by up to about 0.05 [±0.1]°C than if the same scenarios were evaluated using the SR1.5 methodology, and global warming in 2100 is projected to be lower by about 0.1 [±0.1]°C. {Annex III.II.٢.٥.١, Annex III Figure II.٣}

Resulting changes to the emission characteristics of scenario categories described in Table SPM.2 interact with changes in the characteristics of the wider range of emission scenarios published since the SR1.5. Proportionally more scenarios assessed in AR6 are designed to limit temperature overshoot and more scenarios limit large-scale net negative CO2 emissions than in SR1.5. As a result, AR6 scenarios in the lowest temperature category (C1) generally reach net zero GHG emissions later in the 21st century than scenarios in the same category assessed in SR1.5, and about half do not reach net zero GHG by 2100. The rate of decline of GHG emissions in the near term by 2030 in category C1 scenarios is very similar to the assessed rate in SR1.5, but absolute GHG emissions of category C1 scenarios in AR6 are slightly higher in 2030 than in SR1.5, since the reductions start from a higher emissions level in 2020. (Table SPM.2) {Annex III, 2.5, 3.2, 3.3}

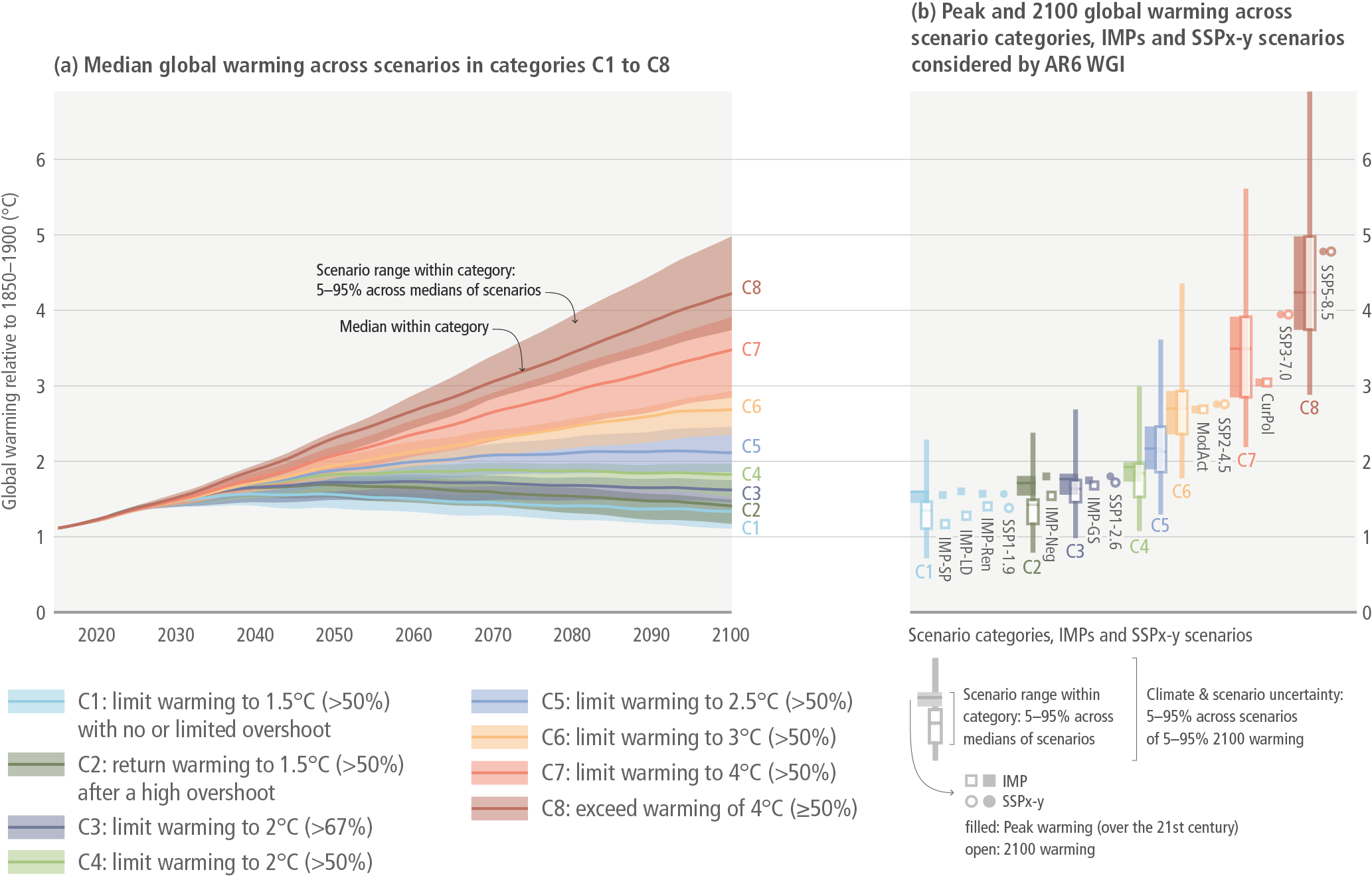

The large number of global emissions scenarios assessed, including 1202 scenarios with projected global warming outcomes using climate emulators, come from a wide range of modelling approaches. They include the five illustrative scenarios (Shared Socio-economic Pathways; SSPs) assessed by WGI for their climate outcomes but cover a wider and more varied set in terms of assumptions and modelled outcomes. For this assessment, Illustrative Mitigation Pathways (IMPs) were selected from this larger set to illustrate a range of different mitigation strategies that would be consistent with different warming levels. The IMPs illustrate pathways that achieve deep and rapid emissions reductions through different combinations of mitigation strategies. The IMPs are not intended to be comprehensive and do not address all possible themes in the underlying report. They differ in terms of their focus, for example, placing greater emphasis on renewables (IMP-Ren), deployment of carbon dioxide removal that results in net negative global GHG emissions (IMP-Neg), and efficient resource use as well as shifts in consumption patterns globally, leading to low demand for resources, while ensuring a high level of services and satisfying basic needs (IMP-LD) (Figure SPM.5). Other IMPs illustrate the implications of a less rapid introduction of mitigation measures followed by a subsequent gradual strengthening (IMP-GS), and how shifting global pathways towards sustainable development, including by reducing inequality, can lead to mitigation (IMP-SP). The IMPs reach different climate goals as indicated in Table SPM.2 and Box SPM.1, Figure 1. {1.5, 3.1, 3.2, 3.3, 3.6, Figure 3.7, Figure 3.8, Box 3.4, Annex III.II.2.4}

Box SPM.1, Figure 1 | Projected global mean warming of the ensemble of modelled scenarios included in the climate categories C1–C8 and IMPs (based on emulators calibrated to the WGI assessment), as well as five illustrative scenarios (SSPx-y) as considered by AR6 WGI. Panel a shows the p5–p95 range of projected median warming across global modelled pathways within a category, with the category medians (line). Panel b shows the peak and 2100 emulated temperature outcomes for the categories C1 to C8 and for IMPs, and the five illustrative scenarios (SSPx-y) as considered by AR6 WGI. The boxes show the p5–p95 range within each scenario category, as in panel a. The combined p5–p95 range across scenarios and the climate uncertainty for each category C1–C8 is also shown for 2100 warming (thin vertical lines). (Table SPM.2) {Figure 3.11; AR6 WGI Figure SPM.8}

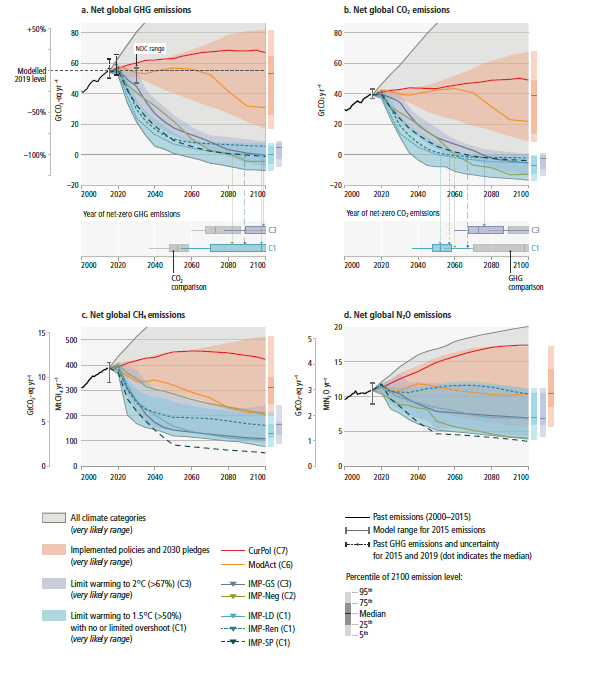

C.2Global net zero CO2 emissions are reached in the early 2050s in modelled pathways that limit warming to 1.5°C (>50%) with no or limited overshoot, and around the early 2070s in modelled pathways that limit warming to 2°C (>67%). Many of these pathways continue to net negative CO2 emissions after the point of net zero. These pathways also include deep reductions in other GHG emissions. The level of peak warming depends on cumulative CO2 emissions until the time of net zero CO2 and the change in non-CO2 climate forcers by the time of peaking. Deep GHG emissions reductions by 2030 and 2040, particularly reductions of methane emissions, lower peak warming, reduce the likelihood of overshooting warming limits and lead to less reliance on net negative CO2 emissions that reverse warming in the latter half of the century. Reaching and sustaining global net zero GHG emissions results in a gradual decline in warming. (high confidence)Expand Table SPM.2 Links to chapters3.3, 3.5, Box 3.4, Cross-Chapter Box 3 in Chapter 3, AR6 WGI SPM D1.8

C.2.1Modelled global pathways limiting warming to 1.5°C (>50%) with no or limited overshoot are associated with projected cumulative net CO2 emissions 50 until the time of net zero CO2 of 510 [330–710] GtCO2. Pathways limiting warming to 2°C (>67%) are associated with 890 [640–1160] GtCO2 (Table SPM.2). (high confidence) {3.3, Box 3.4}

C.2.2Modelled global pathways that limit warming to 1.5°C (>50%) with no or limited overshoot involve more rapid and deeper near-term GHG emissions reductions through to 2030, and are projected to have less net negative CO2 emissions and less carbon dioxide removal (CDR) in the longer term, than pathways that return warming to 1.5°C (>50%) after a high overshoot (C2 category). Modelled pathways that limit warming to 2°C (>67%) have on average lower net negative CO2 emissions compared to pathways that limit warming to 1.5°C (>50%) with no or limited overshoot and pathways that return warming to 1.5°C (>50%) after a high overshoot (C1 and C2 categories respectively). Modelled pathways that return warming to 1.5°C (>50%) after a high overshoot (C2 category) show near-term GHG emissions reductions similar to pathways that limit warming to 2°C (>67%) (C3 category). For a given peak global warming level, greater and more rapid near-term GHG emissions reductions are associated with later net zero CO2 dates. (high confidence) (Table SPM.2) {3.3, Table 3.5, Cross-Chapter Box 3 in Chapter 3, Annex I: Glossary}

C.2.3Future non-CO2 warming depends on reductions in non-CO2GHGs, aerosols and their precursors, and ozone precursor emissions. In modelled global low-emission pathways, the projected reduction of cooling and warming aerosol emissions over time leads to net warming in the near- to mid-term. In these mitigation pathways, the projected reductions of cooling aerosols are mostly due to reduced fossil fuel combustion that was not equipped with effective air pollution controls. Non-CO2GHG emissions at the time of net zero CO2 are projected to be of similar magnitude in modelled pathways that limit warming to 2°C (>67%) or lower. These non-CO2GHG emissions are about 8 [5–11] GtCO2-eq yr –1, with the largest fraction from CH4 (60% [55–80%]), followed by N2O (30% [20–35%]) and F-gases (3% [2–20%]). 51 Due to the short lifetime of CH4 in the atmosphere, projected deep reduction of CH4 emissions up until the time of net zero CO2 in modelled mitigation pathways effectively reduces peak global warming. (high confidence) {3.3; AR6 WGI SPM D1.7}

C.2.4At the time of global net zero GHG emissions, net negative CO2 emissions counterbalance metric-weighted non-CO2GHG emissions. Typical emissions pathways that reach and sustain global net zero GHG emissions based on the 100-year global warming potential (GWP-100)7 are projected to result in a gradual decline of global warming. About half of the assessed pathways that limit warming to 1.5°C (>50%) with no or limited overshoot (C1 category) reach net zero GHG emissions during the second half of the 21st century. These pathways show greater reduction in global warming after the peak to 1.2 [1.1–1.4] °C by 2100 than modelled pathways in the same category that do not reach net zero GHG emissions before 2100 and that result in warming of 1.4 [1.3–1.5] °C by 2100. In modelled pathways that limit warming to 2°C (>67%) (C3 category), there is no significant difference in warming by 2100 between those pathways that reach net zero GHGs (around 30%) and those that do not (high confidence). In pathways that limit warming to 2°C (>67%) or lower and that do reach net zero GHG, net zero GHG occurs around 10–40 years later than net zero CO2 emissions (medium confidence). {Cross-Chapter Box 2 in Chapter 2, 3.3, Cross-Chapter Box 3 in Chapter 3; AR6 WGI SPM D1.8}

C.3 All global modelled pathways that limit warming to 1.5°C (>50%) with no or limited overshoot, and those that limit warming to 2°C (>67%), involve rapid and deep and in most cases immediate GHG emission reductions in all sectors. Modelled mitigation strategies to achieve these reductions include transitioning from fossil fuels without CCS to very low- or zero-carbon energy sources, such as renewables or fossil fuels with CCS, demand side measures and improving efficiency, reducing non-CO2 emissions, and deploying carbon dioxide removal (CDR) methods to counterbalance residual GHG emissions. Illustrative Mitigation Pathways (IMPs) show different combinations of sectoral mitigation strategies consistent with a given warming level. (high confidence)Expand Figure SPM.5Links to chapters3.2, 3.3, 3.4, 6.4, 6.6

C.3.1There is a variation in the contributions of different sectors in modelled mitigation pathways, as illustrated by the Illustrative Mitigation Pathways (IMPs). However, modelled pathways that limit warming to 2°C (>67%) or lower share common characteristics, including rapid and deep GHG emission reductions. Doing less in one sector needs to be compensated by further reductions in other sectors if warming is to be limited. (high confidence) (Figure SPM.5) {3.2, 3.3, 3.4}

C.3.2In modelled pathways that limit warming to 1.5°C (>50%) with no or limited overshoot, the global use of coal, oil and gas in 2050 is projected to decline with median values of about 95%, 60% and 45% respectively, compared to 2019. The interquartile ranges are (80 to 100%), (40 to 75%) and (20 to 60%) and the p5–p95 ranges are [60 to 100%], [25 to 90%] and [–30 to +85%], respectively. In modelled pathways that limit warming to 2°C (>67%), these projected declines have a median value and interquartile range of 85% (65 to 95%), 30% (15 to 50%) and 15% (–10 to +40%) respectively by 2050. The use of coal, oil and gas without CCS in modelled pathways that limit warming to 1.5°C (>50%) with no or limited overshoot is projected to be reduced to a greater degree, with median values of about 100%, 60% and 70% in 2050 compared to 2019. The interquartile ranges are (95 to 100%), (45 to 75%) and (60 to 80%) and the p5–p95 ranges about [85 to 100%], [25 to 90%] and [35 to 90%] for coal, oil and gas respectively. In these global modelled pathways, in 2050 almost all electricity is supplied from zero- or low-carbon sources, such as renewables or fossil fuels with CCS, combined with increased electrification of energy demand. As indicated by the ranges, choices in one sector can be compensated for by choices in another while being consistent with assessed warming levels. 52 (high confidence) {3.4, 3.5, Table 3.6, Figure 3.22, Figure 6.35}

C.3.3In modelled pathways that reach global net zero CO2 emissions: at the point they reach net zero, 5–16 GtCO2 of emissions from some sectors are compensated for by net negative CO2 emissions in other sectors. In most global modelled pathways that limit warming to 2°C (>67%) or lower, the AFOLU sector, via reforestation and reduced deforestation, and the energy supply sector reach net zero CO2 emissions earlier than the buildings, industry and transport sectors. (high confidence) (Figure SPM.5e,f) {3.4}

C.3.4In modelled pathways that reach global net zero GHG emissions, at the point they reach net zero GHG, around 74% [54 to 90%] of global emissions reductions are achieved by CO2 reductions in energy supply and demand, 13% [4 to 20%] by CO2 mitigation options in the AFOLU sector, and 13% [10 to 18%] through the reduction of non-CO2 emissions from land-use, energy and industry (medium confidence). (Figure SPM.5f) {3.3, 3.4}

C.3.5Methods and levels of CDR deployment in global modelled mitigation pathways vary depending on assumptions about costs, availability and constraints. 53 In modelled pathways that report CDR and that limit warming to 1.5°C (>50%) with no or limited overshoot, global cumulative CDR during 2020–2100 from bioenergy with carbon dioxide capture and storage (BECCS) and direct air carbon dioxide capture and storage (DACCS) is 30–780 GtCO2 and 0–310 GtCO2, respectively. In these modelled pathways, the AFOLU sector contributes 20–400 GtCO2 net negative emissions. Total cumulative net negative CO2 emissions including CDR deployment across all options represented in these modelled pathways are 20–660 GtCO2. In modelled pathways that limit warming to 2°C (>67%), global cumulative CDR during 2020–2100 from BECCS and DACCS is 170–650 GtCO2 and 0–250 GtCO2 respectively, the AFOLU sector contributes 10–250 GtCO2 net negative emissions, and total cumulative net negative CO2 emissions are around 40 [0–290] GtCO2. (Table SPM.2) (high confidence) {Table 3.2, 3.3, 3.4}

C.3.6All mitigation strategies face implementation challenges, including technology risks, scaling, and costs. Many challenges, such as dependence on CDR, pressure on land and biodiversity (e.g., bioenergy) and reliance on technologies with high upfront investments (e.g., nuclear), are significantly reduced in modelled pathways that assume using resources more efficiently (e.g., IMP-LD) or that shift global development towards sustainability (e.g., IMP-SP). (high confidence) (Figure SPM.5) {3.2, 3.4, 3.7, 3.8, 4.3, 5.1}

Figure SPM.5: Illustrative Mitigation Pathways (IMPs) and net zero CO2and GHG emissions strategies. Panels a and b show the development of global GHG and CO2 emissions in modelled global pathways (upper sub-panels) and the associated timing of when GHG and CO2 emissions reach net zero (lower sub-panels). Panels c and d show the development of global CH4 and N2O emissions, respectively. Coloured ranges denote the 5th to 95th percentile across pathways. The red ranges depict emissions pathways assuming policies that were implemented by the end of 2020 and pathways assuming implementation of NDCs (announced prior to COP26). Ranges of modelled pathways that limit warming to 1.5°C (>50%) with no or limited overshoot are shown in light blue (category C1) and pathways that limit warming to 2°C (>67%) are shown in light purple (category C3). The grey range comprises all assessed pathways (C1–C8) from the 5th percentile of the lowest warming category (C1) to the 95th percentile of the highest warming category (C8). The modelled pathway ranges are compared to the emissions from two pathways illustrative of high emissions (CurPol and ModAct) and five IMPs: IMP-LD, IMP-Ren, IMP-SP, IMP-Neg and IMP-GS. Emissions are harmonised to the same 2015 base year. The vertical error bars in 2015 show the 5–95th percentile uncertainty range of the non-harmonised emissions across the pathways, and the uncertainty range, and median value, in emission estimates for 2015 and 2019. The vertical error bars in 2030 (panel a) depict the assessed range of the NDCs, as announced prior to COP26 (Figure SPM.4). 23Panel e shows the sectoral contributions of CO2 and non-CO2 emissions sources and sinks at the time when net zero CO2 emissions are reached in the IMPs. Positive and negative emissions for different IMPs are compared to the GHG emissions from the year 2019. Energy supply (neg.) includes BECCS and DACCS. DACCS features in only two of the five IMPs (IMP-REN and IMP-GS) and contributes <1% and 64%, respectively, to the net negative emissions in Energy Supply (neg.). Panel f shows the contribution of different sectors and sources to the emissions reductions from a 2019 baseline for reaching net zero GHG emissions. Bars denote the median emissions reductions for all pathways that reach net zero GHG emissions. The whiskers indicate the p5–p95 range. The contributions of the service sectors (transport, buildings, industry) are split into direct (demand-side) as well as indirect (supply-side) CO2 emissions reductions. Direct emissions represent demand-side emissions due to the fuel use in the respective demand sector. Indirect emissions represent upstream emissions due to industrial processes and energy conversion, transmission and distribution. In addition, the contributions from the LULUCF sector and reductions from non-CO2 emissions sources (green and grey bars) are displayed. {3.3, 3.4}