Chapter 11: Industry

This chapter should be cited as:

Bashmakov, I.A., L.J. Nilsson, A. Acquaye, C. Bataille, J.M. Cullen, S. de la Rue du Can, M. Fischedick, Y. Geng, K. Tanaka, 2022: Industry. In IPCC, 2022: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change[P.R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, J. Malley, (eds.)]. Cambridge University Press, Cambridge, UK and New York, NY, USA. doi: 10.1017/9781009157926.013

Executive Summary

The Paris Agreement, the Sustainable Development Goals (SDGs) and the COVID-19 pandemic provide a new context for the evolution of industry and the mitigation of industry greenhouse gas (GHG) emissions (high confidence). This chapter is focused on what is new since AR5. It emphasises the energy and emissions intensive basic materials industries and key strategies for reaching net zero emissions. {11.1.1}

Net zero CO2 emissions from the industrial sector are possible but challenging (high confidence) . Energy efficiency will continue to be important. Reduced materials demand, material efficiency, and circular economy solutions can reduce the need for primary production. Primary production options include switching to new processes that use low to zero GHG energy carriers and feedstocks (e.g., electricity, hydrogen, biofuels, and carbon capture and utilisation (CCU) for carbon feedstock), and carbon capture and storage (CCS) for remaining CO2. These options require substantial scaling up of electricity, hydrogen, recycling, CO2, and other infrastructure, as well as phase-out or conversion of existing industrial plants. While improvements in the GHG intensities of major basic materials have nearly stagnated over the last 30 years, analysis of historical technology shifts and newly available technologies indicate these intensities can be reduced to net zero emissions by mid-century. {11.2, 11.3, 11.4}

Whatever metric is used, industrial emissions have been growing faster since 2000 than emissions in any other sector, driven by increased basic materials extraction and production (high confidence). GHG emissions attributed to the industrial sector originate from fuel combustion, process emissions, product use and waste, which jointly accounted for 14.1 GtCO2-eq or 24% of all direct anthropogenic emissions in 2019, second behind the energy transformation sector. Industry is a leading GHG emitter – 20 GtCO2-eq or 34% of global emissions in 2019 – if indirect emissions from power and heat generation are included. The share of emissions originating from direct fuel combustion is decreasing and was 7 GtCO2-eq, 50% of direct industrial emissions in 2019. {11.2.2}

Global material intensity (in-use stock of manufactured capital, in tonnes per unit of GDP is increasing (high confidence). In-use stock of manufactured capital per capita has been growing faster than GDP per capita since 2000. Total global in-use stock of manufactured capital grew by 3.4% yr –1 in 2000–2019. At the same time, per capita material stocks in several developed countries have stopped growing, showing a decoupling from GDP per capita. {11.2.1, 11.3.1}

Plastic is the material for which demand has been growing the strongest since 1970 (high confidence). The current >99% reliance on fossil feedstock, very low recycling, and high emissions from petrochemical processes is a challenge for reaching net zero emissions. At the same time, plastics are important for reducing emissions elsewhere, for example, light-weighting vehicles. There are as yet no shared visions for fossil-free plastics, but several possibilities. {11.4.1.3}

Scenario analyses show that significant cuts in global GHG emissions and even close to net zero emissions from GHG intensive industry (e.g., steel, plastics, ammonia, and cement) can be achieved by 2050 by deploying multiple available and emerging options (medium confidence). Cutting industry emissions significantly requires a reorientation from the historic focus on important but incremental improvements (e.g., energy efficiency) to transformational changes in energy and feedstock sourcing, materials efficiency, and more circular material flows. {11.3, 11.4}

Key climate mitigation options such as materials efficiency, circular material flows and emerging primary processes, are not well represented in climate change scenario modelling and integrated assessment models, albeit with some progress in recent years (high confidence). The character of these interventions (e.g., appearing in many forms across complex value chains, making cost estimates difficult) combined with the limited data on new fossil-free primary processes help explain why they are less represented in models than, for example, CCS. As a result, overall mitigation costs and the need for CCS may be overestimated. {11.4.2.1}

Electrification is emerging as a key mitigation option for industry (high confidence). Electricity is a versatile energy carrier, potentially produced from abundant renewable energy sources or other low carbon options; regional resources and preferences will vary. Using electricity directly, or indirectly via hydrogen from electrolysis for high temperature and chemical feedstock requirements, offers many options to reduce emissions. It also can provide substantial grid balancing services, for example through electrolysis and storage of hydrogen for chemical process use or demand response. {11.3.5}

Carbon is a key building block in organic chemicals, fuels and materials, and will remain important (high confidence). In order to reach net zero CO2 emissions for the carbon needed in society (e.g., plastics, wood, aviation fuels, solvents, etc.), it is important to close the use loops for carbon and carbon dioxide through increased circularity with mechanical and chemical recycling, more efficient use of biomass feedstock with the addition of low GHG hydrogen to increase product yields (e.g., for biomethane and methanol), and potentially direct air capture of CO2 as a new carbon source. {11.3, 11.4.1}

Production costs for very low to zero emissions basic materials may be high but the cost for final consumers and the general economy will be low (medium confidence). Costs and emissions reductions potential in industry, and especially heavy industry, are highly contingent on innovation, commercialisation, and market uptake policy. Technologies exist to take all industry sectors to very low or zero emissions but require 5 to 15 years of intensive innovation, commercialisation, and policy to ensure uptake. Mitigation costs are in the rough range of USD50–150 tCO2-eq –1, with wide variation within and outside this band. This affects competitiveness and requires supporting policy. Although production cost increases can be significant, they translate to very small increases in the costs for final products, typically less than a few percent depending on product, assumptions, and system boundaries. {11.4.1.5}

There are several technological options for very low to zero emissions steel, but their uptake will require integrated material efficiency, recycling, and production decarbonisation policies (high confidence). Material efficiency can potentially reduce steel demand by up to 40% based on design for less steel use, long life, reuse, constructability, and low contamination recycling. Secondary production through high quality recycling must be maximised. Production decarbonisation will also be required, starting with the retrofitting of existing facilities for partial fuel switching (e.g., to biomass or hydrogen), CCU and CCS, followed by very low and zero emissions production based on high-capture CCS or direct hydrogen, or electrolytic iron ore reduction followed by an electric arc furnace. {11.3.2, 11.4.1.1}

There are several current and near-horizon options to greatly reduce cement and concrete emissions. Producer, user, and regulator education, as well as innovation and commercialisation policy are needed (medium confidence). Cement and concrete are currently overused because they are inexpensive, durable, and ubiquitous, and consumption decisions typically do not give weight to their production emissions. Basic material efficiency efforts to use only well-made concrete thoughtfully and only where needed (e.g., using right-sized, prefabricated components) could reduce emissions by 24–50% through lower demand for clinker. Cementitious material substitution with various materials (e.g., ground limestone and calcined clays) can reduce process calcination emissions by up to 50% and occasionally much more. Until a very low GHG emissions alternative binder to Portland cement is commercialised, which does not look promising in the near to medium term, CCS will be essential for eliminating the limestone calcination process emissions for making clinker, which currently represent 60% of GHG emissions in best available technology plants. {11.3.2, 11.3.6, 11.4.1.2}

While several technological options exist for decarbonising the main industrial feedstock chemicals and their derivatives, the costs vary widely (high confidence) . Fossil fuel-based feedstocks are inexpensive and still without carbon pricing, and their biomass- and electricity-based replacements will likely be more expensive. The chemical industry consumes large amounts of hydrogen, ammonia, methanol, carbon monoxide, ethylene, propylene, benzene, toluene, and mixed xylenes and aromatics from fossil feedstock, and from these basic chemicals produces tens of thousands of derivative end-use chemicals. Hydrogen, biogenic or air-capture carbon, and collected plastic waste for the primary feedstocks can greatly reduce total emissions. Biogenic carbon feedstock is likely to be limited due to competing land uses. {11.4.1.3}

Light industry and manufacturing can be largely decarbonised through switching to low GHG fuels (e.g., biofuels and hydrogen) and electricity (e.g., for electrothermal heating and heat pumps) (high confidence) . Most of these technologies are already mature, for example, for low temperature heat, but a major challenge is the current low cost of fossil methane and coal relative to low and zero GHG electricity, hydrogen, and biofuels. {11.4.1.4}

The pulp and paper industry has significant biogenic carbon emissions but relatively small fossil carbon emissions. Pulp mills have access to biomass residues and by-products and in paper mills the use of process heat at low to medium temperatures allows for electrification (high confidence). Competition for feedstock will increase if wood substitutes for building materials and petrochemicals feedstock. The pulp and paper industry can also be a source of biogenic carbon dioxide and carbon for organic chemicals feedstock and carbon dioxide removal (CDR) using CCS. {11.4.1.4}

The geographical distribution of renewable resources has implications for industry (medium confidence). The potential for zero emission electricity and low-cost hydrogen from electrolysis powered by solar and wind, or hydrogen from other very low emission sources, may reshape where currently energy and emissions intensive basic materials production is located, how value chains are organised, trade patterns, and what gets transported in international shipping. Regions with bountiful solar and wind resources, or low fugitive methane co-located with CCS geology, may become exporters of hydrogen or hydrogen carriers such as methanol and ammonia, or home to the production of iron and steel, organic platform chemicals, and other energy-intensive basic materials. {11.2, 11.4 and Box 11.1}

The level of policy maturity and experience varies widely across the mitigation options (high confidence). Energy efficiency is a well-established policy field with decades of experience from voluntary and negotiated agreements, regulations, energy auditing and demand side-management (DSM) programmes (see AR5). In contrast, materials demand management and efficiency are not well understood and addressed from a policy perspective. Barriers to recycling that policy could address are often specific to the different material loops (e.g., copper contamination for steel and lack of technologies or poor economics for plastics) or waste management systems. For electrification and fuel switching the focus has so far been mainly on innovation and developing technical supply-side solutions rather than creating market demand. {11.5.2, 11.6}

Industry has so far largely been sheltered from the impacts of climate policy and carbon pricing due to concerns for competitiveness and carbon leakage (high confidence). New industrial development policy approaches needed for realising a transition to net zero GHG emissions are emerging. The transition requires a clear direction towards net zero, technology development, market demand for low-carbon materials and products, governance capacity and learning, socially inclusive phase-out plans, as well as international coordination of climate and trade policies. It requires comprehensive and sequential industrial policy strategies leading to immediate action as well as preparedness for future decarbonisation, governance at different levels (from international to local), and integration with other policy domains. {11.6}

11.1Introduction and New Developments

11.1.1About This Chapter

The AR5 was published in 2014. The Paris Agreement and the 17 Sustainable Development Goals (SDGs) were adopted in 2015. An increasing number of countries have since announced ambitions to be carbon neutral by 2045–2060. The COVID-19 pandemic shocked the global economy in 2020 and motivated economic stimulus with demands for green recovery and concerns for economic security. All this has created a new context and a growing recognition that all industry, including the energy and emissions intensive industries, need to reach net zero GHG emissions. There is an ongoing mind shift around the opportunities to do so, with electrification and hydrogen emerging among key mitigation options as a result of renewable electricity costs falling rapidly. On the demand side there has been renewed attention to end-use demand, material efficiency, and more and better-quality recycling measures. This chapter takes its starting point in this new context and emphasises the need for deploying innovative processes and practices in order to limit the global warming to 1.5°C or 2°C (IPCC 2018a).

The industrial sector includes ores and minerals mining, manufacturing, construction and waste management. It is the largest source of global GHG and CO2 emissions, which include direct and indirect fuel-combustion-related emissions, emissions from industrial processes and products use, as well as from waste. This chapter is focused on heavy industry – the high temperature heat and process emissions intensive basic materials industries that account for 65% of industrial GHG and over 70% of industrial CO2 emissions (waste excluded), where deployment of near‐zero emissions technologies can be more challenging due to capital intensity and equipment lifetimes compared with other manufacturing industries. The transition of heavy industries to zero emissions requires supplementing the traditional toolkit of energy and process efficiency, fuel switching, electrification, and decarbonisation of power with material end-use demand management and efficiency, circular economy, fossil-free feedstocks, carbon capture and utilisation (CCU), and carbon capture and storage (CCS). Energy efficiency was extensively treated in AR5 and remains a key mitigation option. This chapter is focused mainly on new options and developments since AR5, highlighting measures along the whole value chains that are required to approach zero emissions in primary materials production.

11.1.2Approach to Understanding Industrial Emissions

The Kaya identity offers a useful tool of decomposing emission sources and their drivers, as well as of weighing the mitigation options. The one presented below (Equation 11.1) builds on the previous assessments (IPCC 2014, 2018b; Hoegh-Guldberg et al. 2018), and reflect a material stock-driven services-oriented vision to better highlight the growing importance of industrial processes (dominated in emissions increments in 2010–2019), product use and waste in driving emissions. Services delivery (nutrition, shelter, mobility, education, etc.; see Chapter 5 for more detail) not only requires energy and material flows (fuels, food, feed, fertilisers, packaging, etc.), but also material stocks (buildings, roads, vehicles, machinery, etc.), the mass of which has already exceeded 1000 Gt (Krausmann et al. 2018). As material efficiency appears to be an important mitigation option, material intensity or productivity (material extraction or consumption versus GDP (Oberle et al. 2019; Hertwich et al. 2020)) is reflected in the identity with two dimensions: as material stock intensity of GDP (tonnes per dollar) and material intensity of building and operating accumulated in-use stock. 1 For sub-global analysis the ratio of domestically used materials to total material production becomes important to reflect outsourced materials production and distinguish between territorial and consumption-based emissions. The identity for industry differs significantly from that for sectors with where combustion emissions dominate (Lamb et al. 2021).

Recent progress in data availability that allows the integration of major emission sources along with socio-economic metabolism, material flows and stock analysis enriches the identity for industry from a perspective of possible policy interventions (Bashmakov 2021):

Equation 11.1 Table 1 | Variables, Factors, Policies and Drivers

Variables | Factors | Policies and drivers | |

POP | Population | Demographic policies | Demand decarbonisation |

GDP/POP | Services (expressed via GDP– final consumption and investments needed to maintain and expand stock) per capita | Sufficiency and demand management (reduction) | |

MStock/GDP | Material stock (MStock – accumulated in-use stocks of materials embodied in manufactured fixed capital) intensity of GDP | Material stock efficiency improvement | |

(MPR+MSE)/MStock | Material inputs (both virgin (primary materials extraction, MPR) and recycled (secondary materials use, MSE)) per unit of in-use material stock | Material efficiency, substitution and circular economy | |

Dm | Share of allocated emissions – consumption vs production emissions accounting (valid only for sub-global levels)* | Trade policies including carbon leakage issues (localisation versus globalisation) | CBAM |

E/(MPR+MSE) | Sum of energy use for basic material production (Em), processing and other operational industrial energy use (Eoind) per unit of material inputs | Energy efficiency of basic materials production and other industrial processes | Production decarbonisation |

(GHGed+GHGeind)/E | Direct (GHGed) and indirect (GHGeind) combustion-related industrial emissions per unit of energy | Electrification, fuel switching, and energy decarbonisation (hydrogen, CCUS-fuels) | |

GHGoth/(MPR+MSE) | Emissions from industrial processes and product use, waste, F-gases, indirect nitrogen emissions per unit of produced materials | Feedstock decarbonisation (hydrogen), CCUS-industrial processes, waste and F-gases management |

*Dm=1, when territorial emission is considered, and Dm equals the ratio of domestically used materials to total material production for the consumption-based emission accounting). CBAM – carbon border adjustment mechanism.

Factors in Equation 11.1 are interconnected by either positive or negative feedbacks: scrap-based production or light-weighing improves operational energy efficiency, while growing application of carbon capture, use and storage (CCUS) brings it down and increases material demands (Hertwich et al. 2019; IEA 2020a, 2021a). There are different ways to disaggregate Equation 11.1: by industrial subsectors (Bashmakov 2021); by reservoirs of material stock (buildings, infrastructure, vehicles, machinery and appliances, packaging, etc.); by regions and countries (where carbon leakage becomes relevant); by products and production chains (material extraction, production of basic materials, basic materials processing, production of final industrial products); by traditional and low carbon technologies used; and by stages of products’ lives including recycling.

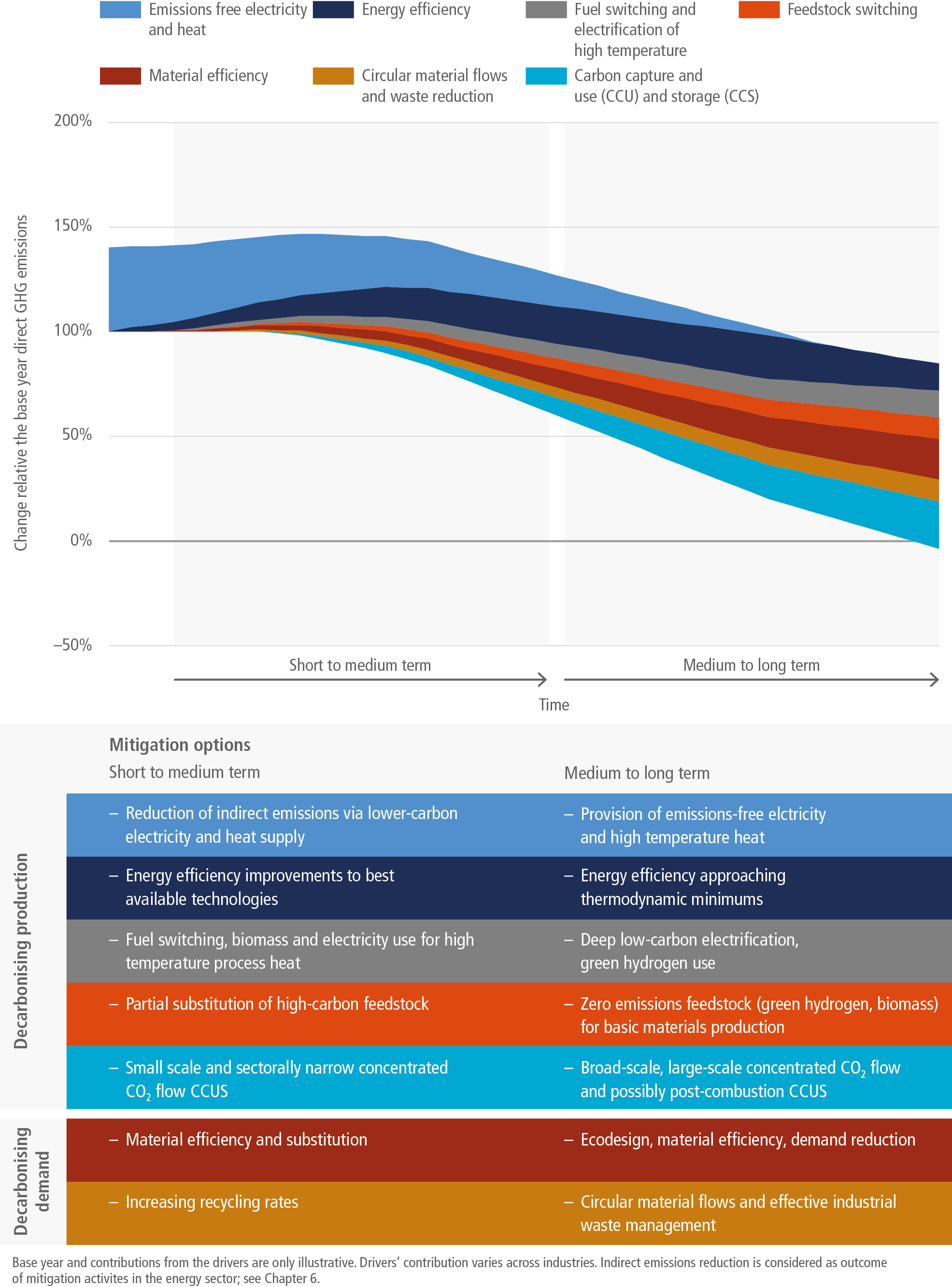

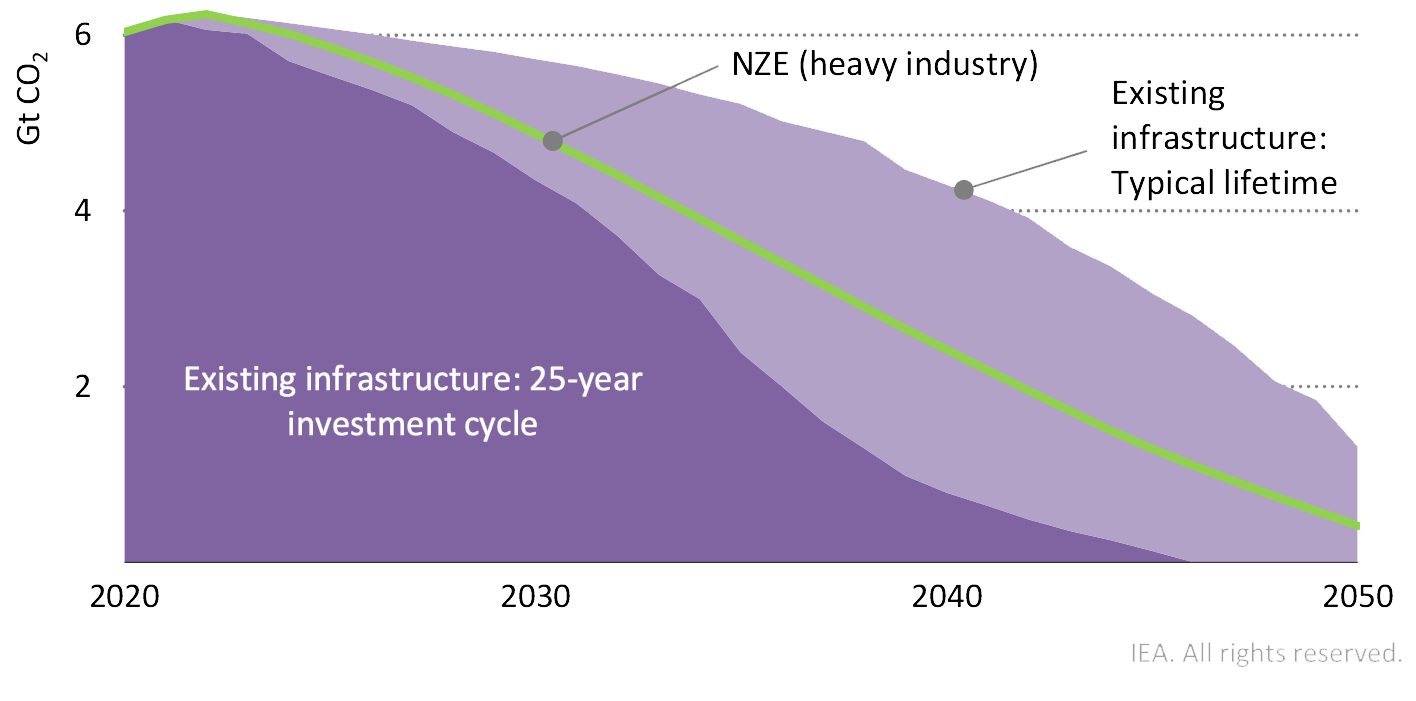

An industrial transition to net zero emissions is possible when the three last multipliers in Equation 11.1 (in square parentheses) are approaching zero. Contributions from different drivers (energy efficiency, low carbon electricity and heat, material efficiency, switching to low carbon feedstock and CCUS) to this evolution vary with time. Energy efficiency dominates in the short- and medium term and potentially long term (in the range of 10–40% by 2050) (IPCC 2018a; Crijns-Graus et al. 2020; IEA 2020a), but for deep decarbonisation trajectories, contributions from the other drivers steadily grow, as the share of non-energy sources in industrial emissions rises and new technologies to address mitigation from these sources mature (Material Economics 2019; CEMBUREAU 2020; BP 2020; Hertwich et al. 2020, 2019; IEA 2021a, 2020a; Saygin and Gielen 2021) (Figure 11.1).

Figure 11.1 | Stylised composition and contributions from different drivers to the transition of industry to net zero emissions.

11.2New Trends in Emissions and Industrial Development

11.2.1Major Drivers

The use of materials is deeply coupled with economic development and growth. For centuries, humanity has been producing and using hundreds of materials (Ashby 2012), the diversity of which skyrocketed in the recent half-century to achieve the desired performance and functionality of multiple products (density; hardness; compressive strength; melting point, resistance to mechanical and thermal shocks and to corrosion; transparency; heat- or electricity conductivity; chemical neutrality or activity, to name a few). New functions drive the growth of material complexity of products; for example, a modern computer chip embodies over 60 different elements (Graedel et al. 2015).

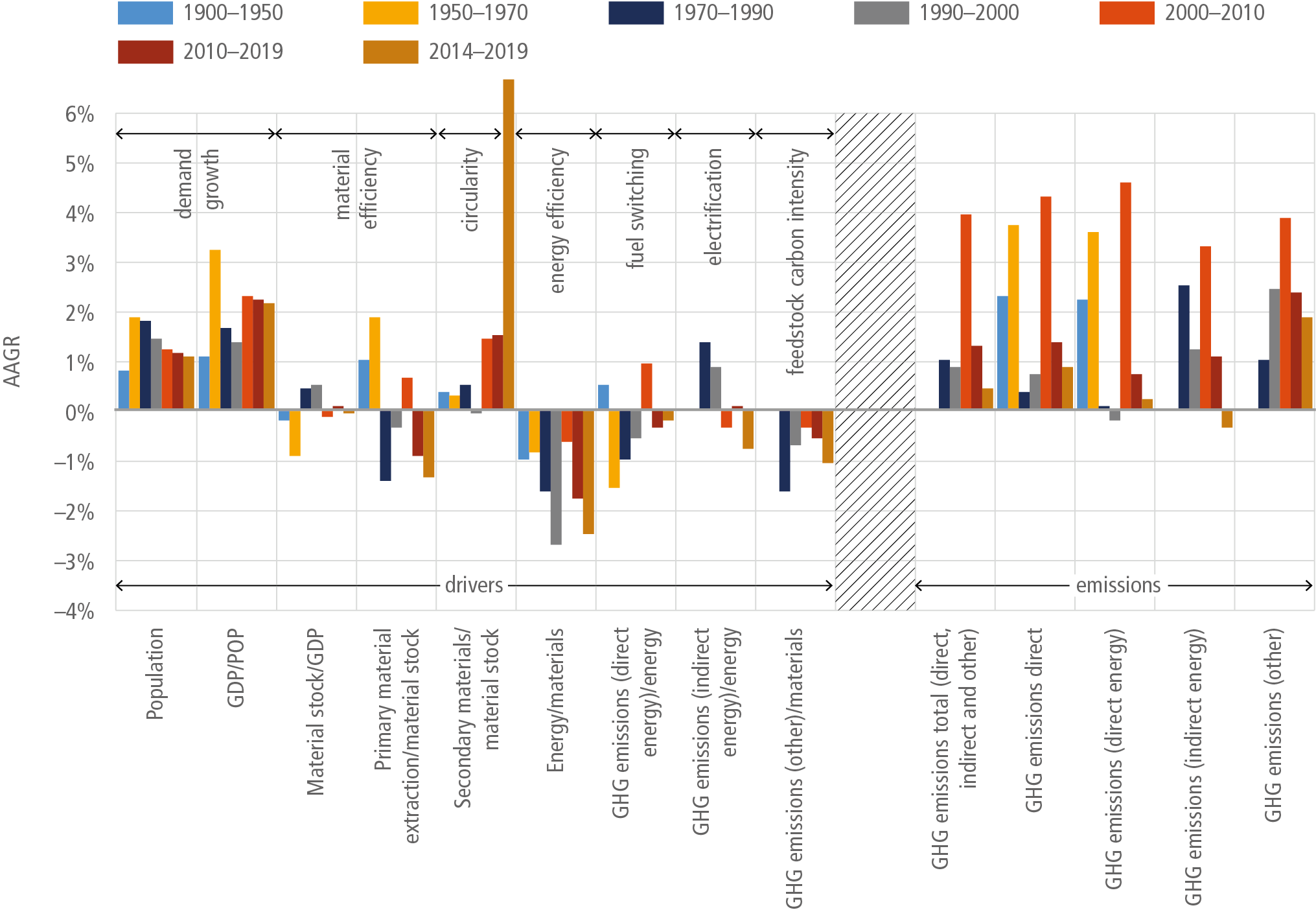

Key factors driving up industrial GHG emissions since 1900 include population and per capita GDP, 2 while energy efficiency and non-combustion GHG emissions intensity (from industrial processes and waste) has been pushing it down. Material efficiency factors – material stock intensity of GDP and ratio of extraction, processing and recycling of materials per unit of built capital along with combustion-related emissions intensity factors and electrification – were cyclically switching their contributions with relatively limited overall impact. Growing recycling allowed for replacement of some energy-intensive virgin materials and thus contributed to mitigation. In 2014–2019, a combination of these drivers allowed for a slowdown in the growth of industrial GHG emissions to below 1% (Figure 11.2 and Table 11.1), while to match a net zero emissions trajectory it should decline by 2% yr –1 in 2020–2030 and by 8.9% yr –1 in 2030–2050 (IEA 2021a).

Table 11.1 | Dynamics and structure of industrial greenhouse gas (GHG) emissions.

Average annual growth rates | Share in total industrial sector emissions | 2019 emissions MtCO2-eq | |||||||||

1971–1990 | 1991–2000 | 2000–2010 | 2011–2019 | 1970 | 1990 | 2000 | 2010 | 2019 | |||

Direct CO2 emissions from fuel combustion | Mining (excl. fuels), manufacturing industries and construction | 0.13% | –0.18% | 4.62% | 0.77% | 45.8% | 37.3% | 33.2% | 36.6% | 34.9% | 6981 |

Iron and steel | 0.20% | 0.13% | 5.62% | 2.28% | 12.4% | 10.2% | 9.4% | 11.4% | 12.4% | 2481 | |

Chemical and petrochemical | 3.66% | 1.54% | 3.16% | 1.19% | 3.0% | 4.9% | 5.2% | 4.9% | 4.9% | 977 | |

Non-ferrous metals | 2.12% | 3.20% | 1.12% | 1.36% | 0.7% | 0.8% | 1.0% | 0.8% | 0.8% | 163 | |

Non-metallic minerals | 2.91% | 1.88% | 6.24% | –0.04% | 3.3% | 4.6% | 5.0% | 6.5% | 5.7% | 1148 | |

Paper, pulp and printing | 0.78% | 2.79% | 0.09% | –2.69% | 1.4% | 1.3% | 1.5% | 1.1% | 0.7% | 150 | |

Food and tobacco | 2.55% | 1.50% | 3.03% | –1.04% | 1.3% | 1.6% | 1.7% | 1.6% | 1.3% | 265 | |

Other | –1.55% | –2.89% | 4.61% | –0.22% | 23.8% | 13.8% | 9.4% | 10.3% | 9.0% | 1797 | |

Indirect emissions – electricity | 2.87% | 2.06% | 3.00% | –0.87% | 17.6% | 24.6% | 27.3% | 25.8% | 21.2% | 4236 | |

Indirect emissions – heat | 2.08% | –3.09% | 2.53% | 9.83% | 5.6% | 6.7% | 4.5% | 4.0% | 8.3% | 1663 | |

Industrial processes CO2 | Total | 1.45% | 2.16% | 5.00% | 1.93% | 11.0% | 11.6% | 13.0% | 14.9% | 15.7% | 3144 |

Non-metallic minerals | 2.22% | 2.36% | 5.66% | 1.67% | 5.7% | 7.0% | 8.0% | 9.7% | 10.0% | 2008 | |

Chemical and petrochemical | 4.51% | 2.52% | 3.50% | 2.01% | 1.5% | 2.9% | 3.4% | 3.4% | 3.6% | 720 | |

Metallurgy | –3.11% | 0.37% | 5.16% | 3.10% | 3.6% | 1.5% | 1.4% | 1.7% | 2.0% | 391 | |

Other | 1.55% | 2.30% | –1.21% | 2.89% | 0.1% | 0.2% | 0.2% | 0.1% | 0.1% | 25 | |

Industrial product use GHG | –0.22% | –0.49% | –1.02% | 0.41% | 2.7% | 2.0% | 1.7% | 1.1% | 1.0% | 204 | |

Other non-CO2GHG | –0.60% | 5.20% | 4.29% | 3.20% | 5.5% | 3.9% | 5.8% | 6.2% | 7.3% | 1470 | |

Waste GHG | 1.94% | 1.35% | 1.22% | 1.57% | 11.9% | 13.8% | 14.4% | 11.4% | 11.6% | 2327 | |

Total GHG | 1.16% | 0.98% | 3.61% | 1.32% | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | 20,025 | |

Source: calculated based on Crippa et al. (2021); IEA (2021b); and Minx et al. (2021).

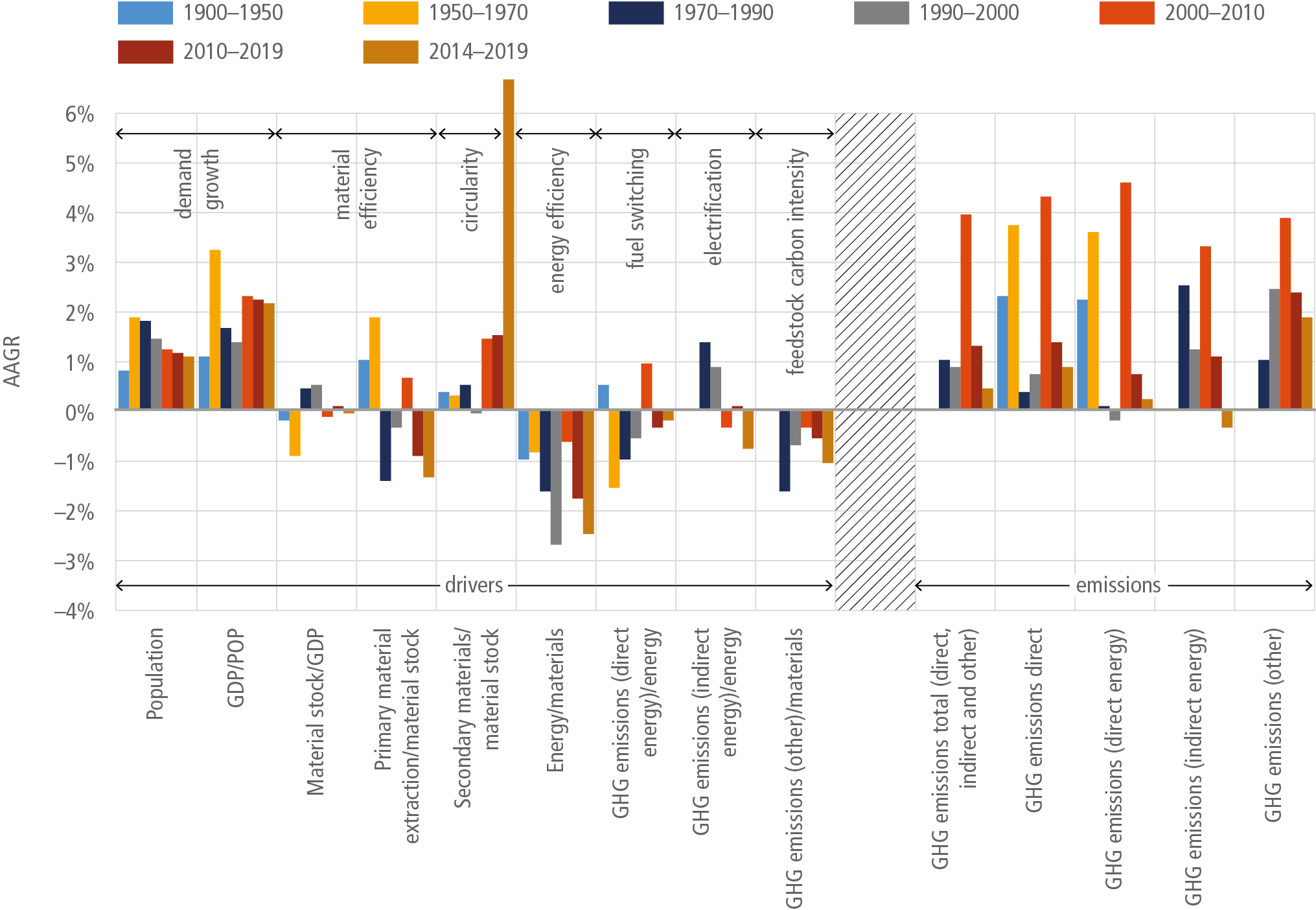

Figure 11.2 | Average annual growth rates of industrial sector GHG emissions and drivers (1900–2019). Before 1970, GHG emission (other) is limited to that from cement production. Waste emission is excluded. Primary material extraction excludes fuels and biomass. Presented factors correspond directly to Equation 11.1. Sources: population before 1950 and GDP before 1960: Maddison Project (2018); population from 1950 to 1970: UN (2015); population and GDP for 1960–2020: World Bank (2021); data on material stock, extraction, and use of secondary materials: Wiedenhofer et al. (2019); data on material extraction: UNEP and IRP (2020); industrial energy use for 1900–1970: IIASA (2018), for 1971–2019: IEA (2021b); data on industrial GHG emissions for 1900–1970: CDIAC (2017), for 1970–2019: data from Crippa et al. (2021) and Minx et al. (2021).

There are two major concepts of material efficiency (ME). The broader one highlights demand reduction via policies promoting more intensive use, assuming sufficient (excluding luxury) living space or car ownership providing appropriate service levels – housing days or miles driven and life-time extension (Hertwich et al. 2019, 2020). This approach focuses on dematerialisation of society (Lechtenböhmer and Fischedick 2020), where a ‘dematerialisation multiplier’ (Pauliuk et al. 2021) limits both material stock and GDP growth, as progressively fewer materials are required to build and operate the physical in-use stock to deliver sufficient services. According to the IRP (2020), reducing floor space demand by 20% via shared and smaller housing compared to the reference scenario would decrease Group of Seven (G7) countries’ GHG emissions from the material-cycle of residential construction up to 70% in 2050. The narrower concept ignores demand and sufficiency aspects and focuses on supply chains considering ME as less basic materials use to produce a certain final product, for example, a car or a metre squared of living space (OECD 2019a; IEA 2020a). No matter if the broader or the narrower concept of ME is applied, in 1970–2019 it did not contribute much to the decoupling of industrial emissions from GDP. This is expected to change in the future (Figure 11.2).

Material efficiency analysis mostly uses material intensity or productivity indicators, which compare material extraction or consumption with GDP (Oberle et al. 2019; Hertwich et al. 2020). Those indicators are functions of material stock intensity of GDP (tonnes per dollar) and material intensity of building and operating accumulated in-use stock. Coupling services or GDP with the built stock allows for a better evaluation of demand for primary basic materials (Müller et al. 2011; Liu et al. 2013; Liu and Müller 2013; Pauliuk et al. 2013a; Cao et al. 2017; Wiedenhofer et al. 2019; Hertwich et al. 2020; Krausmann et al. 2020). Since 1970 material stock growth driven by industrialisation and urbanisation slightly exceeded that of GDP and there was no decoupling, 3 so in Kaya-like identities material stock may effectively replace GDP. There are different methods to estimate the former (see reviews in Pauliuk et al. (2015, 2019) and Wiedenhofer et al. (2019), the results of which are presented for major basic materials with some geographical resolution (Liu and Müller 2013; Pauliuk et al. 2013a) or globally (Graedel et al. 2011; Geyer et al. 2017; Krausmann et al. 2018; Pauliuk et al. 2019; Wiedenhofer et al. 2019; International Aluminium Institute 2021a).

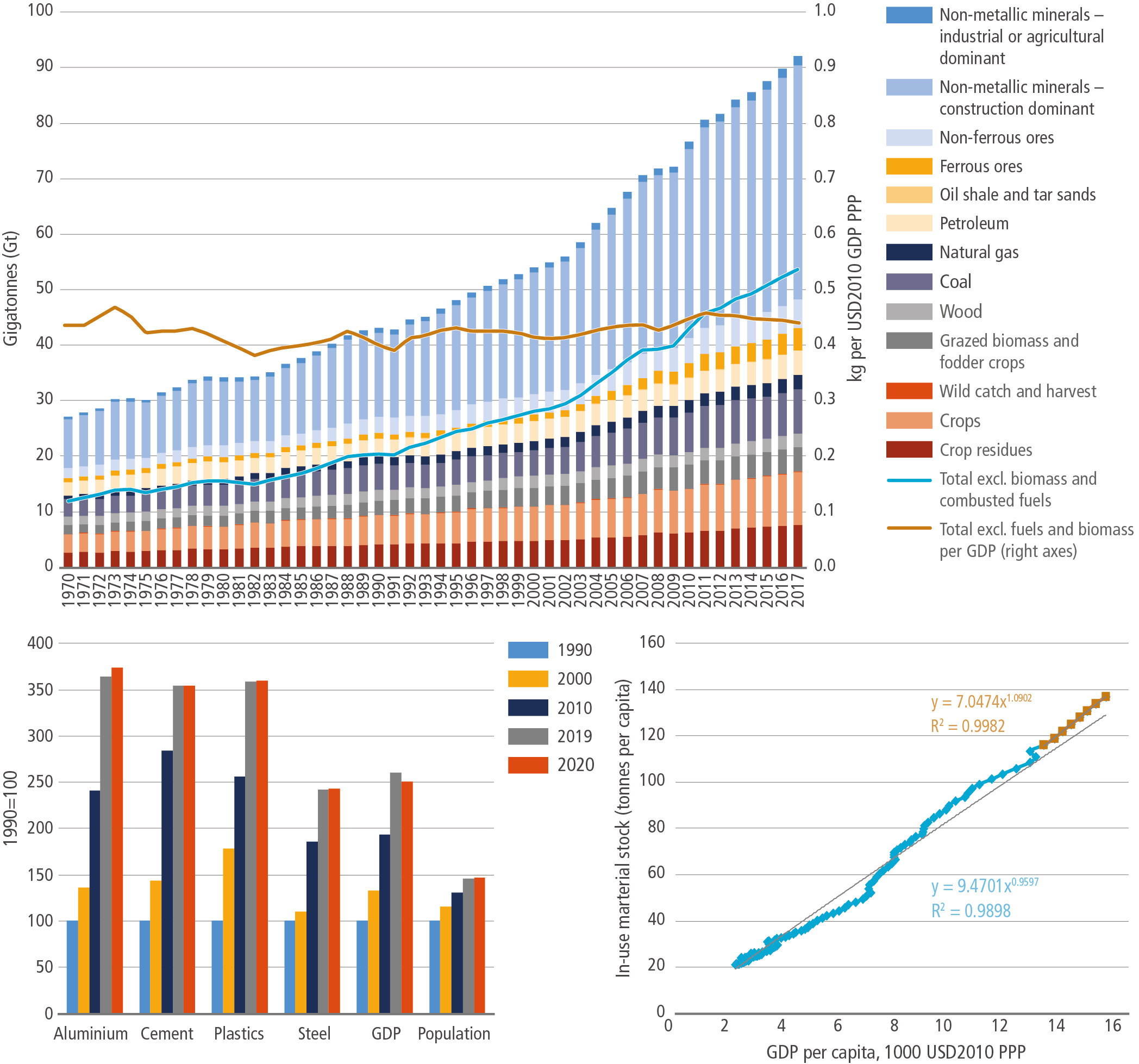

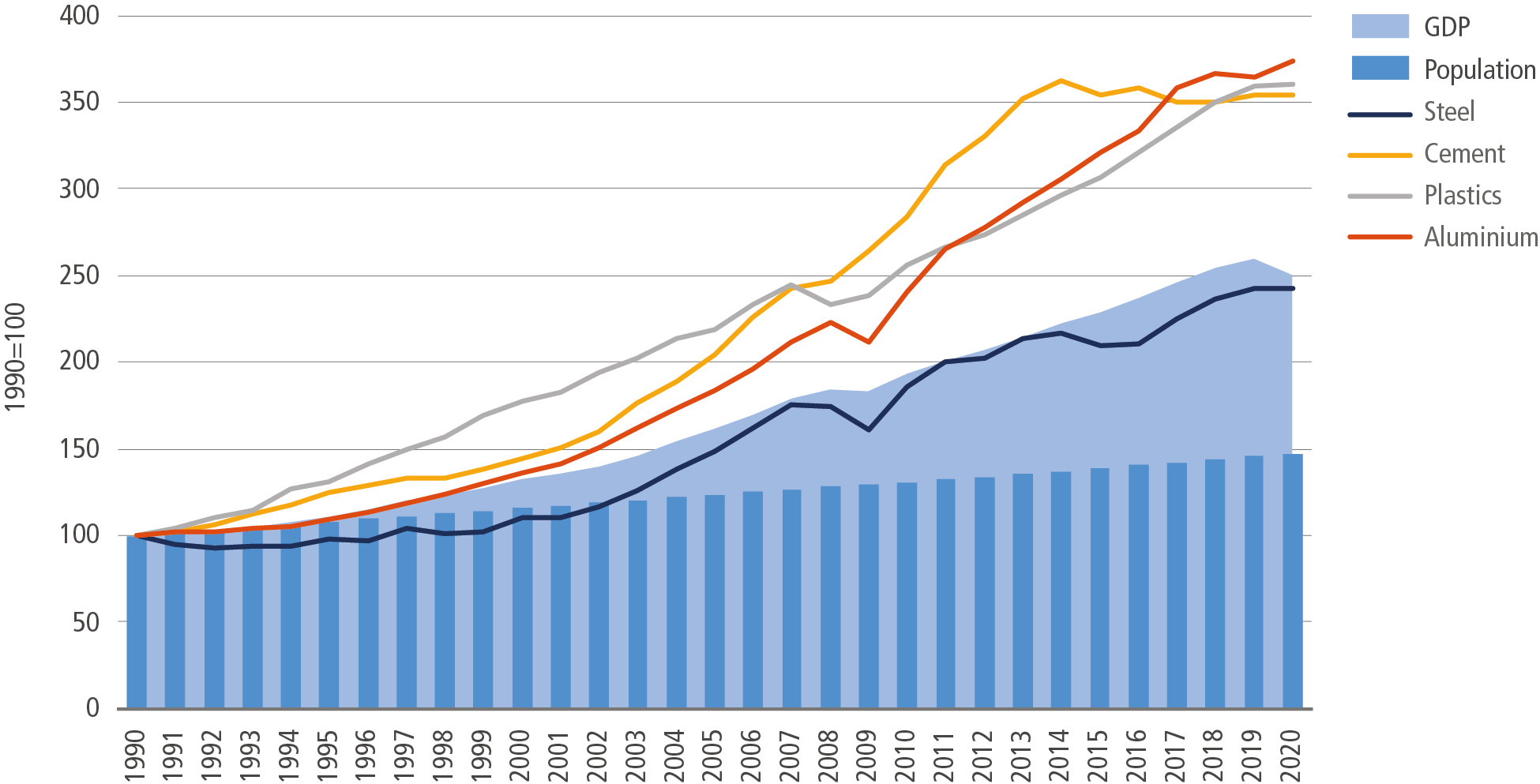

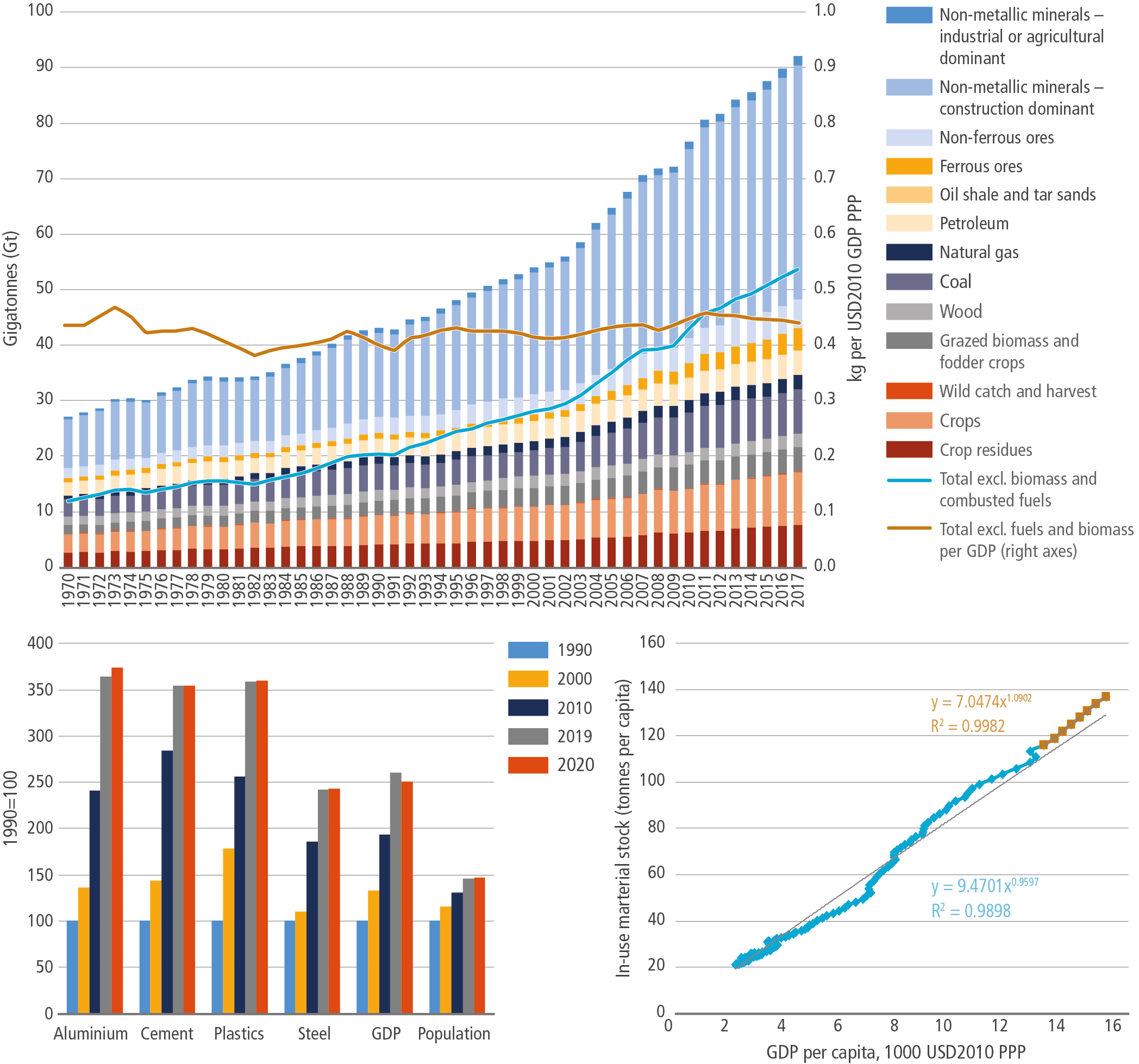

For a subset of materials, such as solid wood, paper, plastics, iron/steel, aluminium, copper, other metals/minerals, concrete, asphalt, bricks, aggregate, and glass, total in-use stock escalated from 36 Gt back in 1900 to 186 Gt in 1970, 572 Gt in 2000, and 960 Gt in 2015, and by 2020 it exceeded 1,100 Gt, or 145 tonnes per capita (Krausmann et al. 2018, 2020; Wiedenhofer et al. 2019). In 1900–2019, the stock grew 31-fold, which is strongly coupled with GDP growth (36-fold). As the UK experience shows, material stock intensity of GDP may ultimately decline after services fully dominate GDP, and this allows for material productivity improvements to achieve absolute reduction in material use, as stock expansion slows down (Streeck et al. 2020). While the composition of basic materials within the stock of manufactured capital was evolving significantly, overall stock use associated with a unit of GDP has been evolving over the last half-century in a quite narrow range of 7.7–8.6 t per USD1000 (2017 purchasing power parity (PPP)) showing neither signs of decoupling from GDP, nor saturation as of yet. Mineral building materials (concrete, asphalt, bricks, aggregate, and glass) dominate the stock volume by mass (94.6% of the whole stock, with the share of concrete alone standing at 43.5%), followed by metals (3.5%) and solid wood (1.4%). The largest part of in-use stock of our ‘cementing societies’ (Cao et al. 2017) is constituted by concrete: about 417 Gt in 2015; Krausmann et al. (2018) extrapolated this to 478 Gt (65 tonnes per capita) in 2018, which contains about 88 Gt of cement. 4 The iron and steel stock is assessed at 25–35 Gt (Wiedenhofer et al. 2019; Gielen et al. 2020; Wang et al. 2021), while the plastics stock reached 2.5–3.2 Gt (Geyer et al. 2017; Wiedenhofer et al. 2019; Saygin and Gielen 2021) and the aluminium stock approached 1.1 Gt (International Aluminium Institute 2021a), or just 0.1% of the total. In sharp contrast to global energy intensity, which has more than halved since 1900 (Bashmakov 2019), in 2019 material stock intensity (in-use stock of manufactured capital per GDP) was only 14% below the 1900 level, but 15% above the 1970 level. In-use stock per capita has been growing faster than GDP per capita since 2000 (Figure 11.3). The growth rate of total in-use stock of manufactured capital was 3.8% in 1971–2000 and 3.5% in 2000–2019, or 32–35 Gt yr –1, to which concrete and aggregates contributed 88%. Recent demand for stockbuilding materials was 51–54 Gt yr –1, to which recycled materials recently contributed only about 10% of material input. About 46–49 Gt yr –1 was virgin inputs, which after accounting for processing waste and short-lived products (over 8 Gt yr –1) scale up to 54–58 Gt yr –1 of primary extraction (Krausmann et al. 2017, 2018; UNEP and IRP 2020). The above indicates that we have only begun to exploit the potential for recycling and circularity more broadly.

Figure 11.3 | Raw natural materials extraction since 1970. In windows: left – growth of population, GDP and basic materials production (1990 = 100) in 1990–2020; right – in-use stock per capita vs income level (1900–2018; brown dots are for 2000–2018). The regressions provided show that for more recent years elasticity of material stock to GDP was greater than unity, comparing with the lower unity in preceding years. Source: developed based on Maddison Project (2018); Wiedenhofer et al. (2019); IEA (2020b); UNEP and IRP (2020); International Aluminium Institute (2021a); Statista (2021a,b); U.S. Geological Survey (2021); World Bank (2021); World Steel Association (2021).

Total extraction of all basic materials (including biomass and fuels) in 2017 reached 92 Gt yr –1, which is 13 times above the 1900 level (Figure 11.3). 5 When recycled resources are added, total material inputs exceed 100 Gt (Circle Economy 2020). In Equation 11.1MPR represents only material inputs to the stock, excluding dissipative use – biomass (food and feed) and combusted fuels. Total extraction of stock building materials (metal ores and non-metallic minerals) in 2017 reached 55 Gt yr –1. 6 In 1970–2018, it grew 4.3-fold and the ratio of MPR to accumulated in-use capital has nearly been constant since 1990 along with ratio to GDP (Figure 11.3).

End-of-life waste from accumulated stocks along with (re)-manufacturing and construction waste is assessed at 16 Gt yr –1 in 2014 and can be extrapolated in 2018 to 19 Gt yr –1 (Krausmann et al. 2018; Wiedenhofer et al. 2019), or 1.8% from stock of manufactured capital. Less than 6 Gt yr –1 was recycled and used to build the stock (about 10% of inputs). 7 While the circularity gap is still large, and limited circularity was engineered into accumulated stocks, 8 material recycling mitigated some GHG emissions by replacing energy-intensive virgin materials. 9 When the stock saturates, in closed material loops the end-of-life materials waste has to be equal to material input, and primary production therefore has to be equal to end-of-life waste multiplied by unity minus recycling rate. When the latter grows, as the linear metabolism is replaced with the circular one, the share of primary materials production in total material input declines.

Recycling rates for metals are higher than for other materials: the end-of-life scrap input ratio for 13 metals is over 50%, and stays in the range of 25–50% for another ten, but even for metals recycling flows fail to match the required inputs (Graedel et al. 2011). Globally, despite overall recycling rates being at 85%, the all-scrap ratio for steel production in recent years stays close to 35–38% (Gielen et al. 2020; IEA 2021b) ranging from 22% in China (only 10% in 2015) to 69% in the US and to 83% in Turkey (BIR 2020). For end-of-life scrap this ratio declined from 30% in 1995–2010 to 21–25% after 2010 (Gielen et al. 2020; Wang et al. 2021).

For aluminium, the share of scrap-based production grew from 17% in 1962 to 34% in 2010 and stabilised at this level until 2019, while the share of end-of-life scrap grew from 1.5% in 1962 to nearly 20% in 2019 (International Aluminium Institute 2021a). The global recycling (mostly mechanical) rate for plastics is only 9–10%10 (Geyer et al. 2017; Saygin and Gielen 2021), and that for paper progressed from 34% in 1990 to 44% in 2000 and to over 50% in 2014–2018 (IEA 2020b).

The limited impacts of material efficiency factors on industrial GHG emissions trends reflect the lack of integration of material efficiency in energy and climate policies which partly results from the inadequacy of monitored indicators to inform policy debates and set targets; 11 lack of high-level political focus and industrial lobbying; uncoordinated policy across institutions and sequential nature of decision-making along supply chains; carbon pricing policy lock-in with upstream sectors failing to pass carbon costs on to downstream sectors (due to compensation mechanisms to reduce carbon leakage) and so have no incentives to exploit such options as light-weighting, reusing, remanufacturing, recycling, diverting scrap, extending product lives, using products more intensely, improving process yields, and substituting materials (Skelton and Allwood 2017; Gonzalez Hernandez et al. 2018b; Hilton et al. 2018). Poor progress with material efficiency is part of the reason why industrial GHG emissions are perceived as ‘hard to abate’, and many industrial low-carbon trajectories to 2050 leave up to 40% of emissions in place (Material Economics 2019; IEA 2021a). The importance of this factor activation rises as in-use material stock is expected to scale up by a factor of 2.2–2.7 to reach 2215–2720 Gt by 2050 (Krausmann et al. 2020). Material extraction in turn is expected to rise to 140–200 Gt yr –1 by 2060 (OECD 2019a; Hertwich et al. 2020) providing unsustainable pressure on climate and environment and calling for fundamental improvements in material productivity.

In 2014–2019, the average annual growth rate (AAGR) of global industrial energy use was 0.4% compared to 3.2% in 2000–2014, following new policies and trends, particularly demonstrated by China 12 (IEA 2020b,d). Whatever metric is applied, industry (coal transformation, mining, quarrying, manufacturing and construction) driven mostly by material production, dominates global energy consumption. About two fifths of energy produced globally goes to industry, directly or indirectly. Direct energy use (including energy used in coal transformation) accounts for nearly 30% of total final energy consumption. When supplemented by non-energy use, the share for the post-AR5 period (2015–2019) stands on average close to 40% of final energy consumption, and at 28.5% of primary energy use. 13 With an account of indirect energy use for the generation of power and centralised heat to be consumed in industry, the latter scales up to 37%. Industrial energy use may be split by: material production and extraction (including coal transformation): 51% on average for 2015–2019; non-energy use (mostly chemical feedstock): 22%14 ; and other energy use (equipment, machinery, food and tobacco, textiles, leather, etc.): 27%. Energy use for material production and feedstock 15 makes about three quarters (73%) of industrial energy consumption and is responsible for 77% of its increment in 2015–2019 (based on IEA 2021a).

For over a century, industrial energy efficiency improvements have partially offset growth in GHG emissions. Industrial energy use per tonne of extracted materials (ores and building materials as a proxy for materials going through the whole production chain to final products) fell by 20% in 2000–2019 and by 15% in 2010–2019, accelerated driven by high energy prices to 2.4% yr –1 in 2014–2019, matching the values observed back in 1990–2000 (Figure 11.2). Assessed per value added using market exchange rates, industrial energy intensity globally dropped by 12% in 2010–2018, after its 4% decline in 2000–2010, resulting in 2000–2018 decline by 15% (IEA 2020b,a). The 2020 COVID crisis slowed down energy intensity improvements by shifting industrial output towards more energy-intensive basic materials (IEA 2020e). Specific energy consumption per tonne of iron and steel, chemicals and cement production in 2019 was about 20% below the 2000 level (IEA 2020b,a). This progress is driven by moving towards best available technologies (BATs) for each product through new and highly efficient production facilities in China, India and elsewhere, and by the contribution from recycled scrap metals, paper and cardboard.

Physical energy intensity for the production of materials typically declines and then stabilises at the BAT level once the market is saturated, unless a transformative new technology enters the market (Gutowski et al. 2013; Crijns-Graus et al. 2020; IEA 2021a). Thus, the energy saving effect of switching to secondary used material comes to the forefront, as energy consumption per tonne for many basic primary materials approach the BATs. This highlights the need to push towards circular economy, materials efficiency, reduced demand, and fundamental process changes (e.g., towards electricity and hydrogen-based steel making). Improved recycling rates allow for a substantial reduction in energy use along the whole production chain – material extraction, production, and assembling – which is in great excess of energy used for collection, separation, treatment, and scrap recycling minus energy used for scrap landfilling. The International Energy Agency (IEA 2019b) estimates that by increasing the recycling content of fabricated metals, average specific energy consumption (SEC) for steel and aluminium may be halved by 2060. Focusing on whole systems ‘integrative design’ expands efficiency resource much beyond the sum of potentials for individual technologies. Material efficiency coupled with energy efficiency can deliver much greater savings than energy efficiency alone. Gonzalez Hernandez et al. (2018b) stress that presently about half of steel or aluminium are scrapped in production or oversized for targeted services. They show that resource efficiency expressed in exergy as a single metric for both material and energy efficiency for the global iron and steel sector is only 33%, while secondary steel-making is about twice as efficient (66%) as ore-based production (29%). While shifting globally in ore-based production from the average to the best available level can save 6.4 EJ yr –1, the saving potential of shifting to secondary steel-making is 8 EJ yr –1, and is limited mostly by scrap availability and steel quality requirements.

11.2.2New Trends in Emissions

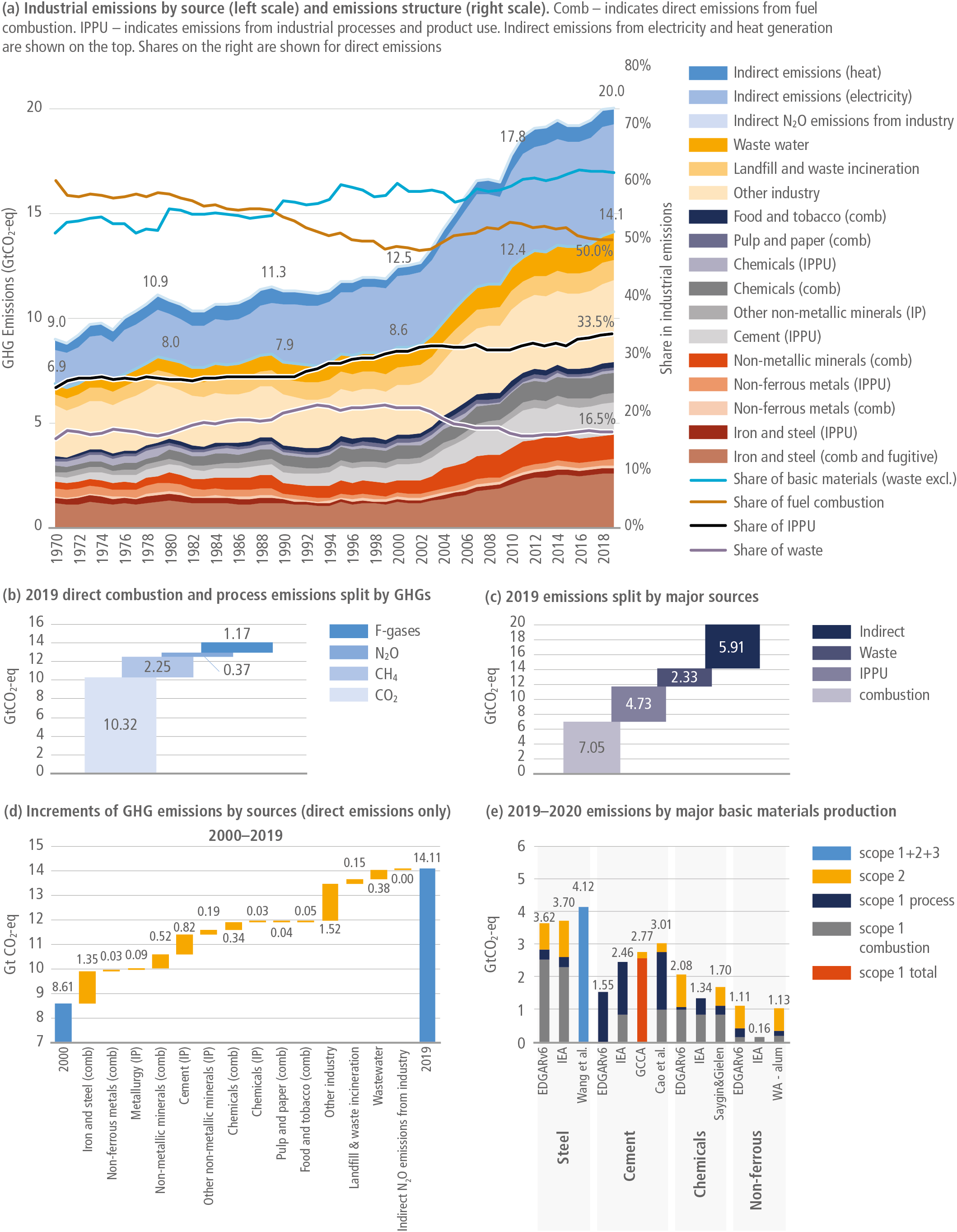

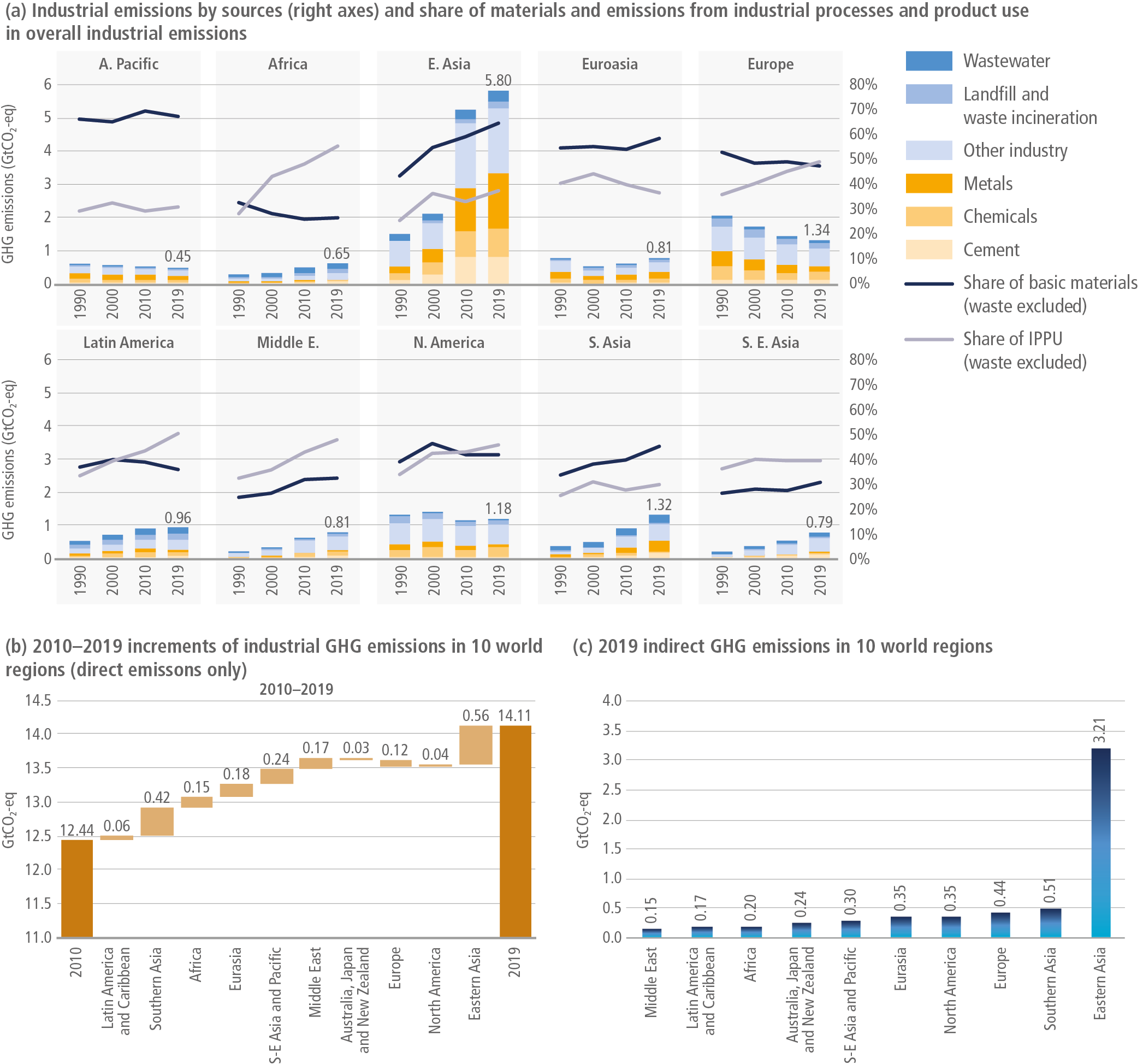

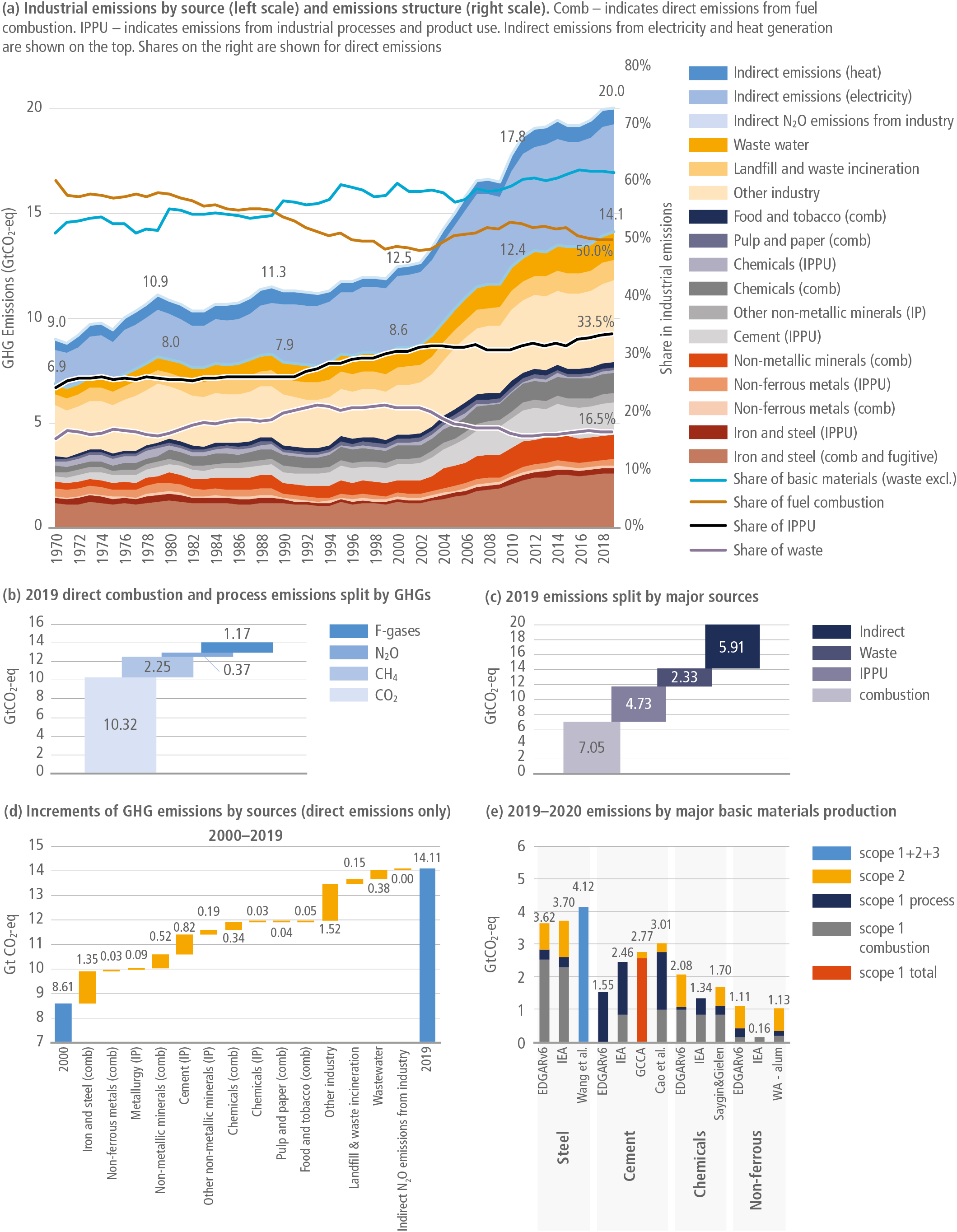

GHG emissions attributable to the industrial sector (see Chapter 2) in 2019 originate from industrial fuel combustion (7.1 GtCO2-eq directly and about 5.9 Gt indirectly from electricity and heat generation 16 ); industrial processes (4.5 GtCO2-eq) and products use (0.2 Gt), as well as from waste (2.3 Gt) (Figure 11.4a,b). Overall industrial direct GHG emissions amount to 14.1 GtCO2-eq (Figure 11.4c and Table 11.1), and scales up to 20 GtCO2-eq after indirect emissions are added, 17 putting industry (24%, direct emissions) second after the energy sector in total GHG emissions and lifting it to the leading position after indirect emissions are allocated (34% in 2019). 18 The corresponding shares for 1990–2000 were 21% for direct emissions and 30% for both direct and indirect (Crippa et al. 2021; Lamb et al. 2021; Minx et al. 2021). As the industrial sector is expected to decarbonise slower than other sectors it will keep this leading position for the coming decades (IEA 2021a). In 2000–2010, total industrial emissions grew faster (3.8% yr –1) than in any other sector (see Chapter 2), mostly due to the dynamics shown by basic materials extraction and production. Industry contributed nearly half (45%) of overall incremental global GHG emissions in the 21st century.

Figure 11.4 | Industrial sector direct global greenhouse gas (GHG) emissions. Source: calculated based on emissions data from Crippa et al. (2021) and Minx et al. (2021). Indirect emissions were assessed using IEA (2021b). For (e): Cao et al. (2020); IEA (2020b, 2021a); GCCA (2021a); International Aluminium Institute (2021a); and Wang et al. (2021).

Industrial sector GHG emissions accounting is complicated by carbon storage in products (Levi and Cullen 2018). About 35% of chemicals’ mass is CO2, which is emitted at use stage – decomposition of fertilisers, or plastic waste incineration (Saygin and Gielen 2021), and sinks. Recarbonation and mineralisation of alkaline industrial materials and wastes (also known as the ‘sponge effect’) provide 0.6–1 GtCO2 yr –1 uptake by cement-containing products 19 (Cao et al. 2020; Guo et al. 2021); see Section 11.3.6 for further discussion in decarbonisation context.

In 1970–1990, industrial direct combustion-related emissions were growing modestly, and in 1990–2000 even switched to a slowly declining trend, steadily losing their share in overall industrial emissions. Electrification was the major driver behind both indirect and total industrial emissions in those years. This quiet evolution was interrupted in the beginning of the 21st century, when total emissions increased by 60–68% depending on the metric applied (the fastest growth ever seen). In 2000–2019 iron, steel and cement absolute GHGs increased more than any other period in history (Bashmakov 2021). Emissions froze temporarily in 2014–2016, partly in the wake of the financial crisis, but returned to their growth trajectory in 2017–2019 (Figure 11.4a).

The largest incremental contributors to industrial emissions in 2010–2019 were industrial processes at 40%, then indirect emissions (25%), and only then direct combustion (21%), followed by waste (14%; Figure 11.4). Therefore, to stop emission growth and to switch to a zero-carbon pathway more mitigation efforts should be focused on industrial processes, product use and waste decarbonisation, along with the transition to low-carbon electrification (Hertwich et al. 2020).

Basic materials production dominates both direct industrial GHG emissions (about 62%, waste excluded)20 as well as direct industrial CO2 emissions (70%), led by iron and steel, cement, chemicals, and non-ferrous metals (Figure 11.4e). Basic materials also contribute 60% to indirect emissions. In a zero-carbon power world, with industry lagging behind in the decarbonisation of high-temperature processes and feedstock, it may replace the energy sector as the largest generator of indirect emissions embodied in capital stock. 21 According to Circle Economy (2020) and Hertwich et al. (2020), GHG emissions embodied in buildings and infrastructure, machinery and transport equipment exceed 50% of their present carbon footprint.

In 1970–2000, direct GHG emissions per unit of energy showed a steady decline interrupted by noticeable growth in 2001–2018 driven by the fast expansion of steel and cement production (Figure 11.5; IEA 2021a). Non-energy-related GHG emissions per unit of extracted materials decline continuously, as the share of not carbon intensive building materials (aggregates and sand) grows.

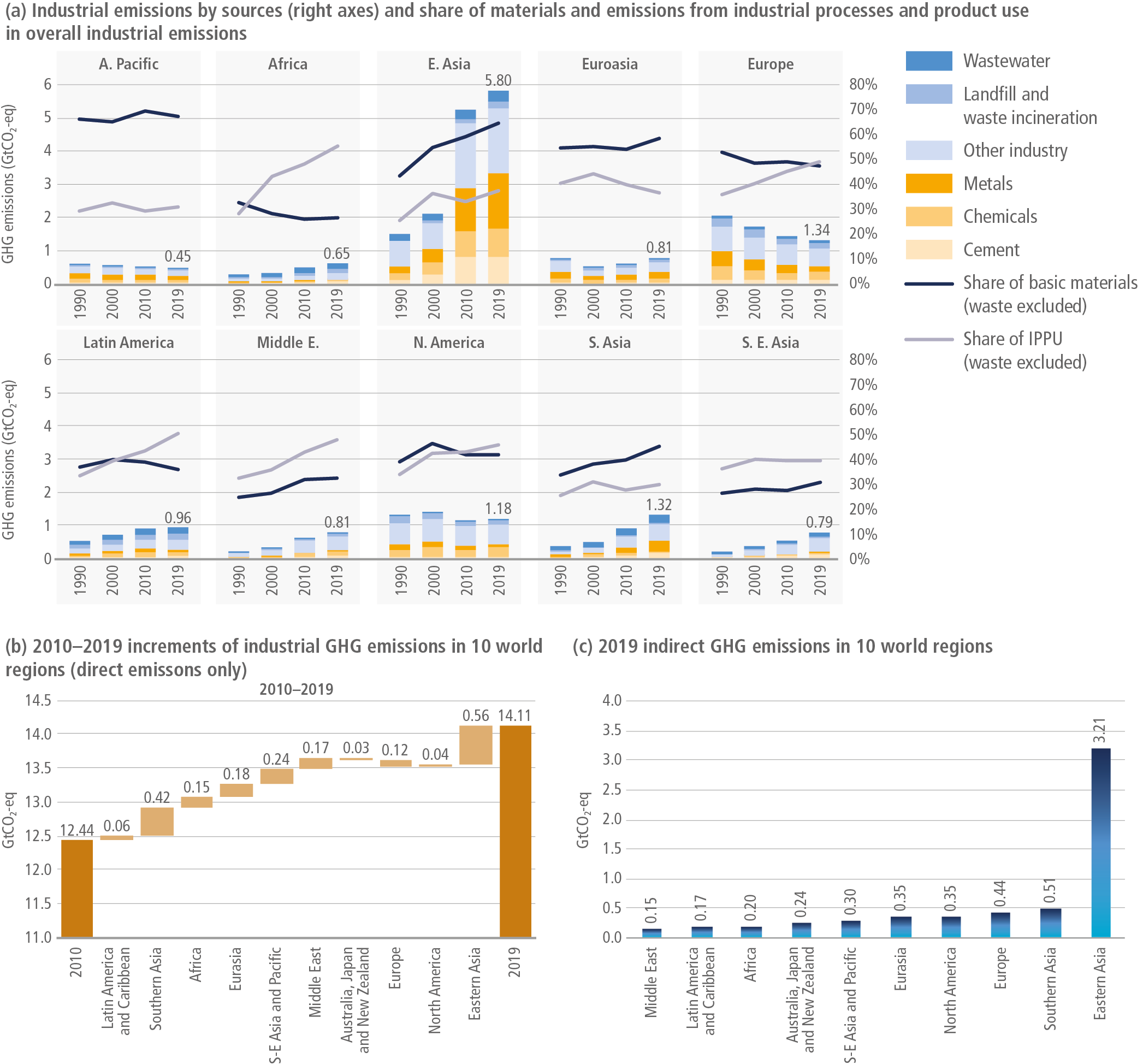

Figure 11.5 | Industrial sector greenhouse gas (GHG) emissions in 10 world regions (1990–2019). Source: calculated based on emissions data from Crippa et al. (2021). Indirect emissions were assessed using IEA (2021b).

|Iron and steel carbon intensity stagnated in 1995–2015 due to rapid growth in carbon-intensive production in some countries (Wang et al. 2021). For aluminium carbon intensity declined in 2010–2019 by only 2% (International Aluminium Institute 2021a). The carbon intensity of cement-making since 2010 is down by only 4%. In 1990–2019 it fell by 19.5%, mostly due to energy efficiency improvements (by 18.5%) as the carbon intensity of the fuel mix declined only by 3% (GCCA 2021b). Historical analysis shows the carbon intensity of steel production has declined with ‘stop and go’ patterns in 50–60-year cycles, reflective of the major jumps in best available technology (BAT). From 1900 to 1935 and from 1960 to 1990 specific scope 1 + 2 + 3 emissions fell by 1.5–2.5 tCO2 per tonne, or as much as needed now to achieve net zero. While historical declines were mostly due to commissioning large capacities with new technologies, with total emissions growing, by 2050 and beyond the decline will likely materialise via new ultra-low emission capacity replacements pushing absolute emissions to net zero (Bataille et al. 2021b).

11.2.3Industrial Development Patterns and Supply Chains (Regional)

The dramatic increase in industrial emissions after 2000 is clearly associated with economic growth in Asia, which dominated both absolute and incremental emissions (Figure 11.5 a,b).

More recent 2010 to 2019 trends show that regional contributions to additional emissions are distributed more evenly, while a large part still comes from Asian countries, where both rates of economic growth and the share of industrial emissions much exceed the global average. All other regions also contributed to total industrial GHG emissions. Structural shifts towards emissions from industrial processes and products use are common for many regions (Figure 11.5 a).

Economic development. Regional differences in emission trends are determined by the differences observed in economic development, trade and supply chain patterns. The major source of industrial emissions is production of energy-intensive materials, such as iron and steel, chemicals and petrochemicals, non-ferrous metals and non-metallic products. Steel and cement are key inputs to urbanisation and infrastructure development (buildings and infrastructure are responsible for about three fourths of the steel stock). Application of a ‘services-stock-flow-emissions’ perspective (Wiedenhofer et al. 2019; Bashmakov 2021; Haberl et al. 2021) shows that relationship patterns between stages of economic development, per capita stocks and flows of materials are not trivial with some clear transition points. Cao et al. (2017) mapped countries by four progressive stages in cement stock per capita S-shape evolution as a function of income and urbanisation: initial stage for developing countries with a low level and slow linear growth; take-off stage with accelerated growth; slowdown stage; and finally a shrinking stage (represented by just a few countries with very high incomes exceeding 40,000 USD2010 per capita) and urbanisation levels above 80%. Bleischwitz et al. (2018) use a similar approach with five stages to study material saturation effects for apparent consumption and stocks per capita for steel, cement, aluminium, and copper. This logic may be generalised to other materials from which in-use stock is built. While globally cement in-use stock is about 12 tonnes per capita, in developed countries it is 15–30 tonnes per capita, but the order of magnitude is lower in developing states with high per capita escalation rates (Cao et al. 2017). When stocks for some materials saturate – per capita stock peaks – the ‘scrap age’ is coming (Pauliuk et al. 2013a). Steel in-use stock has already saturated in advanced economies at 14 ± 2 tonnes per capita due to largely completed urbanisation and infrastructure developments, and a switch towards services-dominated economy. This saturation level is three to four times that of the present global average, which is below 4 tonnes per capita (Pauliuk et al. 2013a; Graedel et al. 2011; Wiedenhofer et al. 2019). China is entering the maturing stage of steel and cement consumption, resulting in a moderate projection of additional demand followed by expected industrial emissions peaking in the next 10 to 15 years (Zhou et al. 2013; Bleischwitz et al. 2018; OECD 2019a; Wu et al. 2019; Zhou et al. 2020). But many developing countries are still urbanising, and the growing need for infrastructure services results in additional demand for steel and cement. Materials intensity of the global economy is projected by OECD (2019a) to decline at 1.3% yr –1 until 2060, driven by improving resource efficiency and the switch to circular economy, but with a projected tripling of global GDP it means a doubling of projected materials use (OECD 2019a). Under the business-as-usual scenario, India’s demand for steel may more than quadruple over the next 30 years (de la Rue du Can et al. 2019; Dhar et al. 2020). In the IEA (2021a) net-zero-energy scenario, the saturation effect along with material efficiency counterbalances activity effects and keeps demand growth for basic materials modest while escalate demand for critical materials (copper, lithium, nickel, graphite, cobalt and others).

International trade and supply chain. In Equation 11.1 the share of allocated emissions (Dm) equals unity when territorial emission is considered, and to the ratio of domestically used materials to total material production for consumption-based emission accounting. Tracking consumption-based emissions provides additional insights in the global effectiveness of national climate policies. Carbon emissions embodied in international trade are estimated to account for 20–30% of global carbon emissions (Meng et al. 2018; OECD.Stat 2019) and are the reason for different emissions patterns of OECD versus non-OECD countries (Chapter 2).

Based on OECD.Stat (2019) datasets, 2015 CO2 emissions embodied in internationally traded industrial products (manufacturing and mining, excluding fuels) by all countries are assessed at 3 GtCO2, or 30% of direct CO2 emissions in the industrial sector as reported by Crippa et al. (2021). OECD countries collectively have reduced territorial emissions (shares of basic materials in direct emissions in those regions decline (Figure 11.5 b), but demonstrated no progress in reducing outsourced emissions embedded in imported industrial products (Arto and Dietzenbacher 2014; OECD.Stat 2019). Accounting for net carbon emissions embodied in international trade of only industrial products (1283 million tCO2 in 2015) escalates direct OECD industrial CO2 emissions (1333 million tCO2 of energy-related and 502 million tCO2 of industrial processes) 1.7 fold, 2.3-fold for the US, 1.5-fold for the EU, and more than triples it for the UK, while cutting (Dm) by a third for China and Russia (OECD.Stat 2019; IEA 2020f). In most OECD economies, the amount of CO2 embodied in net import from non-OECD countries is equal to, or even greater than, the size of their Paris 2030 emissions reduction commitments. In the UK, the Parliament Committee on Energy and Climate Change requested that a consumption-based inventory be complementarily used to assess the effectiveness of domestic climate policy in delivering absolute global emissions reductions (Barrett et al. 2013; UKCCC 2019a). It should be noted that the other side of the coin is that exports from countries with lower production carbon intensities can lead to overall less emissions than if production took place in countries with high carbon intensities, which may become critical in the global evolution toward lower emissions. The evolution of Dm to the date was driven mostly by factors other than carbon regulation often equipped with carbon leakage prevention tools. Empirical tests have failed to date to detect meaningful ‘carbon leakage’ and impacts of carbon prices on net import, direct foreign investments, volumes of production, value added, employment, profits, and innovation in industry (Sartor 2013; Branger et al. 2016; Saussay and Sato 2018; Ellis et al. 2019; Naegele and Zaklan 2019; Acworth et al. 2020; Carratù et al. 2020; Pyrka et al. 2020; Zachmann and McWilliams 2020). In the coming years, availability of large low-cost renewable electricity potential and cheap hydrogen may become a new driver for relocation of such carbon intensive industries as steel production (Bataille 2020a; Gielen et al. 2020; Bataille et al. 2021a; Saygin and Gielen 2021).

11.3Technological Developments and Options

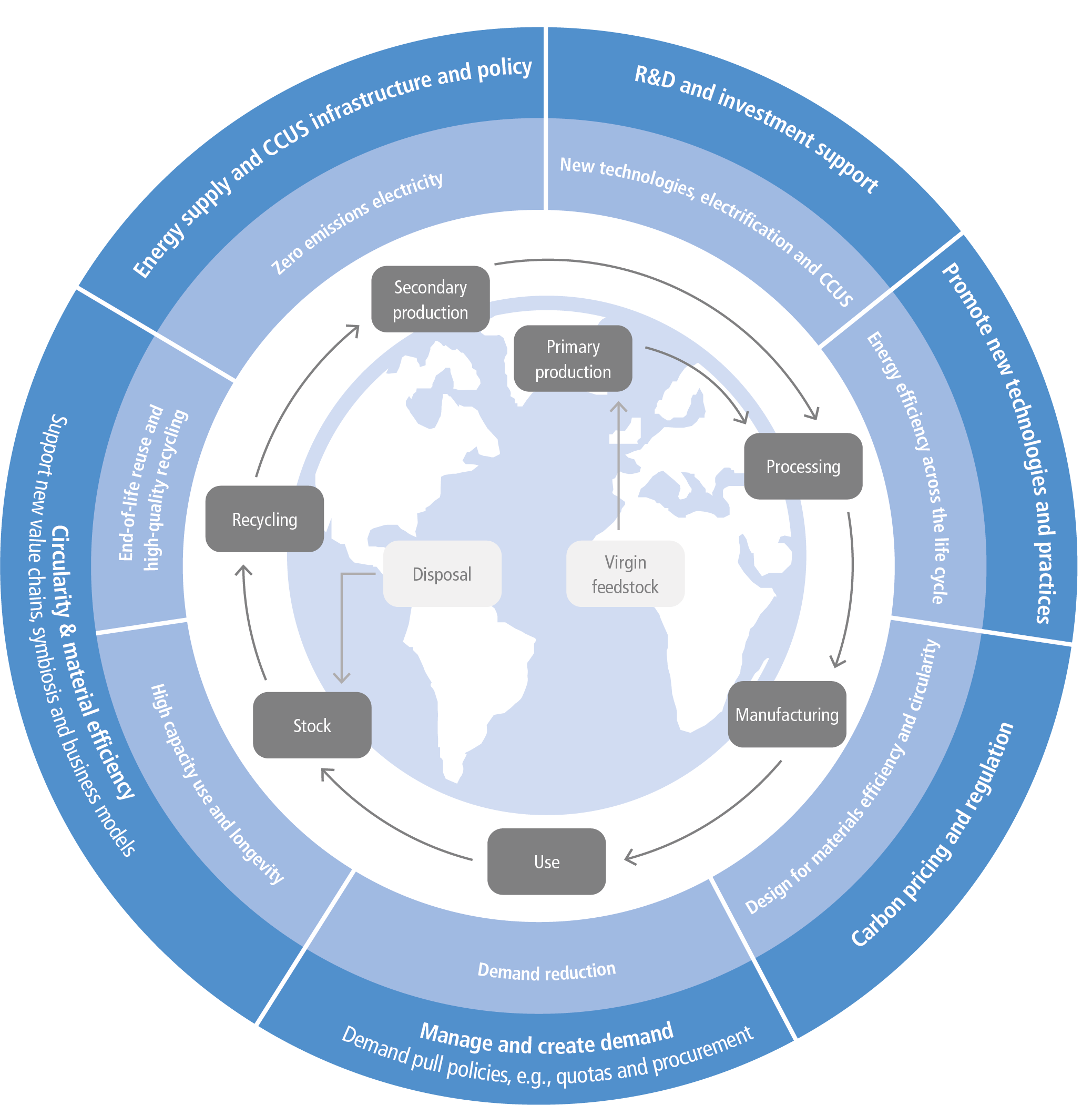

The following overview of technical developments and mitigation options which relate to the industrial sector is organised in six equally important strategies: (i) demand for materials, (ii) materials efficiency, (iii) circular economy and industrial waste, (iv) energy efficiency, (v) electrification and fuel switching, and (vi) CCUS, feedstock and biogenic carbon. Each strategy is described in detail, followed by a discussion of possible overlaps and interactions between strategies and how conflicts and synergies can be addressed through integration of the approaches.

11.3.1Demand for Materials

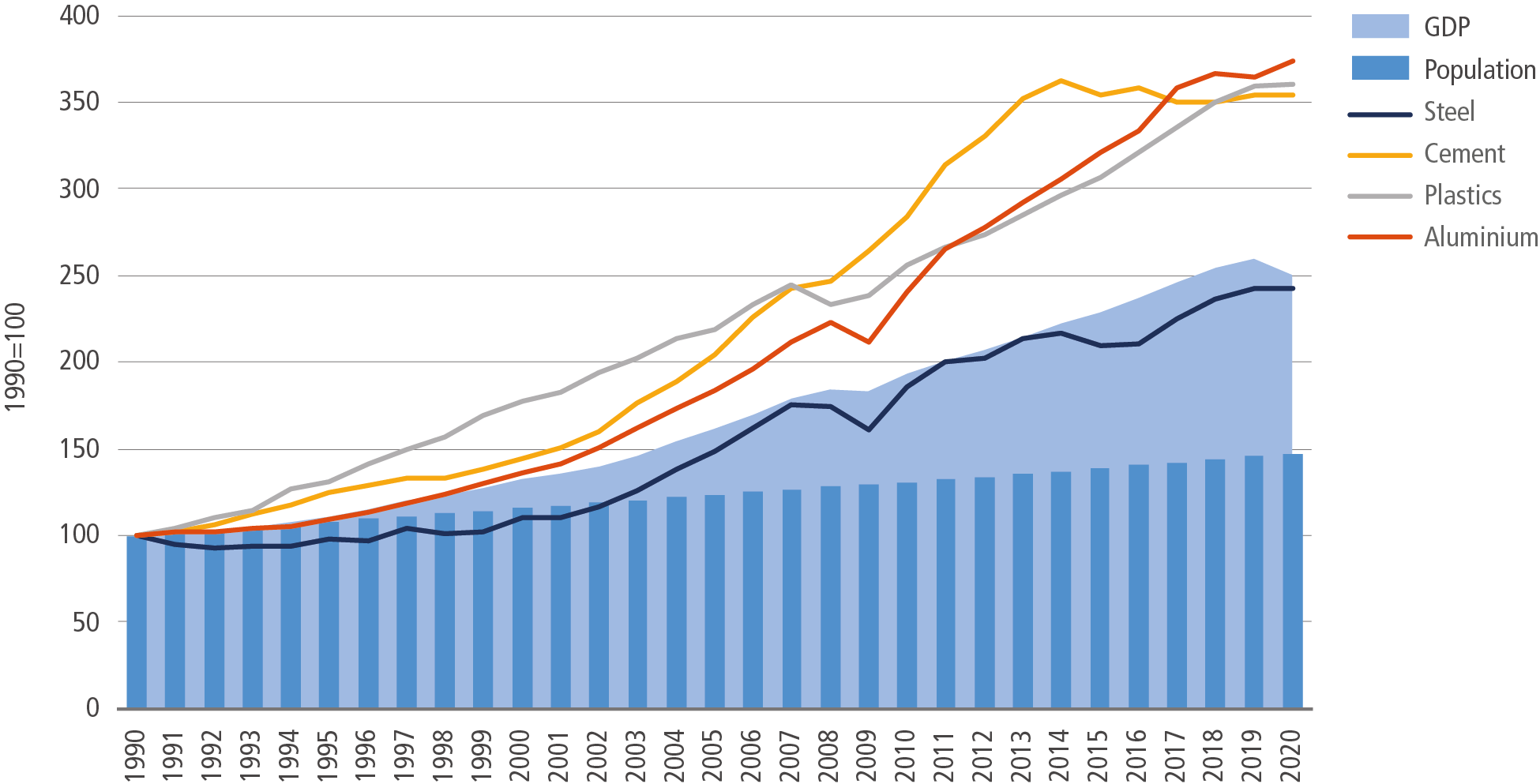

Demand for materials is a key driver of energy consumption and CO2 emissions in the industrial sector. Rapid growth in material demand over the last quarter century has seen demand for key energy-intensive materials increase 2.5- to 3.5-fold (Figure 11.6), with growth linked to, and often exceeding, population growth and economic development. The International Energy Agency (IEA) explains, ‘as economies develop, urbanise, consume more goods and build up their infrastructure, material demand per capita tends to increase considerably. Once industrialised, an economy’s material demand may level off and perhaps even begin to decline’ (IEA 2019b).

Figure 11.6 | Growth in global demand for selected key materials and global population, 1990–2019. Notes: based on global values, shown indexed to 1990 levels (=100). Steel refers to crude steel production. Aluminium refers to primary aluminium production. Plastic refers to the production of a subset of key thermoplastic resins. Cement and concrete follow similar demand patterns. Sources: 1990–2018: IEA (2020b). 2019–2020: GCCA (2021a); International Aluminium Institute (2021a); Statista (2021b); U.S. Geological Survey (2021); World Bank (2021); World Steel Association (2021).

The Kaya-like identity presented earlier in the chapter (Equation 11.1) suggests that material demand can be decoupled from population and economic development by two means: (i) reducing the accumulated material stock (MStock) used to deliver material services; and (ii) reducing the material (MPR+MSE) required to maintain material stocks (MStock). Such material demand reduction strategies are linked upstream to material efficiency strategies (the delivery of goods and services with less material demand, and thus energy and emissions) and to demand reduction behaviours, through concepts such as sufficiency, sustainable consumption and social practice theory (Spangenberg and Lorek 2019). Materials demand can also be influenced through urban planning, building codes and related socio-cultural norms that shape the overall demand for square metres per capita of floor space, mobility and transport infrastructures (Chapter 5).

Modelling suggests that per capita material stocks saturate (level off) in developed countries and decouple from GDP. Pauliuk et al. (2013b) demonstrated this saturation effect in an analysis of in-use steel stocks in 200 countries, showing that per capita steel in stocks in countries with a long industrial history (e.g., USA, UK, Germany) had saturation levels between 11 and 16 tonnes. More recently, Bleischwitz et al. (2018) confirmed the occurrence of a saturation effect for four materials (steel, cement, aluminium and copper) in four industrialised countries (Germany, Japan, UK and USA) together with China. These findings have led to the revision of some material demand forecasts, which previously had been based solely on population and economic trends.

The saturation effect for material stocks is critical for managing material demand in developed countries. Materials are required to meet demand for the creation of new stocks and the maintenance of existing stocks (Gutowski et al. 2017). Once saturation is attained the need for new stocks is minimised, and materials are only required for replacing old stocks and maintenance. Saturation allows material efficiency strategies (such as light-weight design, longer lifetimes, and more intense use) to reduce the required per capita level of material stocks, and material circularity strategies (closing material loops through remanufacture, reuse and recycling) to lessen the energy and carbon impacts required to maintain the material stock. However, it should be noted that some materials still show little evidence of saturation (i.e., plastics, see Box 11.2). Furthermore, meeting climate change targets in developed countries will require the construction of new low-carbon infrastructures (i.e., renewable energy generation, new energy distribution and storage systems, electric vehicles and building heating systems) which may increase demand for emissions intensive materials (i.e., steel, concrete and glass).

For developing countries, who are still far from saturation levels, strong growth for new products and the creation of new infrastructure capacity may still drive global material demand. However, there is an expectation that economic development can be achieved at lower per capita material stock levels, based on the careful deployment of material efficiency and circularity by design (Grubler et al. 2018).

11.3.2Material Efficiency

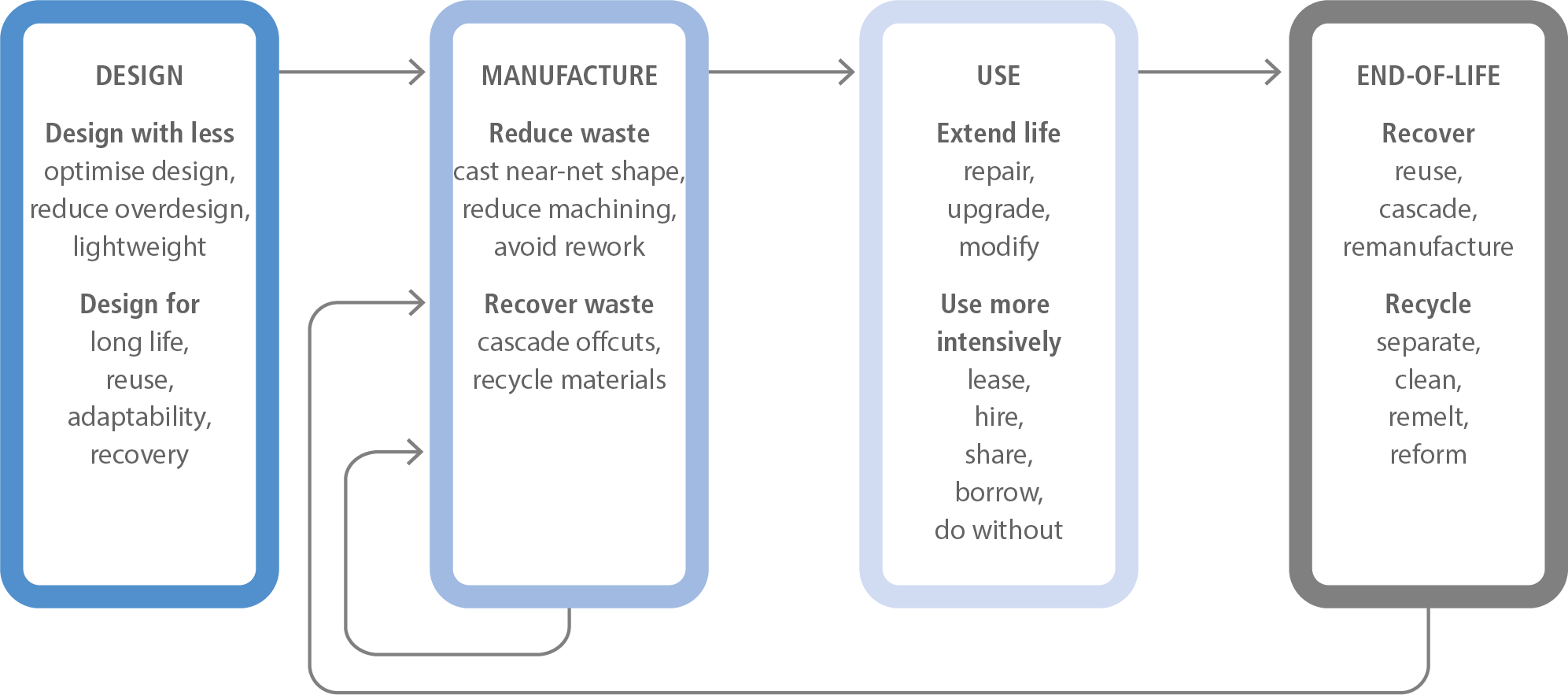

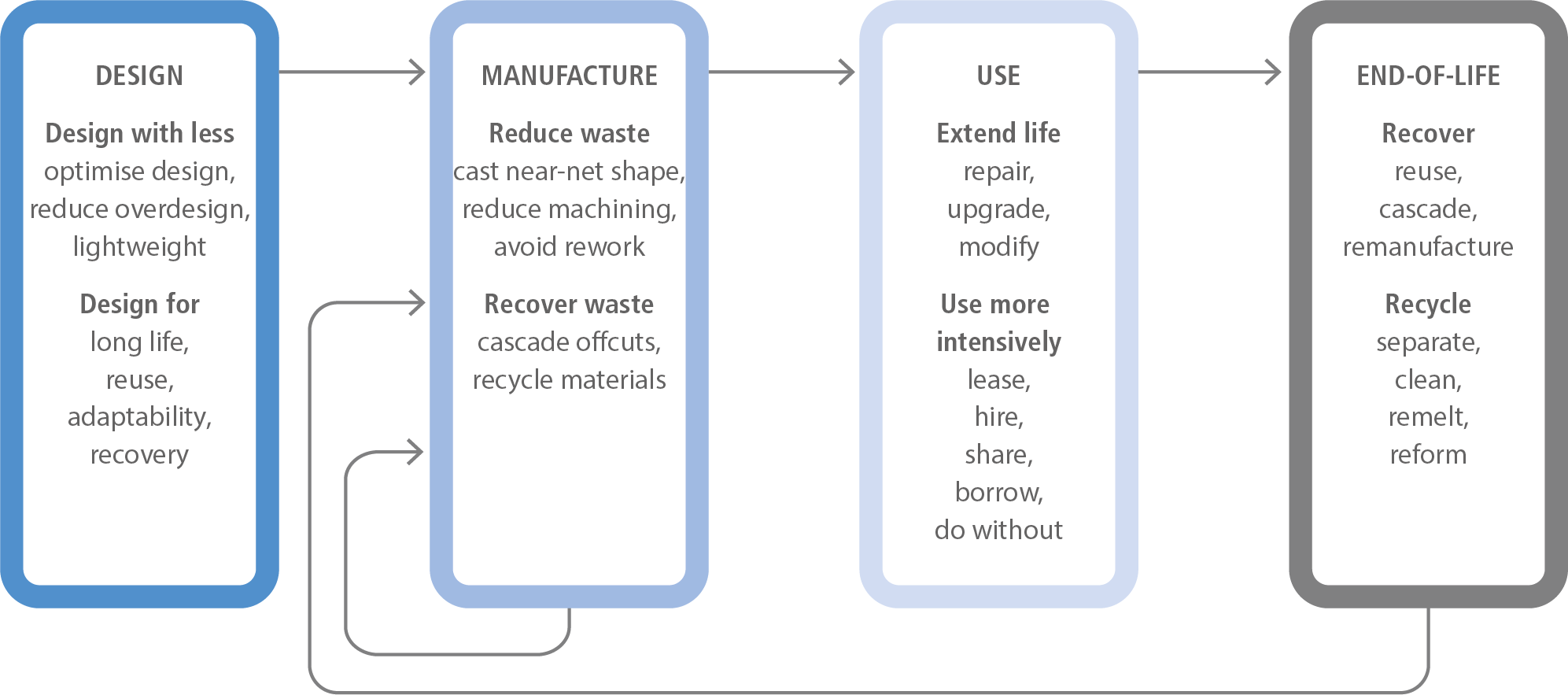

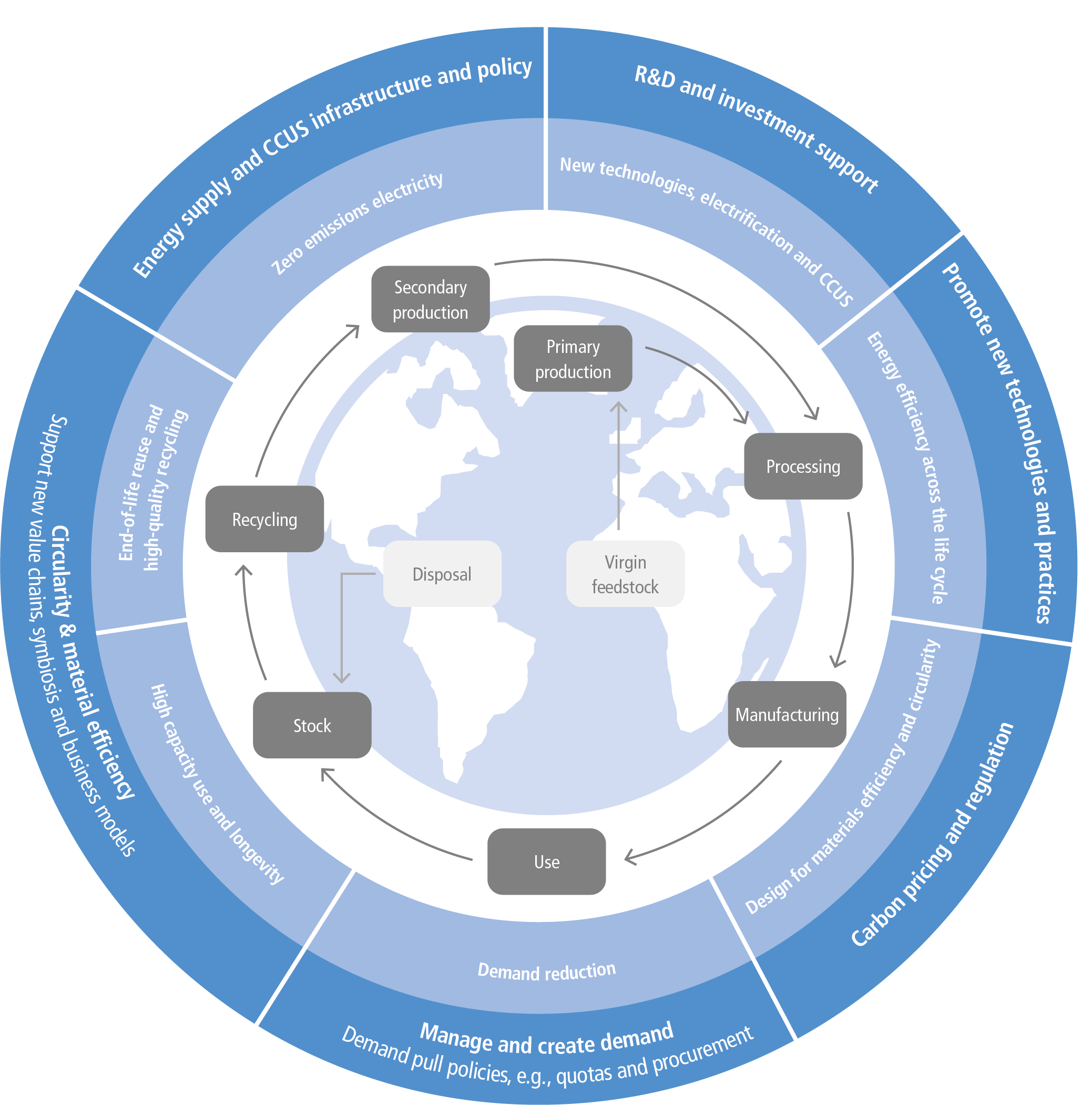

Material efficiency (ME) – the delivery of goods and services with less material – is increasingly seen as an important strategy for reducing GHG emissions in industry (IEA 2017, 2019b). Options to improve ME exist at every stage in the lifecycle of materials and products, as shown in Figure 11.7. This includes: designing products which are lighter, optimising to maintain the end-use service while minimising material use, designing for circular principles (i.e., longer life, reusability, repairability, and ease of high-quality recycling); pushing manufacturing and fabrication process to use materials and energy more efficiently and recover material wastes; increasing the capacity, intensity of use, and lifetimes of product in use; improving the recovery of materials at the end of life, through improved remanufacturing, reuse and recycling processes. For more specific examples see Allwood et al. (2012); Lovins (2018); Hertwich et al. (2019); Scott et al. (2019); and Rissman et al. (2020).

Figure 11.7 | Material efficiency (ME) strategies across the value chain. Source: derived from strategies in Allwood et al. (2012).

ME provides plentiful options to reduce emissions, yet because interventions are dispersed across supply chains and span many different stakeholders, this makes assessing mitigation potentials and costs more challenging. For this reason, ME interventions have traditionally been under-represented in climate change scenario modelling and integrated assessment models (IAMs) (Grubler et al. 2018; Allwood 2018). However, two advances in the modelling of materials flows have underpinned the recent emergence of ME options being included in climate scenario modelling.

Firstly, over many years, the academic community has built up detailed global material-flow maps of the processing steps involved in making energy-intensive materials. Some prominent recent examples include: steel (Gonzalez Hernandez et al. 2018b), pulp and paper (Van Ewijk et al. 2018), petrochemicals (Levi and Cullen 2018). In addition, material-flow maps at the regional and sectoral levels have flourished, for example: steel (Serrenho et al. 2016) and cement (Shanks et al. 2019) in the UK; automotive sheet-metal (Horton et al. 2019); and steel-powder applications (Azevedo et al. 2018). The detailed and transparent physical mapping of material supply chains in this manner enables ME interventions to be traced back to where emissions are released, and allows these options to be compared against decarbonisation and traditional energy efficiency measures (Levi and Cullen 2018). For example, a recent analysis by Hertwich et al. (2019) makes the link between ME strategies and reducing GHG emissions in buildings, vehicles and electronics, while Gonzalez Hernandez et al. (2018a) examines leveraging ME as a climate strategy in European Union (EU) policy. Research to explore the combined analysis of materials and energy, using exergy analysis (for steel: Gonzalez Hernandez et al. 2018b) allows promising comparisons across industrial sectors.

Secondly, many ME interventions result in immediate GHG emissions savings (short-term), for example, light-weighting products, reusing today’s product components, and improving manufacturing yields. Yet, for other ME actions emissions savings are delayed temporally (long-term). For example, designing a product for future reuse, or with a longer life, only reaps emissions savings at the end of the product life, when emissions for a replacement product are avoided. Many durable products have long lifetimes (cars >10 years, buildings >40 years) which requires dynamic modelling of material stocks, over time, to enable these actions to be included in scenario modelling activities. Consequently, much effort has been invested recently to model material stocks in use, to estimate their lifetimes, and anticipate the future waste and replenishment materials to maintain existing stocks and grow the material stock base. Dynamic material models have been applied to material and product sectors, at the country and global level. These include, for example: vehicles stocks in the UK (Serrenho et al. 2017; Craglia and Cullen 2020) and in China (Liu et al. 2020); buildings stocks in the UK (Cabrera Serrenho et al. 2019), China (Hong et al. 2016; Cao et al. 2018, 2019) and the European Union (Sandberg et al. 2016); electronic equipment in Switzerland (Thiébaud et al. 2017); specific material stocks, such as cement (Cao et al. 2020, 2017), construction materials (Sverdrup et al. 2017; Habert et al. 2020), plastics (Geyer et al. 2017), copper (Daehn et al. 2017), and all metals (Elshkaki et al. 2018); all materials in China (Jiang et al. 2019), Switzerland (Heeren and Hellweg 2019) and the world (Krausmann et al. 2017).

These two advances in the knowledge base have allowed the initial inclusion of some ME strategies in energy and climate change scenario models. The International Energy Agency (IEA) first created a ME scenario (MES) in 2015, with an estimated 17% reduction in industrial energy demand in 2040 (IEA 2015). The World Energy Outlook report includes a dedicated sub-chapter with calculations explicitly on industrial material efficiency (IEA 2019c). They also include ME options in their modelling frameworks and reporting, for example for petrochemicals (IEA 2018a), and in the Material Efficiency in Clean Energy Transitions report (IEA 2019b). In Grubler et al. (2018) 1.5°C Low Energy Demand (LED) scenario, global material output decreases by 20% from today, by 2050, with one-third due to dematerialisation, and two-thirds due to ME, resulting in significant emissions savings. Material Economics’ analysis of Industrial Transformation 2050 (Material Economics 2019), found that resource efficiency and circular economy measures (i.e., ME) could almost halve the 530 MtCO2 yr –1 emitted by the basic materials sectors in the EU by 2050. Finally, the Emissions Gap Report, UNEP (2019) includes an assessment of potential material efficiency savings in residential buildings and cars.

Clearly, more work is required to fully integrate ME strategies into mainstream climate change models and future scenarios. Efforts are focused on endogenising ME strategies within climate change modelling, assessing the synergies and trade-offs which exist between energy efficiency and ME interventions, and building up data for the assessment of emissions saved and the cost of mitigation from real ME actions. This requires analysts to work in cross-disciplinary teams and to engage with stakeholders from across the full breadth of material supply chains. Efforts should be prioritised to foster engagement between the IAM community and emerging ME models based in the Life Cycle Assessment, Resource Efficiency, and Industrial Ecology communities (see also Sharmina et al. 2021).

11.3.3Circular Economy and Industrial Waste

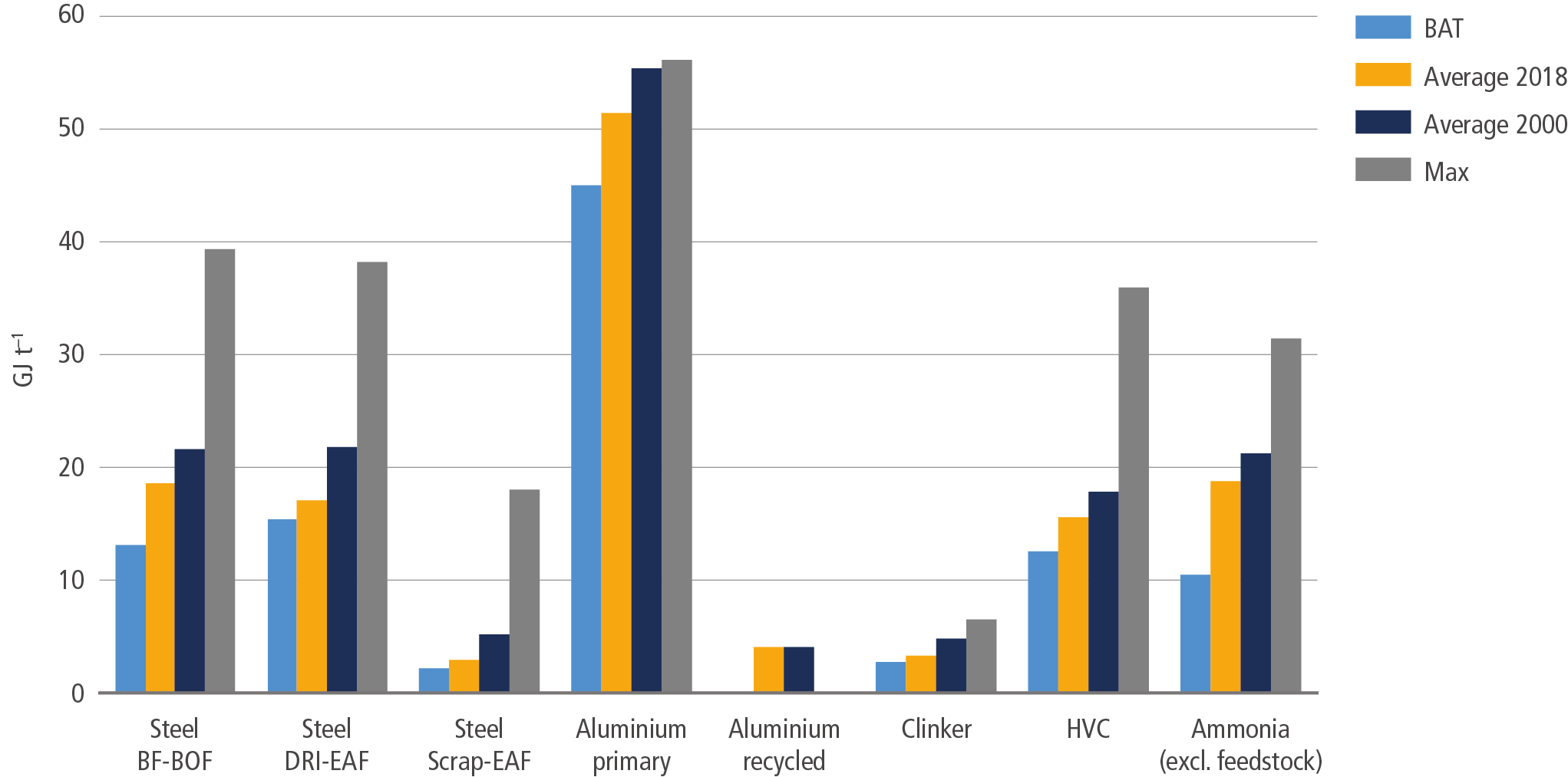

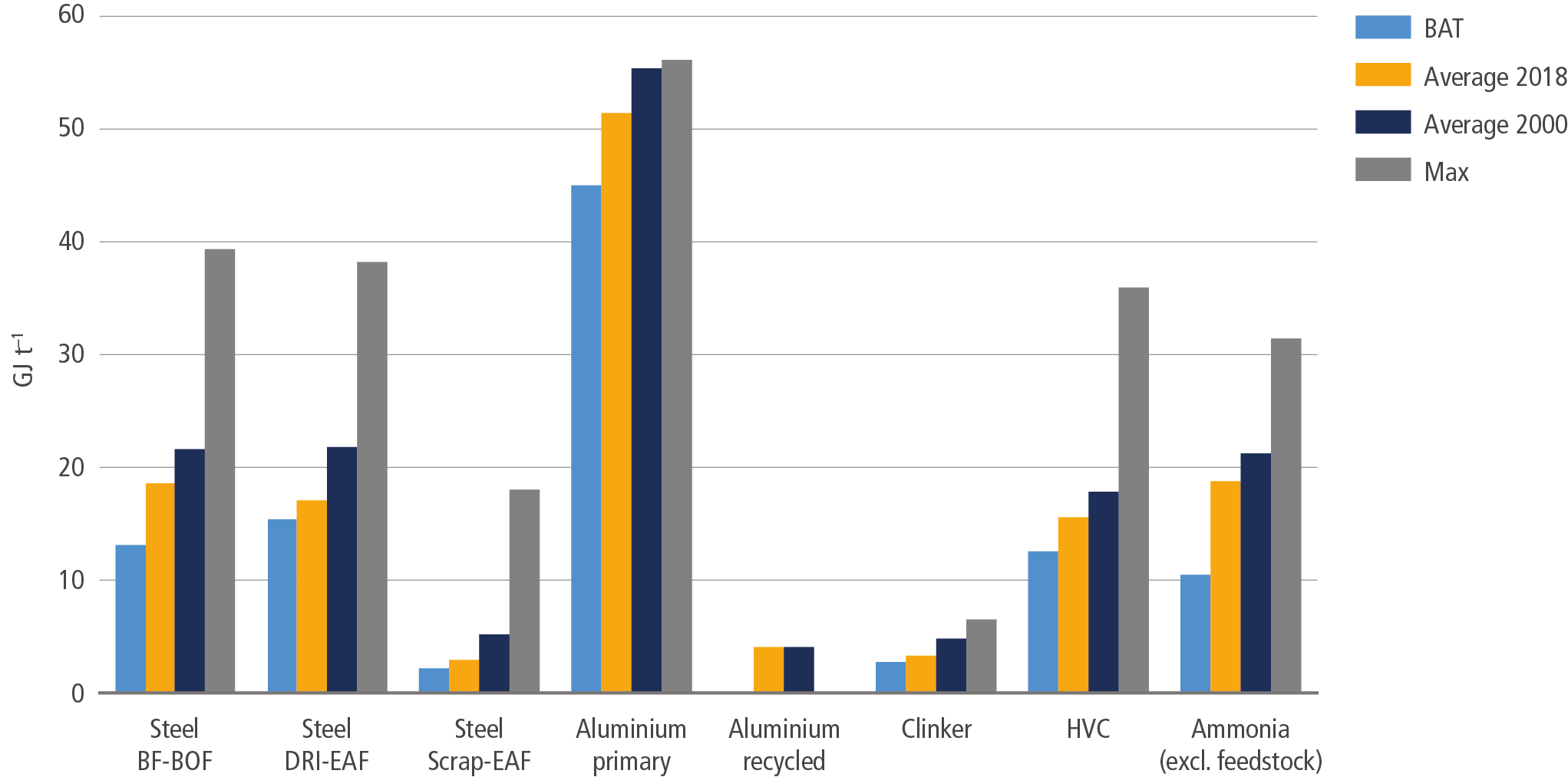

Circular economy (CE) is another effective approach to mitigate industrial GHG emissions and has been widely promoted worldwide since the fourth IPCC assessment report (AR4). From an industrial point of view, CE focuses on closing the loop for materials and energy flows by incorporating policies and strategies for more efficient energy, materials and water consumption, while emitting minimal waste to the environment (Geng et al. 2013). Moving away from a linear mode of production (sometimes referred to as an ‘extract-produce-use-discard’ model), CE promotes the design of durable goods that can be easily repaired, with components that can be reused, remanufactured, and recycled (Wiebe et al. 2019). In particular, since CE promotes reduction, reuse and recycling, a large amount of energy and GHG-intense virgin material processing can be reduced, leading to significant carbon emission reductions. For example, in the case of aluminium, the energy efficiency of primary production is relatively close to best available technology (Figure 11.8), while switching to production using recycled materials requires only about 5% as much energy (Section 11.4.1.4). However, careful evaluation is needed from a lifecycle perspective since some recycling activities may be energy- and emission-intensive, for example, the chemical recycling of plastics (Section 11.4.1.3).

Figure 11.8 | Energy efficiency indicators for basic material production. Energy accounting is based on final energy use. Sectoral boundaries for steel are as defined in IEA (2020c).Sources: calculated based on UNIDO (2010); Saygin et al. (2011); Hasanbeigi et al. (2012); Moya and Pardo (2013); Napp et al. (2014); WBCSD (2016); IEA (2017, 2018b); IEA and WBCSD (2018); IEA (2019b, 2020c); Crijns-Graus et al. (2020); IEA (2020b); International Aluminium Institute (2020).

As one systemic approach, CE can be seen as conducted at different levels, namely, at the micro level (within a single company, such as process integration and cleaner production), meso level (between three or more companies, such as industrial symbiosis or eco‐industrial parks) and macro level (cross‐sectoral cooperation, such as urban symbiosis or a regional eco‐industrial network). Each level requires different tools and policies, such as CE-oriented incentive and tax policies (macro level), and eco-design regulations (micro level). This section is focused on industry and a broader discussion of the CE concept is found in Box 12.2 and Section 5.3.4.2.

Micro level: More firms have begun to implement the concept of CE, particularly multi-national companies, since they believe that multiple benefits can be obtained from CE efforts, and it has become common across sectors (D’Amato et al. 2019). Typical CE tools and policies at this level include cleaner production, eco-design, environmental labelling, process synthesis, and green procurement. For instance, leading chemical companies are incorporating CE into their industrial practices, for example, through the design of more recyclable plastics, a differentiated and market-driven portfolio of resins, films and adhesives that deliver a total package that is more sustainable, cost-efficient and capable of meeting new packaging and plastics preferences. Problematically, at the same time the plastics industry is improving recyclability, it has, for example, been expanding into markets without recycling capacity (Mah 2021). Similarly, automakers are pursuing strategies to increase the portion of new vehicles that are fully recyclable when they reach the end of life, with increasing ambitions for using recycled material, largely motivated by end-of-life vehicle regulations. This will require networks that are available to collect and sort all the materials in vehicles, and policy incentives to do it (Wiebe et al. 2019; Soo et al. 2021).

Meso level: Industrial parks first appeared in Manchester, UK, at the end of the 19th century and they have been implemented in industrialised countries for maximising energy and material efficiency, which also has merit for CO2-emissions reduction, as stated in AR5. Industrial parks reduce the cost of infrastructure and utilities by concentrating industrial activities in planned areas, and are typically founded around large, long-term anchor companies. Complementary industries and services provided by industrial parks can entail diversified effects on the surrounding region and stimulate regional development (Huang et al. 2019a). This is crucial for small and medium enterprises (SMEs) because they often lack access to information and funds for sophisticated technologies.

Typical CE tools and policies at this level include sustainable supply chains and industrial symbiosis. A common platform for sharing information and enhancing communication among industrial stakeholders through the application of information and telecommunication technologies is helpful for facilitating the creation of industrial symbiosis. The main benefit of industrial symbiosis is the overall reduction of both virgin materials and final wastes, as well as reduced/avoided transportation costs from by-product exchanges among tenant companies, which can specifically help small- and medium-sized enterprises to improve their growth and competitiveness. From a climate perspective, this indicates significant industrial emission mitigation since the extraction, processing of virgin materials and the final disposal of industrial wastes are more energy intensive. Also, careful site selection of such parks can facilitate the use of renewable energy. Due to these advantages, eco-industrial parks have been actively promoted, especially in East Asian countries, such as China, Japan and the Republic of Korea (South Korea), where national indicators and governance exist (Geng et al. 2019). For instance, the successful implementation of industrial symbiosis at Dalian Economic and Technological Development Zone has achieved significant co-benefits, including GHG-emission reduction, economic and social benefits, and improved ecosystem functions (Liu et al. 2018). Another case at Ulsan industrial park, South Korea, estimated that 60,522 tonnes of CO2 were avoided annually through industrial symbiosis between two companies (Kim et al. 2018b). The case of China shows the great potential of implementing these measures, estimating 111 million tonnes of CO2 equivalent will be reduced in 213 national-level industrial parks in 2030 compared with 2015 (Guo et al. 2018). As such, South Korea’s national eco-industrial park project has reduced over 4.7 million tonnes of CO2 equivalent through their industrial symbiosis efforts (Park et al. 2019). Meso-level CE solutions have been identified as essential for industrial decarbonisation (Section 11.4.3). Moreover, waste prevention as the top of the so-called ‘waste hierarchy’ can be promoted on the meso level for specific materials or product systems. For instance, the European Environment Agency published a report on plastic waste prevention approaches in all 28 EU-member states (Wilts and Bakas 2019). However, challenges exist for industrial symbiosis activities, such as inter-firm contractual uncertainties, the lack of synergy infrastructure, and the regulations that hamper reuse and recycling. Therefore, necessary legal reforms are needed to address these implementation barriers.

Macro level: The macro level uses both micro- and meso-level tools within a broader policy strategy, addressing the specific challenge of CE as a cross-cutting policy (Wilts et al. 2016). More synergy opportunities exist beyond the boundary of one industrial park. This indicates the necessity of scaling up industrial symbiosis to urban symbiosis. Urban symbiosis is defined as the use of by-products (waste) from cities as alternative raw materials for energy sources for industrial operations (Sun et al. 2017). It is based on synergistic opportunity arising from geographic proximity through the transfer of physical sources (waste materials) for environmental and economic benefits. Japan is the first country to promote urban symbiosis. For instance, the Kawasaki urban symbiosis efforts can save over 114,000 tonnes of CO2 emissions annually (Ohnishi et al. 2017). Another simulation study indicates that Shanghai (the largest Chinese city) has the potential to save up to 16.8 MtCO2 through recycling all the available wastes (Dong et al. 2018). As such, the simulation of urban-energy-symbiosis networks in Ulsan, South Korea, indicates that 243,396 tCO2–1 yr –1 emission and USD48 million yr –1 fuel cost can be saved (Kim et al. 2018a). Moreover, Wiebe et al. (2019) estimate that the adoption of the CE can lead to a significantly lower global material extraction compared to a baseline. Their global results range from a decrease of about 27% in metal extraction to 8% in fossil fuel extraction and use, 8% in forestry products, and about 7% in non-metallic minerals, indicating significant climate change benefits. A macro-perspective calculation on the circulation of iron in Japan’s future society shows that CO2 emissions from the steel sector can be reduced by 56% as per the following assumptions: the amount recovered from social stock is the same as the amount of inflow, and all scrap was used domestically, and the export of steel products is halved (LCS 2018). A key challenge is to go beyond ensuring proper waste management to setting metrics, targets and incentives to preserve the incorporated value in specific waste streams. Estimations for Germany have shown that despite recycling rates of 64% for all solid-waste streams, these activities only lead to a resource-use reduction of only 18% (Steger et al. 2019). In general, the identification of the most appropriate CE method for different countries requires understanding and information exchange on background conditions, local policies and myriad other factors influencing material flows from the local up to the global level (Tapia Carlos et al. 2019). Also, an information platform should be created at the national level so that all the stakeholders can share their CE technologies and expertise, information (such as materials/energy/water consumption data), and identify the potential synergy opportunities.

11.3.4Energy Efficiency

Energy efficiency in industry is an important mitigation option and central in keeping 1.5°C within reach (IPCC SR1.5). It has long been recognised as the first mitigation option in industry (Yeen Chan and Kantamaneni 2016; Nadel and Ungar 2019; IEA 2021a). It allows reduction of the necessary scale of deployment for low-carbon energy supplies and associated mitigation costs (Energy Transitions Commission 2018). The efficiency potentials are greatest in the non-energy-intensive industries and are often relatively limited in energy-intensive ones, such as steel (Pardo and Moya 2013; Kuramochi 2016; Arens et al. 2017). Deep decarbonisation in these subsectors requires fundamental process changes but energy efficiency remains important to reduce costs and the need for low-carbon energy supplies.

Below, we focus mainly on the technical progress and on new options that are reflected in the literature since AR5 and refer the reader there for a broader and deeper treatment of energy efficiency. Digitalisation and the development of industrial high-temperature heat pumps are two notable technology developments that can facilitate energy efficiency improvements.