Chapter 6: Energy systems

This chapter should be cited as:

Clarke, L., Y.-M. Wei, A. De La Vega Navarro, A. Garg, A.N. Hahmann, S. Khennas, I.M.L. Azevedo, A. Löschel, A.K. Singh, L. Steg, G. Strbac, K. Wada, 2022: Energy Systems. In IPCC, 2022: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change[P.R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, J. Malley, (eds.)]. Cambridge University Press, Cambridge, UK and New York, NY, USA. doi: 10.1017/9781009157926.008.

Executive Summary

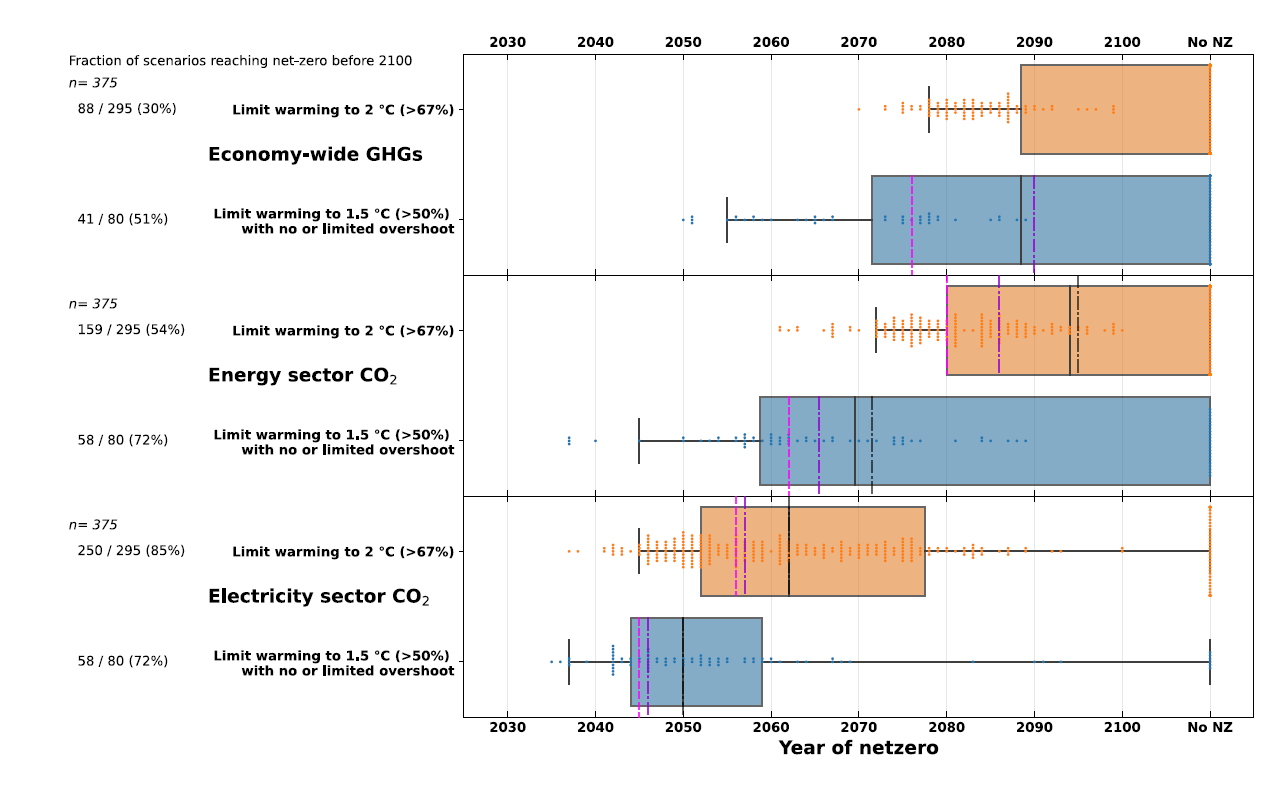

Warming cannot be limited to well below 2°C without rapid and deep reductions in energy system carbon dioxide (CO2) and greenhouse gas (GHG) emissions. In scenarios limiting warming to 1.5°C (>50%) with no or limited overshoot (2°C (>67%) with action starting in 2020), net energy system CO2 emissions (interquartile range) fall by 87–97% (60–79%) in 2050. In 2030, in scenarios limiting warming to 1.5°C (>50%) with no or limited overshoot, net CO2 and GHG emissions fall by 35–51% and 38–52% respectively. In scenarios limiting warming to 1.5°C (>50%) with no or limited overshoot (2°C (>67%)), net electricity sector CO2 emissions reach zero globally between 2045 and 2055 (2050 and 2080). ( high confidence) {6.7}

Limiting warming to well below 2°C will require substantial energy system changes over the next 30 years. This includes reduced fossil fuel consumption, increased production from low- and zero-carbon energy sources, and increased use of electricity and alternative energy carriers. Coal consumption without carbon capture and storage (CCS) falls by 67–82% (interquartile range) in 2030 in scenarios limiting warming to 1.5°C (>50%) with no or limited overshoot. Oil and gas consumption fall more slowly. Low-carbon sources produce 93–97% of global electricity by 2050 in scenarios that limit warming to 2°C (>67%) with action starting in 2020. In scenarios limiting warming to 1.5°C (>50%) with no or limited overshoot (2°C (>67%) with action starting in 2020), electricity supplies 48–58% (36–47%) of final energy in 2050, up from 20% in 2019. ( high confidence) {6.7}

Net-zero energy systems will share common characteristics, but the approach in every country will depend on national circumstances. Common characteristics of net-zero energy systems will include: (i) electricity systems that produce no net CO2 or remove CO2 from the atmosphere; (ii) widespread electrification of end uses, including light-duty transport, space heating, and cooking; (iii) substantially lower use of fossil fuels than today; (iv) use of alternative energy carriers such as hydrogen, bioenergy, and ammonia to substitute for fossil fuels in sectors less amenable to electrification; (v) more efficient use of energy than today; (vi) greater energy system integration across regions and across components of the energy system; and (vii) use of CO2 removal (e.g., direct air carbon capture and storage (DACCS) and bioenergy with carbon capture and storage (DACCS, BECCS)) to offset any residual emissions. (high confidence) {6.6}

Energy demands and energy sector emissions have continued to rise. From 2015 to 2019, global final energy consumption grew by 6.6%, CO2 emissions from the global energy system grew by 4.6%, and total GHG emissions from energy supply rose by 2.7%. Methane emissions, mainly fugitive emissions from oil, gas, and coal, accounted for 18% of GHG emissions in 2019. Coal electricity capacity grew by 7.6% between 2015 and 2019, as new builds in some countries offset declines in others. Total consumption of oil and oil products increased by 5%, and natural gas consumption grew by 15%. Declining energy intensity in almost all regions has been balanced by increased energy consumption. ( high confidence) {6.3}

Prices have dropped rapidly over the last five years for several key energy system mitigation options, notably solar photovoltaics (PV), wind power, and batteries. From 2015 to 2020, the prices of electricity from PV and wind dropped 56% and 45%, respectively, and battery prices dropped by 64%. Electricity from PV and wind is now cheaper than electricity from fossil sources in many regions, electric vehicles are increasingly competitive with internal combustion engines, and large-scale battery storage on electricity grids is increasingly viable. ( high confidence) {6.3, 6.4}

Global wind and solar PV capacity and generation have increased rapidly. Solar PV grew by 170% (to 680 TWh); wind grew by 70% (to 1420 TWh) from 2015 to 2019. Policy, societal pressure to limit fossil generation, low interest rates, and cost reductions have all driven wind and solar PV deployment. Solar PV and wind together accounted for 21% of total low-carbon electricity generation and 8% of total electricity generation in 2019. Nuclear generation grew 9% between 2015 and 2019 and accounted for 10% of total generation in 2019 (2790 TWh); hydroelectric power grew by 10% and accounted for 16% (4290 TWh) of total generation. In total,low- and zero-carbon electricity generation technologies produced 37% of global electricity in 2019. ( high confidence) {6.3, 6.4}

If investments in coal and other fossil infrastructure continue, energy systems will be locked in to higher emissions, making it harder to limit warming to well below 2°C. Many aspects of the energy system – physical infrastructure; institutions, laws, and regulations; and behaviour – are resistant to change or take many years to change. New investments in coal-fired electricity without CCS are inconsistent with limiting warming to well below 2°C. ( high confidence) {6.3, 6.7}

Limiting warming to well below 2°C will strand fossil-related assets, including fossil infrastructure and unburned fossil fuel resources. The economic impact of stranded assets could amount to trillions of dollars. Coal assets are most vulnerable over the coming decade; oil and gas assets are more vulnerable toward mid-century. CCS can allow fossil fuels to be used longer, reducing potential stranded assets. ( high confidence) {6.7}

A low-carbon energy transition will shift investment patterns and create new economic opportunities. Total energy investment needs will rise, relative to today, over the next decades, if warming is limited to 2°C (>67%) or lower. These increases will be far less pronounced, however, than the reallocations of investment flows that are likely to be seen across sub-sectors, namely from fossil fuels (extraction, conversion, and electricity generation) without CCS and toward renewables, nuclear power, CCS, electricity networks and storage, and end-use energy efficiency. A significant and growing share of investments between now and 2050 will be made in emerging economies, particularly in Asia. ( high confidence) {6.7}

Climate change will affect many future local and national low-carbon energy systems. The impacts, however, are uncertain, particularly at the regional scale. Climate change will alter hydropower production, bioenergy and agricultural yields, thermal power plant efficiencies, and demands for heating and cooling, and it will directly impact power system infrastructure. Climate change will not affect wind and solar resources to the extent that it would compromise their ability to reduce emissions. ( high confidence) {6.5}

Electricity systems powered predominantly by renewables will be increasingly viable over the coming decades, but it will be challenging to supply the entire energy system with renewable energy. Large shares of variable solar PV and wind power can be incorporated in electricity grids through batteries, hydrogen, and other forms of storage; transmission; flexible non-renewable generation; advanced controls; and greater demand-side responses. Because some applications (e.g., air travel) are not currently amenable to electrification, 100% renewable energy systems would likely need to include alternative fuels such as hydrogen or biofuels. Economic, regulatory, social, and operational challenges increase with higher shares of renewable electricity and energy. The ability to overcome these challenges in practice is not fully understood. ( high confidence) {6.6}

Multiple energy supply options are available to reduce emissions over the next decade. Nuclear power and hydropower are already established technologies. Solar PV and wind are now cheaper than fossil-generated electricity in many locations. Bioenergy accounts for about a tenth of global primary energy. Carbon capture is widely used in the oil and gas industry, with early applications in electricity production and biofuels. It will not be possible to widely deploy all of these and other options without efforts to address the geophysical, environmental-ecological, economic, technological, socio-cultural, and institutional factors that can facilitate or hinder their implementation. ( high confidence) {6.4}

Some mitigation options can provide more immediate and cost-effective emissions reductions than others, but a comprehensive approach will be required over the next 10 years to limit warming to well below 2°C. There are substantial, cost-effective opportunities to reduce emissions rapidly in several sectors, including electricity generation and light-duty transportation. But near-term reductions in these sectors will not be sufficient to limit warming to well below 2°C. A broad-based approach across the energy sector will be necessary to reduce emissions over the next 10 years and to set the stage for still deeper reductions beyond 2030. ( high confidence) {6.4, 6.6, 6.7}

Enhanced integration across energy system sectors and across scales will lower costs and facilitate low-carbon energy system transitions. Greater integration between the electricity sector and end use sectors can facilitate integration of variable renewable energy (VRE) options. Energy systems can be integrated across district, regional, national, and international scales. ( high confidence){6.4, 6.6}

The viable speed and scope of a low-carbon energy system transition will depend on how well it can support sustainable development goals (SDGs) and other societal objectives. Energy systems are linked to a range of societal objectives, including energy access, air and water pollution, health, energy security, water security, food security, economic prosperity, international competitiveness, employment. These linkages and their importance vary among regions. Energy sector mitigation and efforts to achieve SDGs generally support one another, though there are important region-specific exceptions. ( high confidence) {6.1, 6.7}

The economic outcomes of low-carbon transitions in some sectors and regions may be on a par with, or superior to those of an emissions-intensive future. Cost reductions in key technologies, particularly in electricity and light-duty transport, have increased the economic attractiveness of near-term low-carbon transitions. Long-term mitigation costs are not well understood and depend on policy design and implementation, and the future costs and availability of technologies. Advances in low-carbon energy resources and carriers such as next-generation biofuels, hydrogen produced from electrolysis, synthetic fuels, and carbon-neutral ammonia would substantially improve the economics of net-zero energy systems. (medium confidence) {6.4, 6.7}

6.1Introduction

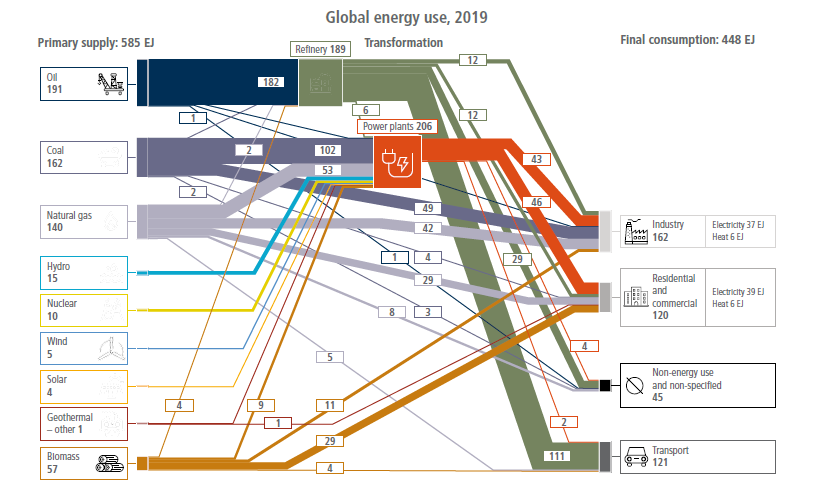

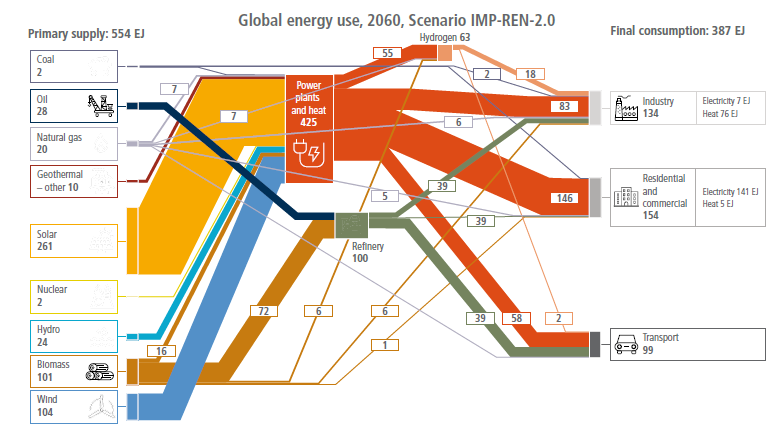

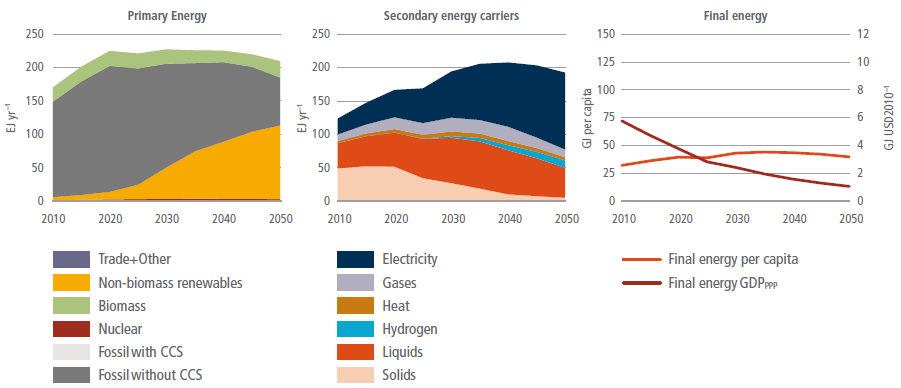

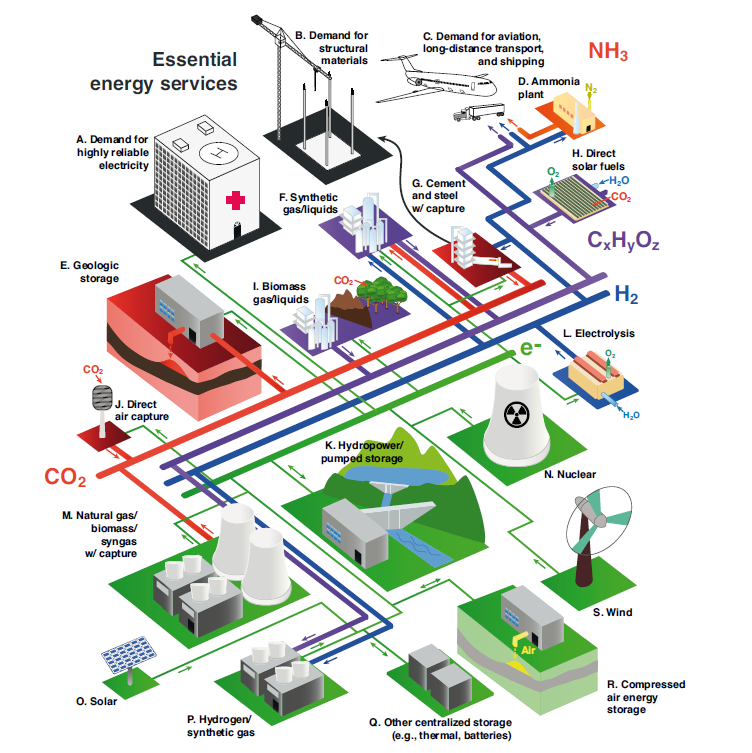

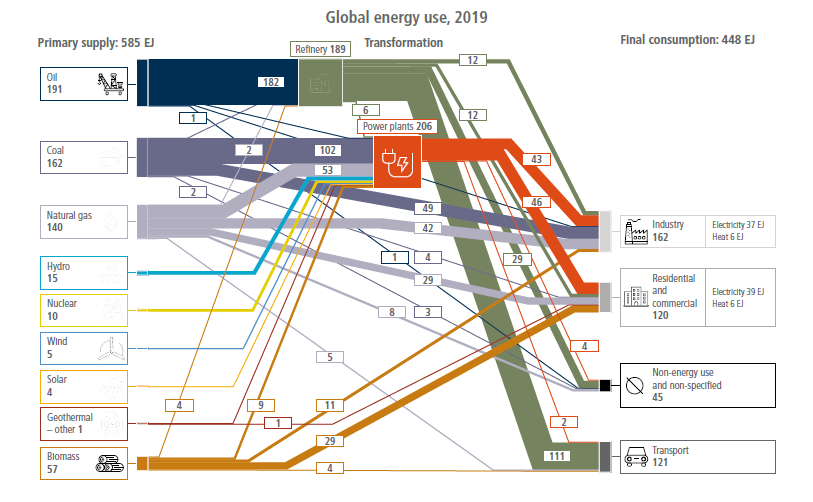

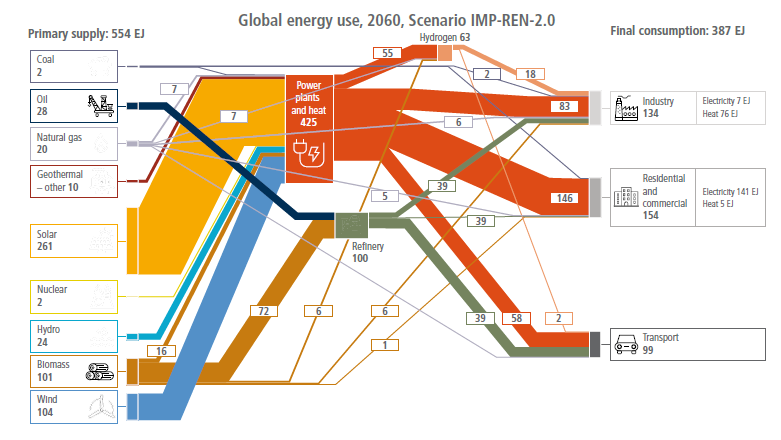

The global energy system is the largest source of CO2 emissions (Chapter 2). Reducing energy sector emissions is therefore essential to limit warming. The energy systems of the future will be very different from those of today if the world successfully limits warming to well below 2°C. Energy will be provided, converted, and used in different ways than it is today (Figure 6.1). Achieving and responding to these changes presents an impressive range of challenges and opportunities.

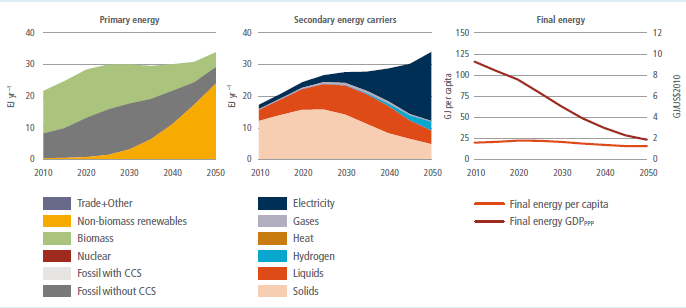

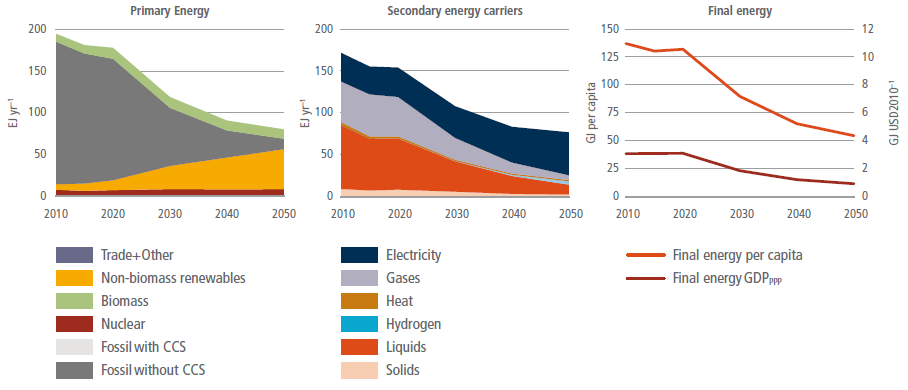

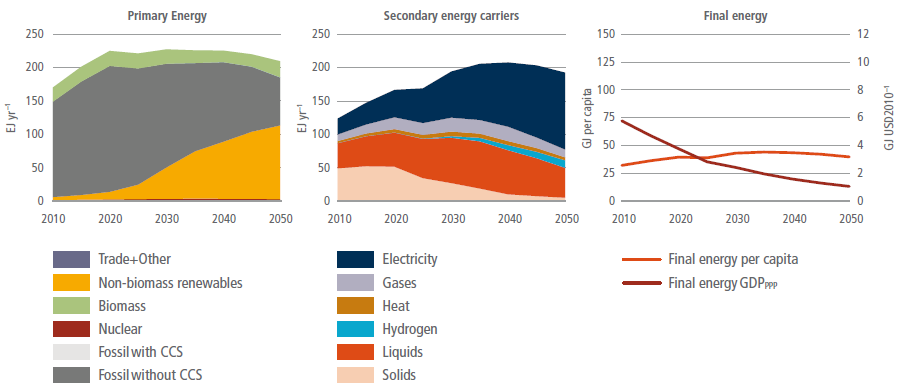

Figure 6.1 | Global energy flows within the 2019 global energy system (top panel) and within two illustrative future, net-zero CO2 emissions global energy systems (bottom panels). Source: IEA, AR6 Scenarios Database. Flows below 1 EJ are not represented. Agricultural energy and energy own use are included in industry. Captured methane is included in natural gas supply where appropriate. The illustrative net-zero scenarios correspond to the years in which net energy system CO2 emissions reach zero – 2060 in IMP-Ren and 2070 in IMP-Neg-2.0. Source: data from IMP-Ren: Luderer et al. (2022); IMP-Neg-2.0: Riahi, K. et al. (2021).

Within this context, this chapter has two main objectives. First, it aims to assess specific, individual mitigation options in energy supply, energy transformation, and energy transportation and transmission. This assessment is complementary to a set of chapters that explore mitigation options in agriculture, forestry, and other land uses (Chapter 7), urban systems and other settlements (Chapter 8), buildings (Chapter 9), transport (Chapter 10), industry (Chapter 11), and cross-sectoral perspectives (Chapter 12). Second, this chapter aims to assess system-level mitigation opportunities and challenges across the entirety of energy systems. These systems include energy supply, transformation, transmission, storage, transportation, and end uses. They also include the societal systems that interact with the physical energy system. As energy systems become increasingly integrated and interconnected, a system-wide perspective is necessary for understanding mitigation opportunities and challenges.

Within this context, this chapter addresses six topics, each of which is addressed in a separate section. First, Section 6.2 defines the scope of the energy system. Section 6.3 then discusses the recent trends in energy systems that might exert the most significant influence on energy system evolution and options for reducing emissions. Section 6.4 assesses the status and potential of individual energy supply, transformation, storage, transportation and transmission, and integration mitigation options in the energy sector. Section 6.5 explores how climate change might affect energy systems and alter potential energy system mitigation options and strategies. Section 6.6 identifies key characteristics of net-zero energy systems – those that emit very little or no CO2. Section 6.7 explores transition pathways toward and through net-zero energy systems. Across all of these sections, the chapter aims to explore the ways that energy sector mitigation options and strategies interact with Sustainable Development Goals (SDGs) and other societal and environmental goals.

6.2The Scope of the Energy System and its Possible Evolution

For this chapter, energy systems are defined broadly to include both physical and societal elements. The physical infrastructure includes all the infrastructure and equipment used to extract, transform, transport, transmit, and convert energy to provide energy services. In addition to the physical system, a broad range of societal systems and dynamics are relevant to the energy system. Human societies use energy to transport themselves and the goods that they use and consume, to heat, cool, and light their homes, to cook their food, and to produce goods and services. Energy systems are therefore tied to the systems involved in the provision of these various goods and services. All energy users engage in the operation of energy systems by demanding energy at particular times and in particular forms. They can adjust their behaviour and demands, for example, by using less energy or by changing when they use energy. Consumers can invest in equipment that reduces their energy needs, and they can invest in technologies that transform energy (e.g., rooftop solar) or store energy (e.g., batteries). Firms and governments invest in equipment to produce, transform, and transport energy such as power plants, refineries, electric transmission lines, and oil tankers. All aspects of energy systems are governed by laws, regulations, and actual institutions that reside within businesses and governments at all levels. This includes, for example, rules for trading emissions permits, deciding when particular electricity generation technologies might come online, water management and related environmental rules that define the availability of hydropower or influence water availability for cooling power plants, regulations for injecting CO2 into underground reservoirs or disposing of nuclear waste, and even company policies regarding work hours or teleworking, which can have important implications for energy demand profiles. Many people are employed in the energy sector, and energy system mitigation will eliminate some jobs while creating others.

This broader view of energy systems is essential for understanding energy system mitigation, as these broader societal and institutional factors can have an important influence on energy system transformations and the potential to rapidly reduce energy CO2 emissions. Energy system mitigation is as much about the challenges of societal change as it is about the challenges of changes in physical infrastructure, technologies, and operations. While this chapter does not attempt to draw a specific boundary around all the different systems that interact with the energy system, it frequently explores these broader system interactions when assessing different mitigation options and strategies.

There is no single spatial scale at which energy systems might be defined and assessed. They can be assessed at the scales of homes, cities, states or provinces, countries, regions, or the entire world. These different scales are frequently both distinct with their own internal dynamics yet al.o connected to one another. This chapter most frequently assesses energy systems from the country and global perspective.

Because the energy system is so complex, it can be hard to define particular parts of it precisely, and there may be competing definitions in the literature. For the purposes of this chapter, ‘energy supply‘ encompasses all primary energy, conversion, and transmission processes with the exception of those that use final energy to provide energy services in the end-use sectors (transport, buildings, industry and agriculture). The ‘energy system‘ includes energy end uses sectors along with energy supply. ‘Low-emissions‘ is used for energy technologies that produce little CO2 or no CO2 or that remove CO2 from the atmosphere. Similarly, ‘low-carbon‘ transitions is used to describe transitions that limit likely to 2°C (>67%) or below. ‘Net-zero‘ energy systems refer to those that produce very little or no CO2 or may even sequester CO2 from the atmosphere.

6.3Recent Energy System Trends and Developments

Global energy sector emissions continue to grow but at a decreasing rate

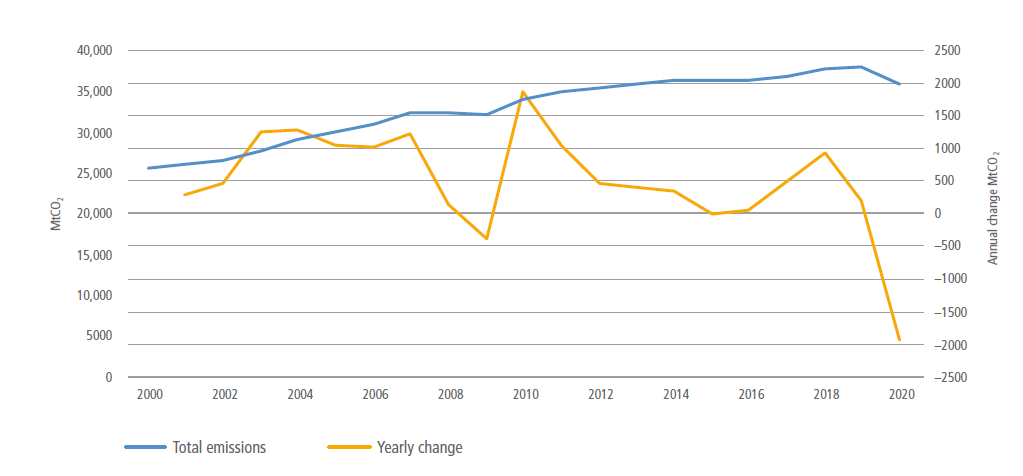

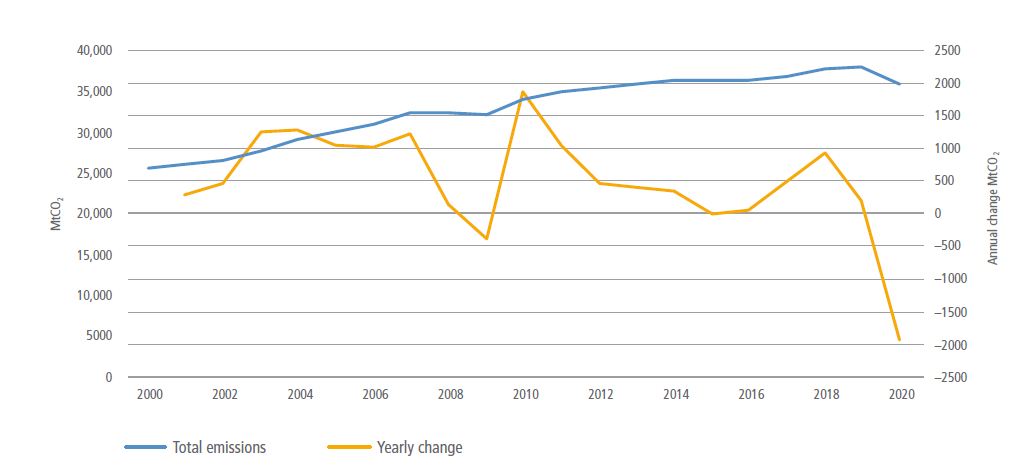

Current energy sector emissions trends, if continued, will not limit global temperature change to well below 2°C ( high confidence). Global energy system fossil fuel CO2 emissions grew by 4.6% between 2015 and 2019 (1.1% yr –1), reaching 38 GtCO2 yr –1 and accounting for approximately two-thirds of annual global anthropogenic GHG emissions. In 2020, with the worldwide COVID-19 pandemic, energy sector CO2 emissions dropped by roughly 2 GtCO2 yr –1 (Figure 6.2). However global energy-related CO2 emissions are projected to rebound by nearly 5% in 2021, approaching the 2018–19 peak (IEA 2021d).

Figure 6.2 | Global energy sectorfossil fuel CO2 emissions and annual change 2000–2019 (MtCO2yr–1). Source: adapted from Minx et al. (2021a); Crippa et al. (2021).

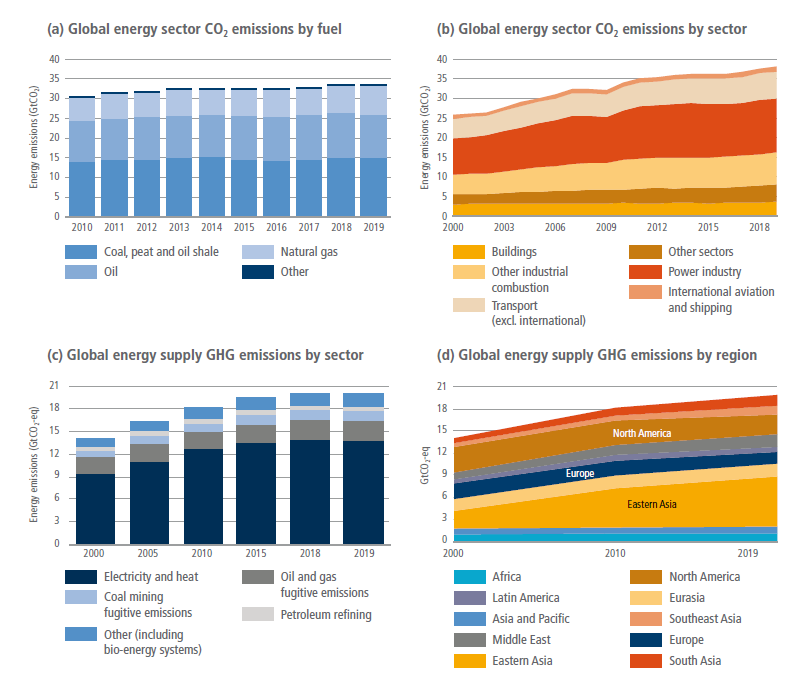

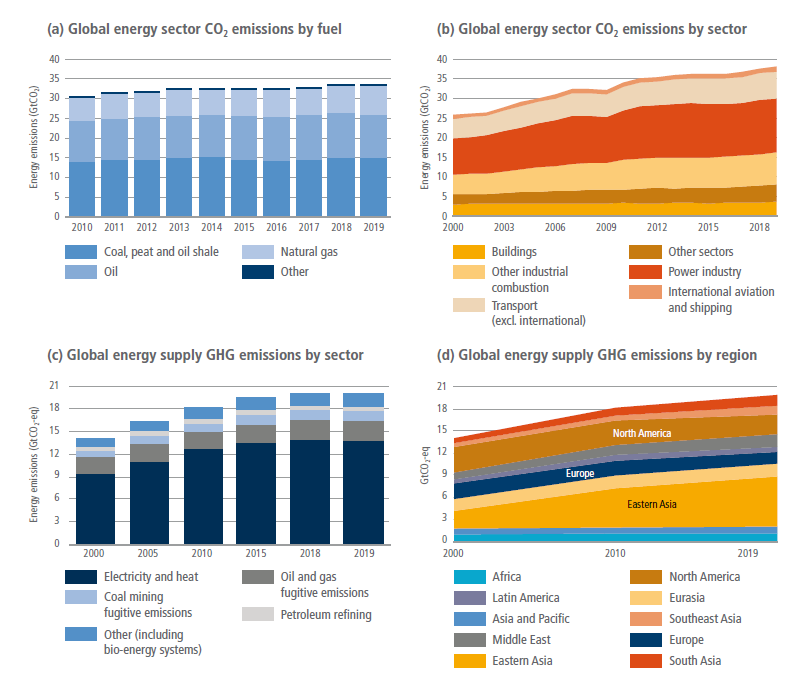

Coal was the single largest contributor to energy sector CO2 emissions between 2015 and 2019, accounting for about 44% of energy sector CO2 emissions in 2019. Oil accounted for about 34% and natural gas accounted for about 22% of energy sector CO2 emissions. Coal, oil and natural gas CO2 emissions grew respectively by 1.2%, 2% and 12.7% (annual rates of 0.31%, 0.5% and 3%) (Figure 6.3). The electricity sector remains the single largest source of energy sector CO2 emissions, accounting for about 36% in 2019, followed by industry at 22% and transport (excluding international shipping and aviation transport) at about 18% (Figure 6.3). Shipping and aviation accounted for a little over 3%. These proportions have remained relatively unchanged over the last decade. Recent trends reinforce the near-term challenges facing energy sector mitigation – electricity sector emissions continue to rise despite rapid deployment of wind and solar power (see below); transportation emissions continue to rise, and petroleum remains the dominant fuel, despite advances in batteries and electric cars (see below). Some specific sectors, such as shipping and aviation, may present longer-term challenges.

Figure 6.3 | Global energy sector CO2 emissions and global energy supply GHG emission. Source: Panel (a): data from IEA (2020a); other panels: data from Crippa et al. (2021).

Energy supply GHG emissions, including CO2 and non-CO2 greenhouse gases, reached 20 GtCO2-eq yr –1 in 2019, rising by 2.7% between 2015 and 2019 (0.66% yr –1). Approximately 18% of energy supply emissions were non-CO2 emissions. Electricity and heat contributed approximately 69% of total energy supply GHG emissions in 2019 (Figure 6.3). This growth has occurred despite the high penetration of solar PV and wind power, particularly in Asia and developed countries.

Fugitive emissions from fossil fuel production, primarily methane, accounted for about 18% of sector supply emissions in 2019, with 2.6 Gt CO2-eq yr –1 linked to oil and gas production and 1.3 GtCO2-eq yr –1 to coal mining (Crippa et al. 2021). Oil and gas operations produced 2.9 GtCO2- eq yr –1 in 2019 (82 Mt yr –1 as methane), split roughly equally between the two (IEA 2020a). There remains a high degree of uncertainty in methane emissions estimates from oil and gas operations despite the emergence of new data from satellites and other measurement campaigns. According to a recent study (Hmiel et al. 2020), methane emissions are underestimated by about 25 to 40%.

Increasing global energy sector GHG emissions have been driven by rising emissions in some large developing and emerging countries; however, per capita emissions in these countries remain well below those in developed countries (Yu et al. 2019). From 2015 to 2019, Eastern Asia, Southern Asia, and South-East Asia energy sector CO2 emissions grew by 2.4% yr –1, 2.6% yr –1, and 5.1% yr –1, respectively. The relative and absolute shares of Europe and North America have continued to decline, partly due to the growth in other countries (Figure 6.3).

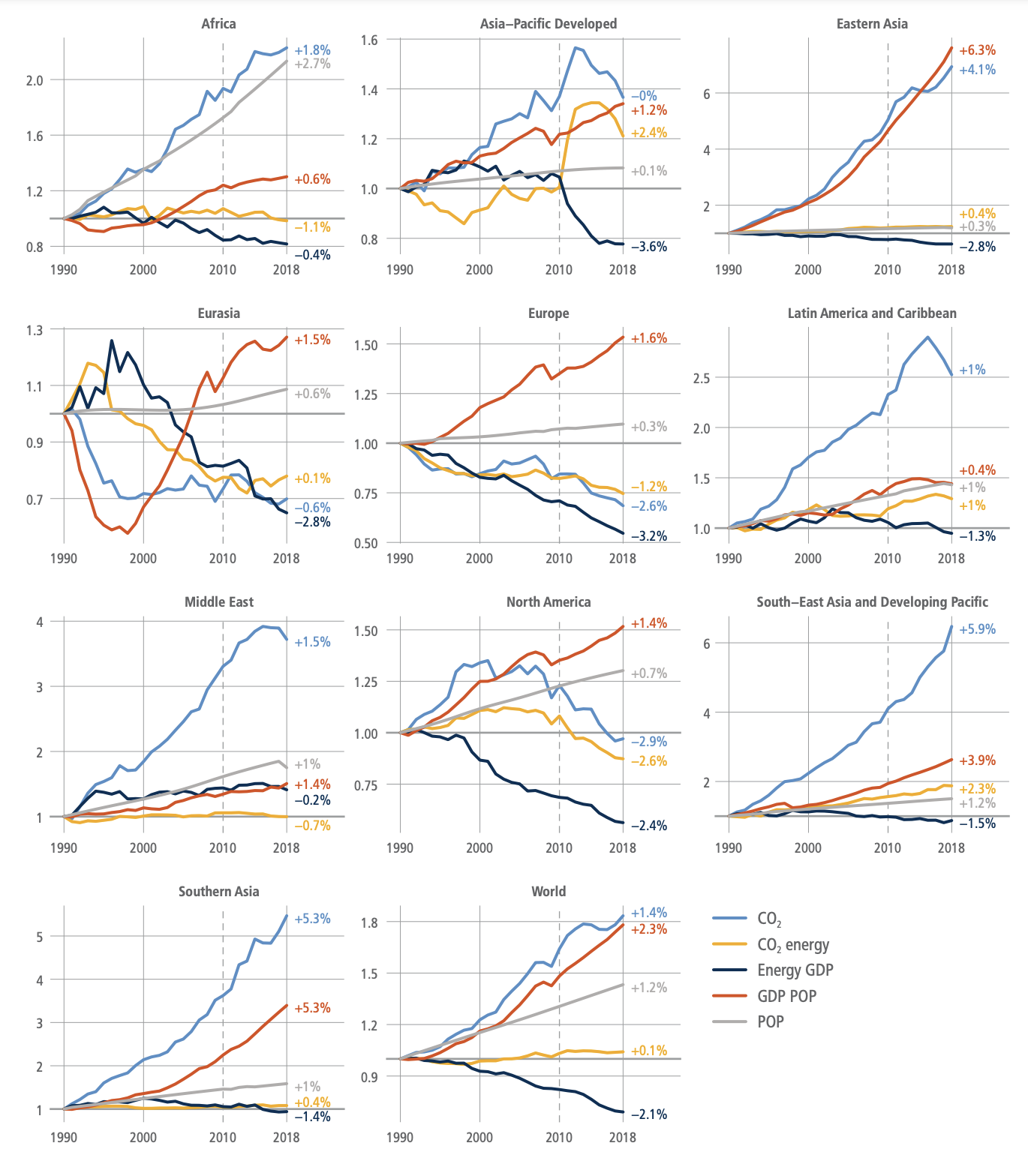

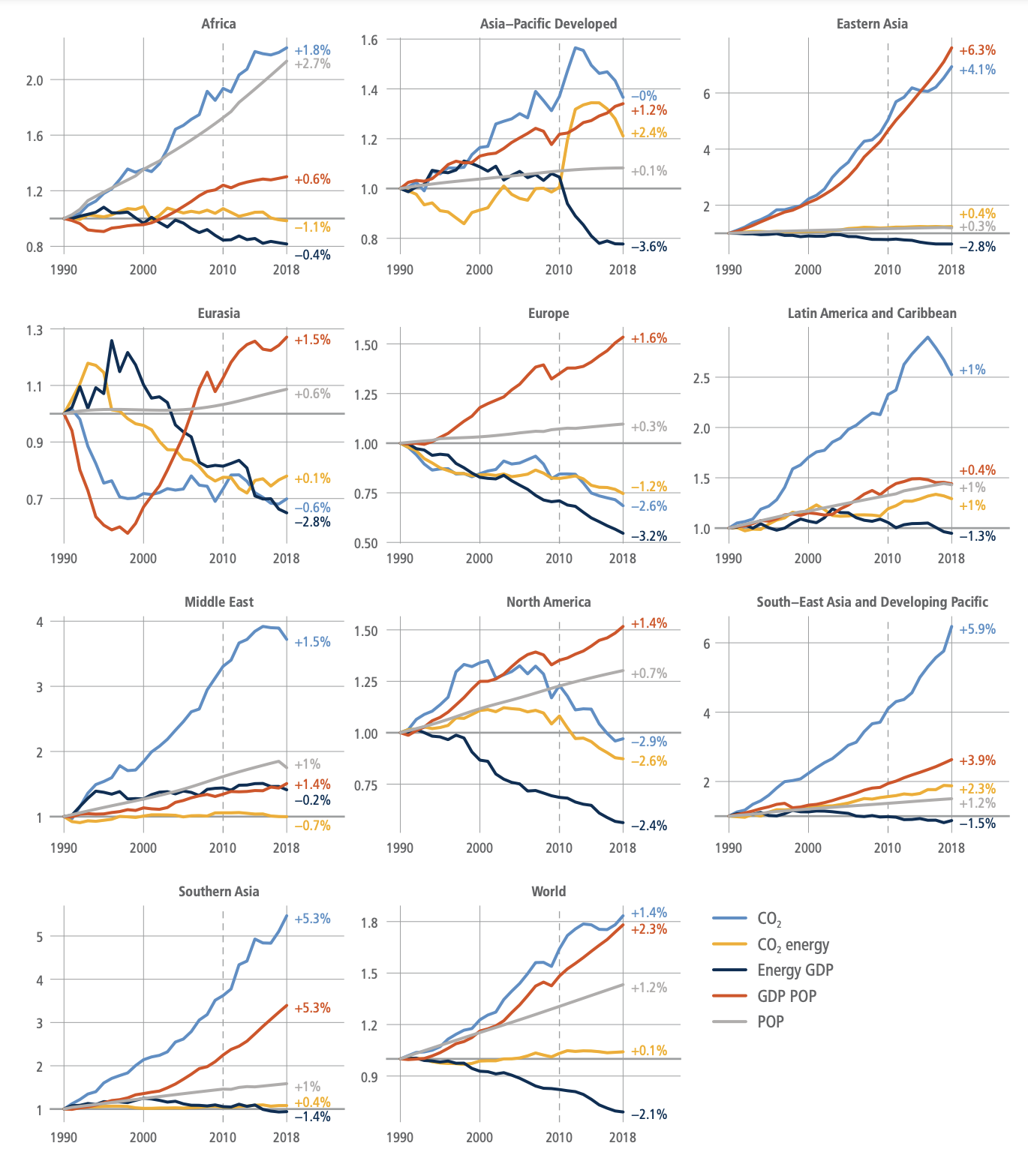

Despite the declining energy intensity, global energy system CO2 emissions have closely tracked GDP per capita (Figure 6.4). This is especially true in the Asian economies, which have experienced rapid GDP per capita growth in the past decades and a massive rise in energy demand. Similarly, emissions have declined in times of economic downturns – for example, in Eurasia in the 1990s and globally in 2009 and 2020. Population growth has also contributed to emissions growth globally and in most regions, particularly Africa, but the effect of population growth has been less than that of economic growth. Since 2015, energy intensity has been declining (IEA 2020b), limiting the impact of economic and population growth. However, there is no region where this factor alone would have been sufficient to decrease CO2 emissions from the energy system. In Europe and North America, the only two regions where emissions decreased meaningfully since 2010, a steady decrease in the carbon intensity of energy was a significant downward driver. The reduction in carbon intensity in the EU is due primarily to the increase of renewable electricity production coupled with the low levels of fossil fuel-based production in the energy mix (Dyrstad et al. 2019).

Figure 6.4 | Drivers of greenhouse gas emissions across selectedregions. Source: Lamb et al. 2021.

Global energy production and demand continue to grow, but at a declining rate

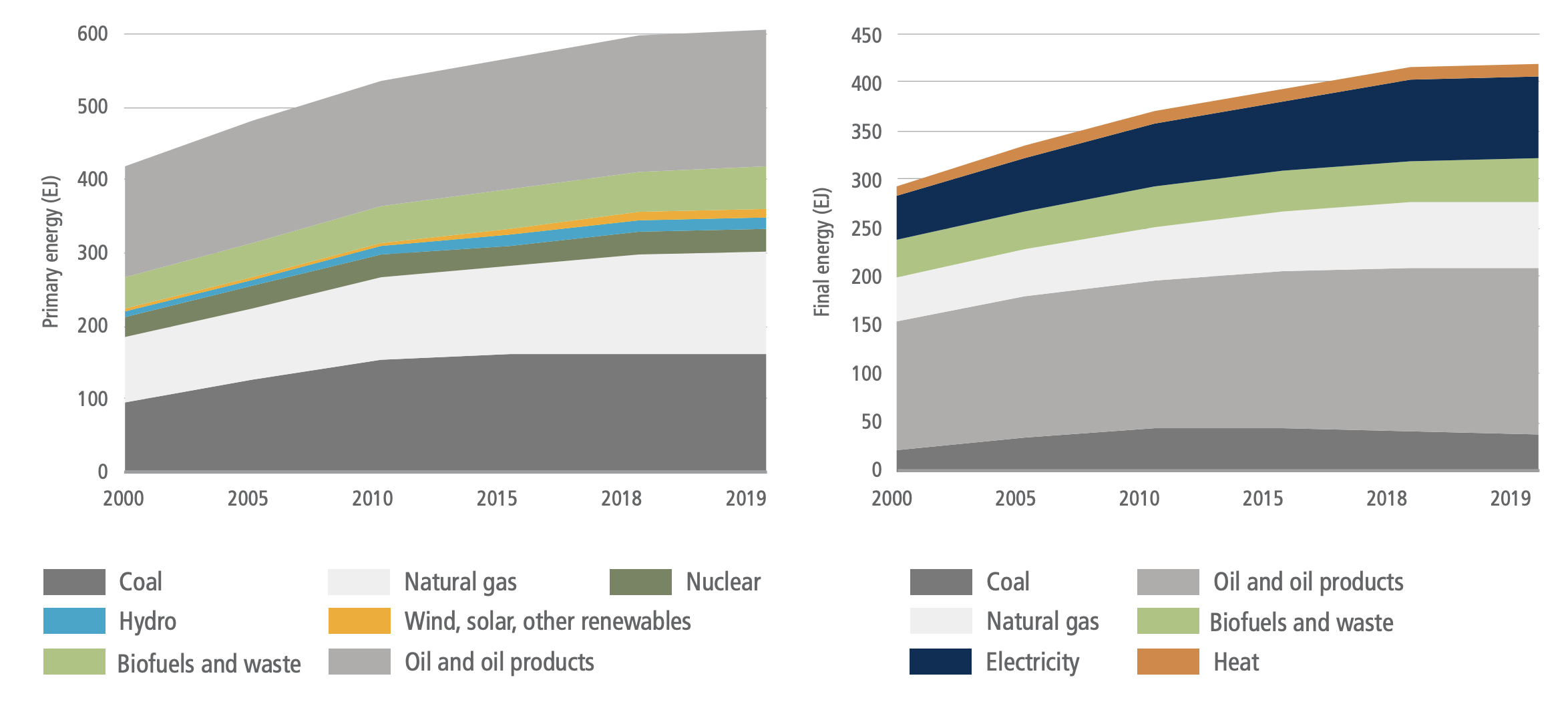

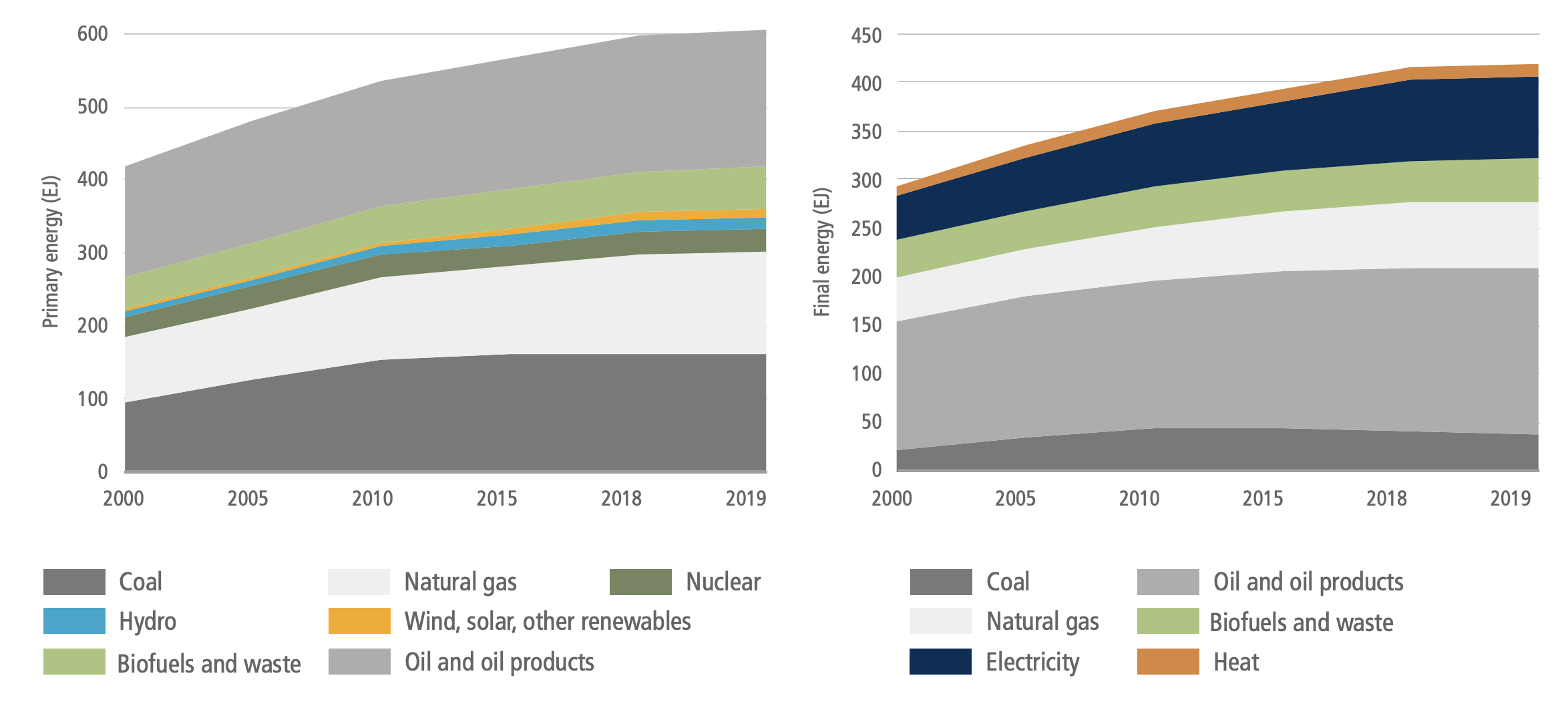

Recent changes in the energy system can be viewed within the context of longer-term trends in energy supply and use. Over the last decade, there has been a significant increase in the total primary energy supply (TPES) and major changes in energy sources. From 2015 to 2019, TPES grew by 6.6% (1.6% yr –1) from 569 EJ yr –1 to 606 EJ yr –1. Natural gas consumption grew most quickly during this period, at 3.5% yr –1. Coal, oil and oil products grew at annual rates of 0.23% yr –1 and 0.83% yr –1, respectively. In 2019, the shares of coal, oil, and natural gas in global TPES were 27%, 31% and 23%, representing only a modest shift from 2015, when the shares were 28%, 32% and 22%, respectively. Renewables, excluding hydropower, grew at an annual rate of 12% yr –1 during this period; however, their share remains marginal in 2019, with just 2.2% of the TPES compared to 1.5% in 2015 (Figure 6.5). Bioenergy (including traditional bioenergy) accounted for 9.4% of the TPES, a similar share compared with 2015.

The totalfinal energy consumption (TFC) grew by 6.6% (1.6% yr –1) from 2015 to 2019, rising from 392 EJ yr –1 to 418 EJ yr –1. This is a slower growth rate than the previous decade (2.8% yr –1) (Figure 6.5). In 2019, oil products used for transportation accounted for 41% of TFC. The penetration of non-fossil fuels is still marginal despite the significant growth of electric vehicles in recent years. Coal still accounted for 9.5% of TFC in 2019, dropping from 11.7% in 2015. Coal is mainly used as a primary energy source in industry and, to a lesser extent, in the residential sector. The share of electricity increased modestly, from 18.6% in 2015 to 20.2% in 2019, reflecting increasing access in developing countries and increasing use of electricity for a wide variety of end uses in the residential sector (Box 6.1). Heat accounts for approximately 3% of TFC, used mainly in industry and the residential sector. Biofuels and waste accounted for 10.4% of TFC in 2019, only modestly changed compared with 2015.

Figure 6.5 | World total primary energy supply (TPES) (EJ) and total final energy consumption (TFC) 2000–2019. Primary energy in this figure is based on IEA accounting methods and not direct equivalents for several energy sources. Final energy does not include industry own use and losses. Source: adapted from IEA world energy balances, Minx et al. (2021b) database for IPCC.

There are important differences in fuel use across countries. While developed countries almost exclusively use modern fuels, many countries still obtain a significant fraction of their energy from traditional bioenergy (fuelwood and charcoal). Traditional bioenergy (fuelwood and charcoal) is particularly important in sub-Saharan countries and some Asian countries such as India, particularly in the residential sector for cooking. Africa is still characterised by a high share of traditional bioenergy in TPES and TFC. In 2019, biomass and waste in Africa accounted for 44% of the TPES. The global average was 9.4%.

Asia has been particularly important in TFC growth since 2015. In 2019, Eastern Asia accounted for more 24% of TFC (1.52% annual growth from 2015). In contrast, TFC has increased by only 0.58% in Europe and 1.24% in North America. Despite an increase of 2.05% over the same period, Africa’s TFC remains relatively low (6.1% of global TFC), particularly in sub-Saharan countries. Approximately 860 million people, mostly in sub-Saharan Africa and some Asian countries, lacked access to electricity and about 2.65 billion to clean-cooking facilities in 2018 (IEA 2019a). Achieving universal energy access (SDG 7) will require energy transitions in the domestic sector, including new developments in off-grid energy technologies, emphasis on rationalising energy subsidies, and increasing efforts to address health concerns related to the use of traditional fuels (Box 6.1).

Non-climate factors continue to drive energy systems changes

While energy system changes are vital to climate mitigation, recent energy system changes have arisen in response to a much broader set of factors. Important factors include economic growth, energy access, energy justice, energy security, air pollution, technological progress in low-emissions technologies, local job creation. Several of these are discussed here.

Energy access. Between 2000 and 2019, the proportion of the population with access to electricity increased from 73% to 90% (IEA 2020c). Although most of those people gaining access to energy have gained access to fossil fuel-based electricity, an increasing number are gaining access to electricity from renewable sources. Low-emissions, decentralised systems are proving a cost-effective way to provide electricity in rural areas (Scott et al. 2016; Muchunku et al. 2018; IEA 2019b), although the use of diesel generators continues in some remote areas. Between 2000 and 2019 the proportion of the population with access to clean cooking (modern fuels and/or improved biomass cookstoves) rose from 52% to 66%.

Energy security. The ability of countries to maintain access to reliable and affordable energy resources continues to shape energy policy. Energy security is perceived as a national security issue and often prioritised over climate concerns (Nyman 2018). The linkage between climate and energy security is now widely recognised (Blarke and Lund 2007; Toke and Vezirgiannidou 2013; La Viña et al. 2018; World Energy Council 2020; Fu et al. 2021; United Nations 2021). Approaches to energy security are frequently driven by the scope of domestic energy resources. For example, energy security concerns have led to continued reliance on domestic coal production and consumption (Jakob et al. 2020) and increased investment in domestic renewable generation (Konstantinos and Ioannidis 2017). Liquefied natural gas (LNG) Importers have diversified their sources as reliance on LNG has increased (Vivoda 2019).

Air pollution. The energy system is an important source of air pollution, including both indoor and outdoor air pollution. Efforts to address air pollution in several countries and regions (the USA, Mexico, China, India, European Union, Africa, Southeast Asia, among others) have had an importance influence on energy system changes (Bollen and Brink 2014; Fang et al. 2019). Policies aimed at controlling nitrogen oxides (NOx) and sulphur dioxide (SO2) emissions have driven emissions abatement efforts and coal fleet retirements (Singh and Rao 2015; Drake and York, 2021). In some places, the prospect of reducing local air pollution remains more salient to policymakers and the public than climate mitigation when deciding to tighten regulations on coal use (Brauers and Oei 2020).

Technology and costs. Costs for renewable technologies have fallen significantly in recent years, driving significant changes in electricity production and transportation (see below). These advances are not divorced from climate and other environmental concerns (Kuik, Branger and Quirion 2019; Timilsina and Shah 2020). Recent advances in PV cells, for example, can be traced in part to aggressive deployment policies spurred by energy security, climate, and other environmental concerns (Kreuz and Müsgens 2017) (Sections 6.3.5 and 6.4.2). The falling costs of batteries, manly Li-ion batteries, has boosted the competitiveness of electric vehicles (Nykvist et al. 2015) (Section 6.3.7).

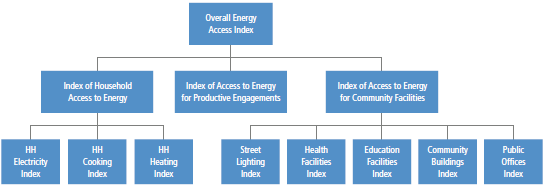

Box 6.1 | Energy Access, Energy Systems, and Sustainability

Successful mitigation must work in tandem with fundamental development goals such as access to modern forms of energy. In many developing countries, access to electricity, clean cooking fuels, and modern and efficient energy remain an essential societal priority. This is particularly true in sub-Saharan Africa and several Asian countries. SDG 7 on universal access to modern energy includes targets on modern energy services, renewable energy, and energy efficiency, which implies a profound transformation of the current energy systems. Although there are different definitions of energy access, the ultimate goal is universal access to clean and modern fuels.

Despite progress in some countries such as India, Bangladesh and Kenya, 860 million people were without access to electricity in 2018, compared with 1.2 billion in 2010. About 2.65 billion households were cooking with solid fuels, distributed across Asia and Africa (IEA et al. 2020). Around 850 million people in sub-Saharan Africa relied on traditional biomass (firewood and charcoal) for cooking, and 60 million relied on kerosene and coal to meet their energy needs (IEA 2018a). Air pollution was likely responsible for 1.1 million deaths across Africa in 2019 (Fisher et al. 2021). It has been estimated that 2.2 billion people will still be dependent on inefficient and polluting energy sources for cooking by 2030, mainly in Asia and Sub-Saharan Africa, and 650 million people are likely to remain without access to electricity in 2030, 90% of whom will reside in Sub-Saharan Africa (IEA et al. 2020).

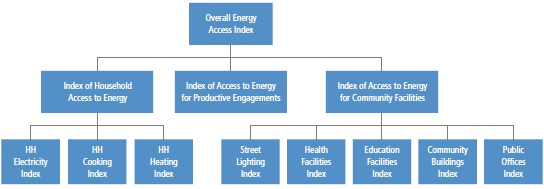

Box 6.1, Figure 1 | Measuring access to energy. Source: with permission from ESMAP-World Bank 2015.

Research indicates that decentralised and on-grid renewables are likely the least cost options to provide universal access to electricity by 2030 (Section 6.4.2). Natural gas, LPG, and improved biomass cookstoves are the most important options for cooking. Universal access to electricity and clean cooking requires a rapid shift from traditional biomass to cleaner fuels and/or clean cooking technologies (IEA et al. 2020). It has been estimated that the provision of electricity and clean cooking for all would require USD786 billion in cumulative investment to 2030, equal to 3.4% of total energy sector investment over the period (IEA 2017).

Even without universal access to modern energy, increased access will substantially affect energy systems, particularly electricity systems through the deployment of renewable energy, LPG, and biomass supply chains. Universal access for households, however, will have a minimal impact on global energy demand; it has been estimated that universal access for household will increase energy demand by 0.2% in 2030 (37 Mtoe yr –1) relative to a future without any change in access to modern energy (IEA 2017).

There have been initial efforts to phase out coal but only modest declines in use

Global coal consumption has been declining, with small fluctuations, since it peaked in 2013 (IEA 2020d). Coal is faring differently across regions. Coal use has been decreasing in the OECD regions, particularly in the USA and the European Union (EU), while remaining mostly flat in China after a period of growth, and it is continuing to increase in other major developing Asian economies (IEA 2020d). Trends in the electricity sector, where most coal is being consumed, are similar. Growth in coal-fired electricity generation capacity in the Asia Pacific region has offset retirements in North America and Europe (Jakob et al. 2020; Global Energy Monitor et al., 2021).

Reductions in coal consumption have been driven in large part by non-climate factors, most notably environmental regulations to address air pollution, rapidly declining costs of renewables, and lower natural gas prices, especially inexpensive unconventional gas in the USA. (Culver and Hong 2016; Diluiso et al.2021; Vinichenko et al. 2021). Older coal-fired power plants that cannot meet new environmental regulations, or have become unprofitable or uncompetitive, have been closed in many regions. Moreover, coal power expansion has slowed down in Asia, as countries have suspended and cancelled new projects for reasons such as overcapacity, environmental constraints, and the development of renewables (Box 6.2).

Different regions have replaced retired coal with different energy sources. Old coal fleets have been replaced approximately half by gas and half by renewables in the USA, mainly by renewables in the EU, and by advanced coal plants and renewables in Asia (EMBER 2020). Replacing old coal with new coal facilities is inconsistent with limiting warming to 2°C or below ( high confidence) (Pfeiffer et al. 2016, 2018; Smith et al. 2019; Tong et al. 2019) (Section 6.7.4).

Major coal-consuming countries with abundant coal reserves remain far from phasing out coal (Edenhofer et al. 2018; Spencer et al. 2018). In most developing countries with large coal reserves, coal use has been increasing to support energy security and because it is perceived to have lower costs than alternatives (Steckel et al. 2015; Kalkuhl et al.2019). However, coal faces increasing business risks from the decreasing costs of alternative, low-emissions energy sources and increasing focus on air pollution and other environmental impacts from coal mining and use (Garg et al. 2017; Sovacool et al. 2021). Continued coal builds, mostly in developing countries, will increase the risks of stranded assets (Farfan Orozco 2017; Cui et al. 2019; Saygin et al. 2019) (Box 6.13).

Economic, social, and employment impacts of accelerated coal phase-outs tend to be significant in coal-dependent regions. Tailored reemployment has been used to support coal transitions in some regions. Although some estimates show higher employment opportunities from low-carbon energy (Garrett-Peltier 2017), results vary across regions. Moreover, even with a net increase in total employment, in the long run, renewable jobs are often located outside of coal regions and require different skill sets from the coal industry (Spencer et al. 2018). In a broader sense, achieving a ‘just transition’ also requires managing the impacts on regional economic development for coal-dependent communities and the effects of higher energy prices for consumers and energy-intensive industries through a comprehensive policy package (Green and Gambhir 2020; Jakob et al. 2020) (Box 6.2).

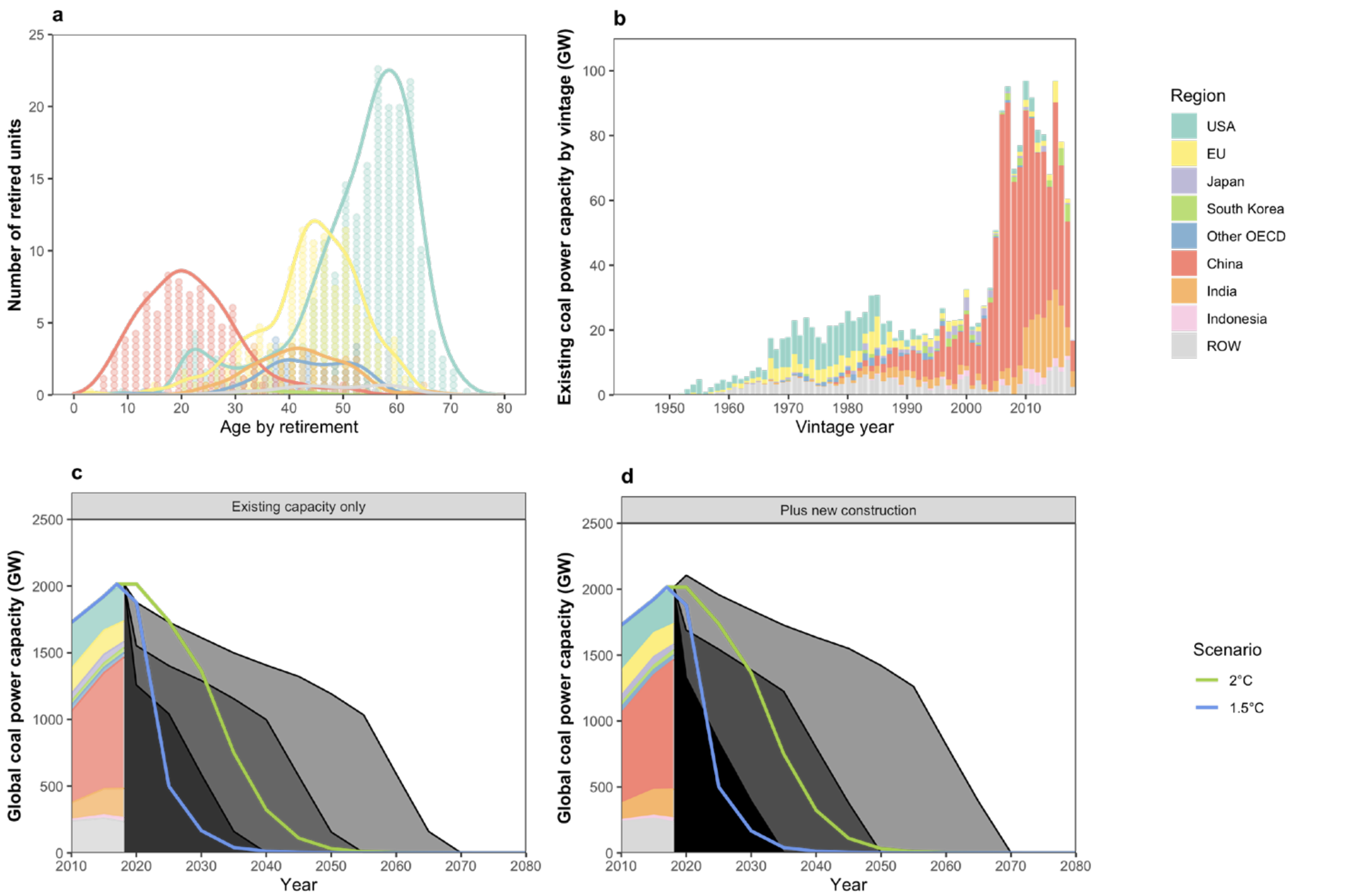

Box 6.2 | Status and Challenges of a Coal Phase-out

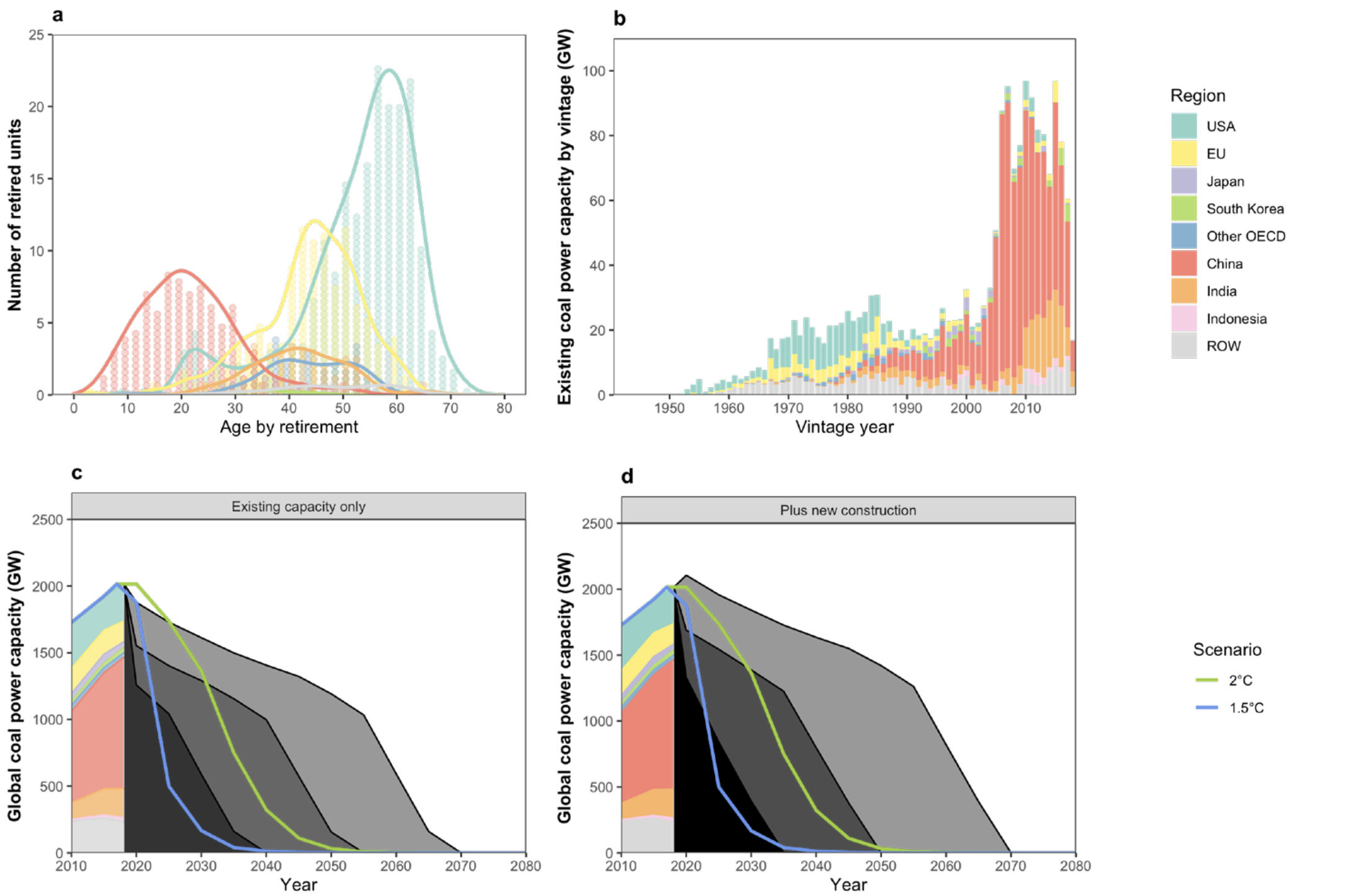

Limiting global warming to 2°C or below requires a rapid shift away from unabated coal consumption – coal without CCS – in the energy system by 2050 (IPCC 2018 a; Section 6.7; Chapter 3). This will require cancellation of new coal power projects and accelerated retirement of existing coal plants (Edenhofer et al. 2018; Kriegler et al. 2018; Pfeiffer et al. 2018; Smith et al. 2019; Tong et al. 2019). To limit warming to 2°C or lower, and without new builds, existing coal plants will need to retire 10 to 25 years earlier than the historical average operating lifetime. Completing all planned projects will further reduce the viable lifetime of all plants by 5 to 10 years if warming is to be limited to 2°C or lower (Cui et al. 2019). Phasing-out coal in the next few decades will present economic, social, and security challenges. These will vary across regions based on the characteristics of existing coal infrastructure, the availability of alternatives, economic development, and technological and institutional lock-in (Jakob et al. 2020).

Box 6.2, Figure1 | Retirement of coal-fired power plants to limit warming to 1. 5°C and 2°C or lower. (a) Historical facility age at retirement, (b) the vintage year of existing units, (c) global coal capacity under different plant lifetimes, compared to capacity levels consistent with a well-below 2°C (green) and 1.5°C (blue) pathway assuming no new coal plants, and (d) and assuming plants currently under construction come online as scheduled, but those in planning or permitting stages are not built. Source: with permission from Cui et al. (2019).

Between 2015 and 2019, global coal power capacity grew by 146 GW, or 7.6%, as new builds offset retirements in some countries (Global Energy Monitor et al. 2021). Meanwhile, an increasing number of countries and regions have committed to or operationalised coal phase-outs (Jewell et al. 2019; Watts et al. 2019; Littlecott et al. 2021). Actions are being taken by various international and sub-national actors, including national and sub-national governments, public and private power companies, and financial institutions and pension funds that have committed not to fund new coal or coal-based infrastructure (yan Nie et al. 2016; Buckley 2019; Auger et al. 2021). Although these initial efforts are not yet sufficient in limiting warming to 1.5°C, and most have occurred in regions with older coal fleets, these examples provide insight into possible coal phase-out strategies (Spencer et al. 2018) and help identify the mechanisms driving the move away from coal, such as market, technology, policy, or other societal objectives. They also enable better understanding of the possible character of oil and gas phase-downs that would ultimately be needed to limit warming two well below 2°C (Section 6.7.4) (Raimi et al. 2019).

Europe. Several European countries are part of the Powering Past Coal Alliance (PPCA) and have committed to phase out unabated coal on or before 2030 (Jewell et al. 2019). Because these countries represent a small share of global coal generation capacity and have mostly ageing coal plants, they tend to face fewer changes in phasing out coal. The effectiveness of PPCA in countries with younger coal fleets has thus been questioned (Jewell et al. 2019; Blondeel et al. 2020). Germany recently joined the PPCA and has committed to phase out unabated coal by 2038. As part of its commitment to phase out coal, Germany is implementing a set of measures that include compensation for power plant closures, labour market measures for coal workers, and substantial support of structural change in coal-mining regions. Poland, another coal-heavy country in Europe, has not indicated a coal phase-out target and faces substantial challenges (Whitley et al. 2017; Antosiewicz et al. 2020). European efforts to phase out coal indicate that appropriate financial instruments are needed (Rentier et al. 2019), and a just transition for workers are important to gain broad public support and help those most affected by the phase-out (Johnstone and Hielscher 2017; Osička et al. 2020).

North America. Coal use has been declining in North America. In the USA, the primary driver has been the availability of cheap shale gas and ageing coal fleets. Coal use in the USA has dropped by over 50% since 2008 (EIA 2019). The recently announced Nationally Determined Contribution (NDC) by the Biden Administration sets a 100% carbon-free electricity goal by 2035 (The White House 2021), indicating a phase-out not only of unabated coal electricity generation, but also of natural gas generation. As one of the two founding countries of the PPCA, Canada has committed to phasing out unabated coal power by 2030 (Government of Canada 2018). Declining coal use in both the USA and Canada has decreased GHG emissions, local air pollutants, and cooling water use (Harris et al. 2015; Kondash et al. 2019). However, there have been concerns about social and economic consequences, particularly at the local level. For instance, the USA has lost about 50,000 coal mining jobs between 2011 and 2021 (US Bureau of Labor Statistics, 2021), with significant regional and economic inequities (Bodenhamer 2016; Abraham 2017; Greenberg 2018). Comprehensive social programmes, such as retirement compensation, training for reemployment, and business support for economic diversification, have been suggested as means to support a just transition (Homagain et al. 2015; Patrizio et al. 2018; Grubert 2020).

Asia. After a period of rapid growth, coal expansion has slowed in Asia, but it still the primary driver of the global increase in coal demand (IEA 2020e). China’s coal consumption reached a plateau under policy efforts during the 13th Five-Year Plan (2016–2020), and new coal plants are being built at a slower rate than previously. Both China and India have suspended and cancelled many new coal power projects and retired a small set of old, dirty, inefficient coal plants (CEA 2019; Global Energy Monitor et al. 2021). These efforts are largely due to non-climate reasons, such air pollution and health (Singh and Rao 2015; Gass et al. 2016; Peng et al. 2018; Malik et al. 2020), overcapacity (Blondeel and Van de Graaf 2018), and rural electrification and renewable investments (Aklin et al. 2017; Thapar et al. 2018). However, as new builds offset retirements, coal generation capacity has continued to grow in both countries since 2015 (Global Energy Monitor et al. 2021). Other fast-growing Southeast Asian countries, such as Indonesia, Vietnam, and the Philippines have experienced strong growth in coal use (IEA 2020b), but an increasing number of new coal power projects are being cancelled (Littlecott et al. 2021). Coal projects in these countries are decreasingly likely to proceed because they rely on international financing, and China, Japan, USA, and other G7 countries have pledged to end overseas coal financing (Schiermeier 2021).

Africa. New coal power projects in Africa have been declining since 2016, with only South Africa and Zimbabwe currently building new coal plants and several others with planned projects (Littlecott et al. 2021). However, these projects also largely depend on international financing and are thus less likely to be implemented (see above). In South Africa, employment in the coal mining sector has dropped by almost half since the 1980s and has been estimated to fall from 77,000 today to 22,000 to 42,000 by 2050 (Cock 2019; Strambo et al. 2019). Policy and financial support are essential to ensure a sustainable transition for these workers (Swilling et al. 2016).

Solar and wind energy have grown dramatically, but global shares remain low relative to other sources

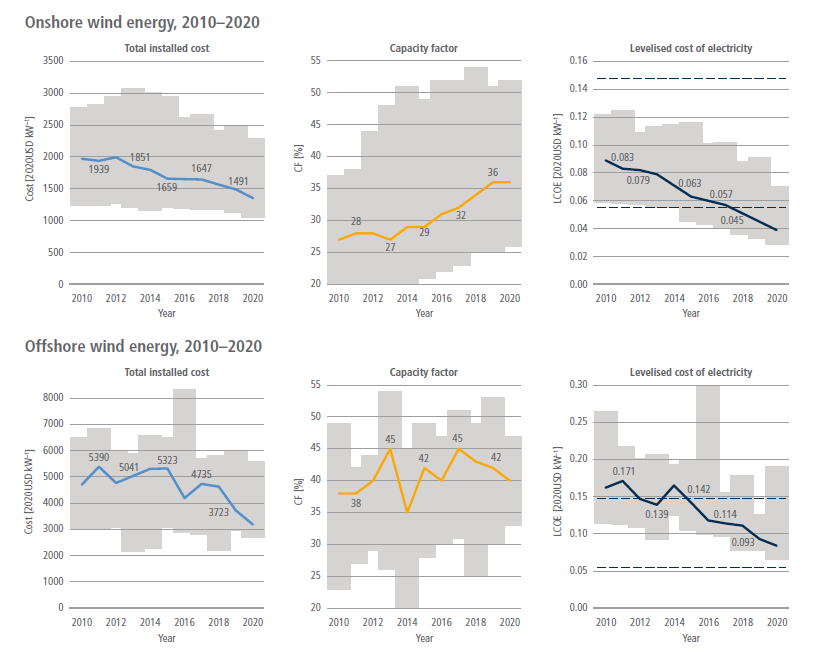

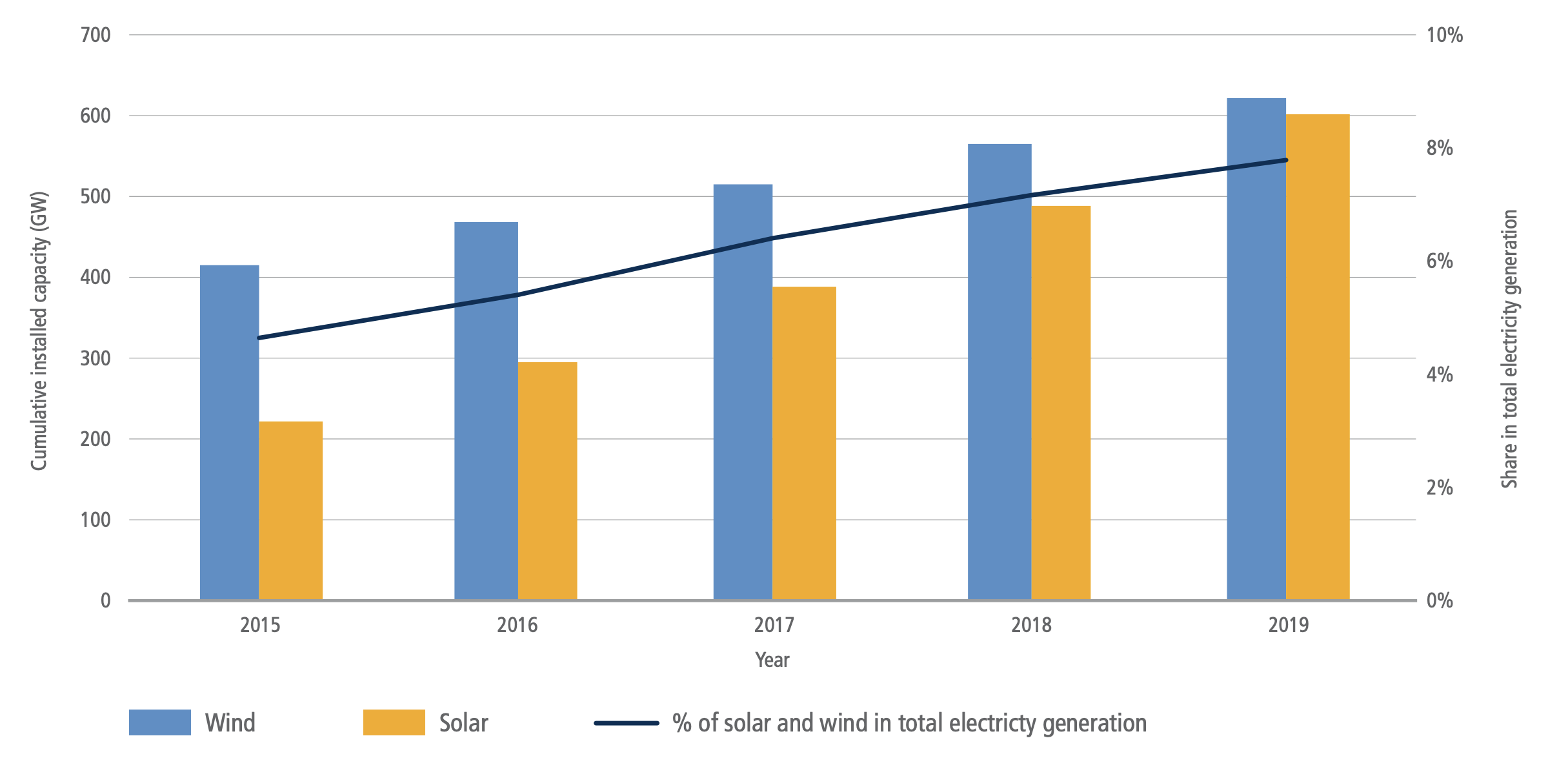

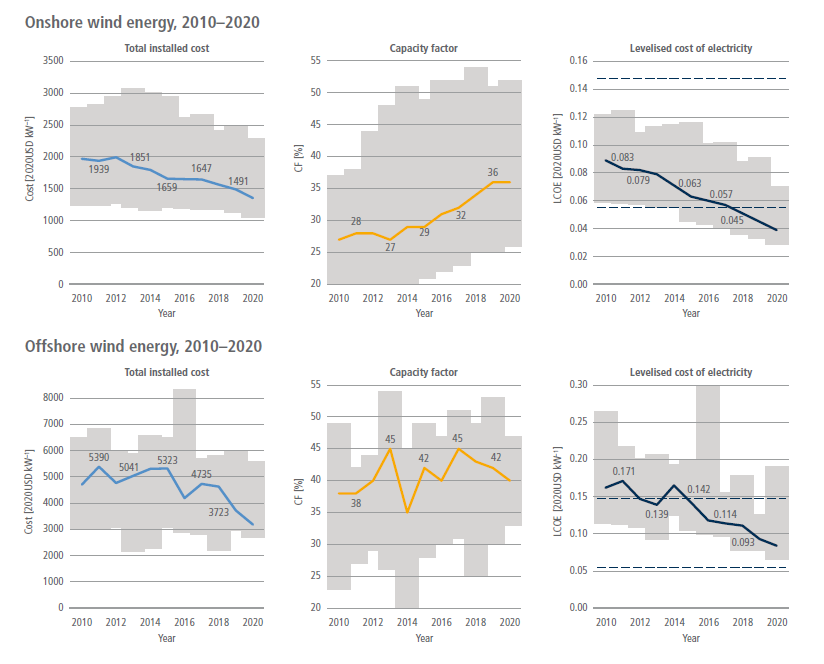

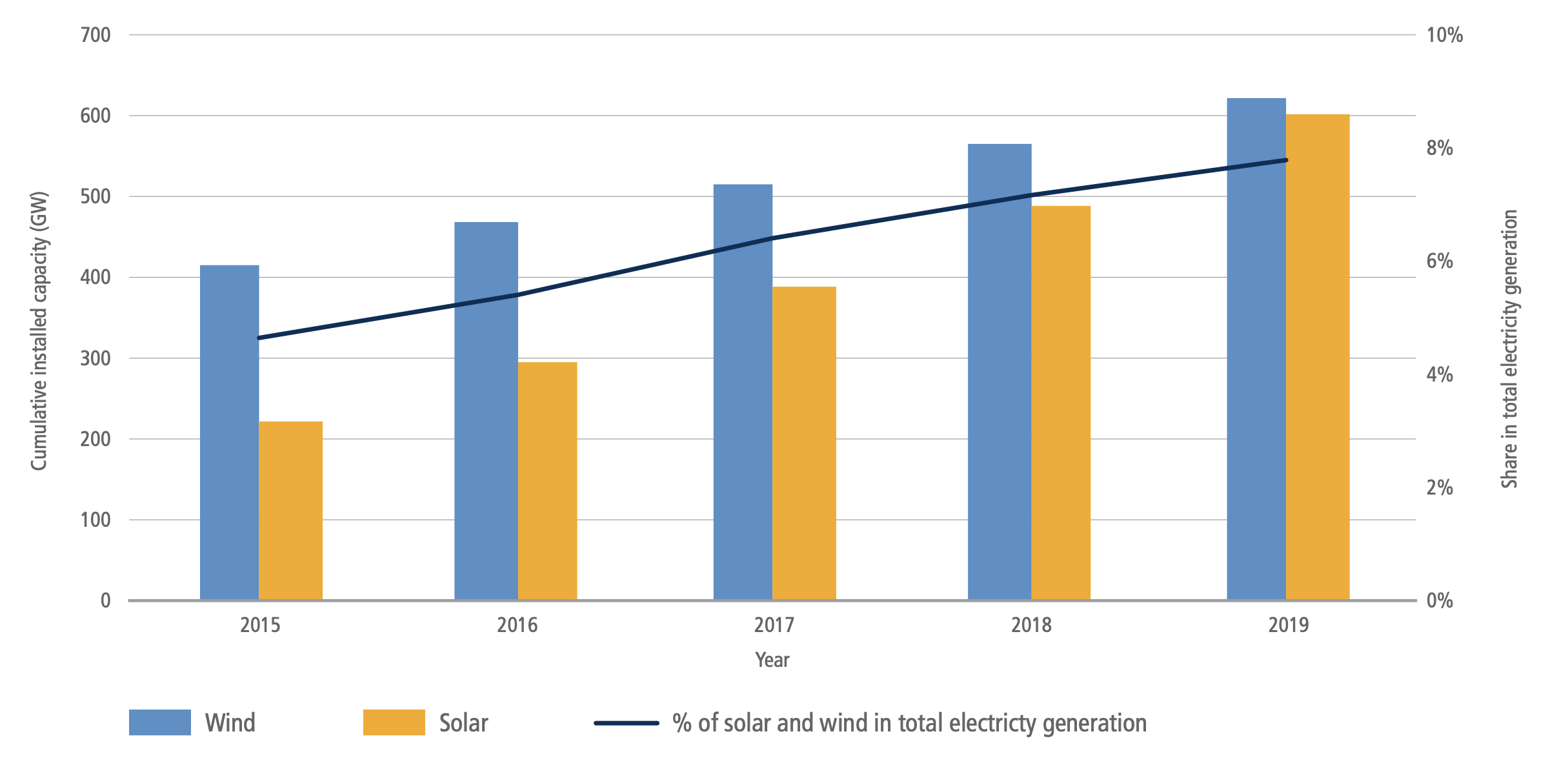

Global PV and wind electric capacities grew 170% and 70%, respectively, between 2015 and 2019. Total solar and wind capacities in 2019 were 609 GW and 623 GW (Figure 6.6) and generation was 680 TWh yr –1 and 1420 TWh yr –1. The combined share of solar and wind in the total global electricity generation in 2019 was around 8% (5.5% wind, 2.5% solar), up from around 5% in 2015 (IEA 2021a). Since 2015, the cost of solar PVs has declined by over 60%. Offshore wind costs have fallen by 32%, and onshore wind costs have fallen by 23% (Section 6.4). PV was around 99% of total solar capacity in 2019; onshore wind was about 95% of total wind capacity. Concentrating solar power (CSP) deployment has also continued to grow, but it remains far below PV. Prior to 2010, 50% of all wind capacity was in Europe, but since then, capacity growth in Asia (led by China), has surpassed the growth in Europe. As a consequence, Europe’s share in global solar capacity has declined from 74% in 2010 to 24% in 2019. Asia’s share in wind and solar capacity in 2019 was 41% and 56%, followed by Europe (31% and 24%) and North America (20% and 12%) (IRENA 2020a, 2021a).

Figure 6.6 | Global solar and wind electricity installed capacities (GW) from 2015–2019 and their combined share in total electricity generation. Source: data from IEA (2021a) and IRENA (2021).

Although the shares of wind and solar remain low in the global total electricity generation, recent growth rates signal the potential for these technologies to support substantial mitigation. The prospects for a continuation of recent growth rates will depend on meeting key challenges such as rapidly integrating wind and solar into electricity grids (Section 6.6.2, Box 6.8) and retiring fossil power plants (see above).

Low-carbon energysources beyond wind and solar have continued to grow

Low-carbon energysources such as nuclear, hydropower, bioenergy, geothermal, marine, and fossil or bioenergy with carbon capture, use and storage (CCUS) have continued to grow since 2015 (IEA 2017, 2021a). Hydroelectric power grew from 3890 TWh yr –1 (14.0 EJ yr –1) in 2015 to 4290 TWh yr –1 (15.5 EJ yr –1) in 2019, or 10.3%; nuclear power grew from 2570 TWh yr –1 (9.3 EJ yr –1) to 2790 TWh yr –1 (10.1 EJ yr –1), or 8.6%. Hydroelectric and nuclear shares in global total electricity generation remained around 16% and 10%, respectively (IEA 2017, 2021a). Global biofuels production grew from 3.2 EJ yr –1 to 4.0 EJ yr –1 from 2015 to 2019 (IEA 2017, 2021a). Bioenergy accounted for 2.4% of electricity generation in 2019. Geothermal energy sources produced 92 TWh yr –1 (0.33 EJ yr –1) of electricity in 2019, up from 80 TWh yr –1 (0.28 EJ yr –1) in 2015 (IEA 2017, 2021a). At present, there are 28 commercially operating CCUS facilities with a CO2 removal capacity of around 40 million tonnes yr –1 (Mtpa). Only two of these are associated with electricity production: the majority are in industrial applications – 37 commercial projects, accounting for about 75 Mtpa, are in various stages of development and construction (Global CCS Institute 2020). The share of marine energy in global electricity generation has remained at approximately 1 TWh yr –1 since 2015. In total, low- and zero-carbon electricity generation technologies produced 37% of global electricity in 2019.

Battery prices have dropped substantially, spurring deployment in electricity and transportation

Recent years have seen a rapid decline in the cost of energy storage, particularly batteries (Section 6.4.4). The price of lithium-ion batteries (LIBs) has declined by 97% in the past three decades, and by 90% in the past decade alone (IEA 2021a; Ziegler and Trancik 2021). These declines have important implications for the energy systems, most notably in supporting increased deployment of variable renewable energy (VRE) generation and electrification of the vehicle fleet.

Battery electricity storage has emerged as important for supporting the flexibility of electricity systems as they accommodate rising shares of VRE. Although pumped-storage hydropower systems accounted for 160 GW, or over 90%, of total energy storage capacity in 2019 (IEA 2020c), battery energy storage systems, led by LIB technology, have accounted for over 90% of new capacity addition since 2015 (IRENA 2019a). In 2019, 10 GW of batteries were connected at the grid and consumer level, rising from 0.6 GW in 2015 (IEA WEO 2019; IEA 2020c).

In California in the USA, legislation was passed to procure around 1.3 GW energy storage (excluding pumped storage) by 2020. One of the largest utility-scale battery storage facilities (300 MW) recently went online in California (Vistra Corp. 2021). Other major projects are in Florida in the USA (409 MW), London in the UK (320 MW), Lithuania (200 MW), Australia (150 MW), Chile (112 MW) and Germany (90 MW), (IRENA 2019a; ARENA 2020; Katz 2020).

The drop in battery prices has also had important implications in the transportation sector. Automotive LIB production rose from around 40 GWh in 2015 to 160 GWh in 2020 (32%). The stock of battery electric vehicles (BEVs) grew from around 0.7 million in 2015 to 4.8 million in 2019 (IEA 2020d). The number of publicly accessible vehicle chargers reached 1.3 million in 2020, 30% of which were fast chargers. The average battery size of BEVs reached 67 kWh in 2019 due to consumer preferences and government incentives for long-range vehicles (Agency 2020; IEA 2021b).

The energy policy landscape continues to evolve

The current energy sector policy landscape consists of policy mixes or policy packages, including regulatory, market-based and other approaches. These mixes have evolved over time and include many sectoral but also some economy-wide policy instruments, such as carbon pricing subsidies.

Governments have chosen a mix of policies and institutional mechanisms that consists of regulatory instruments, like efficiency and technology standards, economic instruments (e.g., carbon pricing, subsidies) (Bertram et al. 2015; Martin and Saikawa 2017) and other policies, such as government interventions to provide infrastructure, information policies, and voluntary actions by non-government actors (Somanathan et al. 2014). In recent years, regulatory instruments to promote low-carbon infrastructure have gained traction in developing countries (Finon 2019). The choice of policies has depended on institutional capacities, technological maturity and other developmental priorities of governments. For example, governments have favoured regulatory instruments over economic instruments when there has been sufficient institutional capacity to implement and monitor the regulations and standards (Hughes and Urpelainen 2015). Furthermore, institutional capacity has also determined the extent of implemented measures (Adenle et al. 2017). Market conditions and technological maturity are other important determinants of policy mixes being deployed in the energy sector. For example, subsidies for mitigation like feed-in-tariffs have worked best when the technologies are in nascent stages of development (Gupta et al. 2019a).

On the other hand, market-based instruments like emissions rading schemes (ETS) and auctions coupled with a regulatory framework have been a favourable strategy for more mature technologies (Polzin et al. 2015; Kitzing et al. 2018). FIT, tax incentives, and renewable portfolio standards – despite potentially substantial programme costs (Andor and Voss 2016; Abrell et al. 2019) – have played a significant role in attracting foreign direct investments in the renewable sector (Wall et al. 2019). Subsidies and carbon pricing have also played an important role in mainstreaming these renewable energy sources (Best and Burke 2018). Recently, subsidy-free investments in renewables, such as wind offshore (Jansen et al. 2020), backed by power purchase agreements, have gained momentum (Frankfurt School-UNEP Centre and BNEF 2020). Similar considerations apply for policy mixes targeted to other sectors – for example, transport and buildings.

The role of carbon pricing is still limited though increasing. Different measures have been suggested to improve the performance of the ETS, such as ‘price floors and caps’ and other carbon pricing schemes (Campiglio 2016; Bataille et al. 2018; Goulder and Morgenstern 2018). In 2020, 61 regional, national and sub-national carbon pricing instruments, representing 22% of the global GHG emissions, were in action or scheduled for implementation (World Bank 2019). Over 51% of emissions covered are priced at less than USD10 per tCO2-eq. At present, however, only 5% of the global emissions covered under carbon pricing initiatives are consistent with the range of carbon prices that have been suggested as needed to limit warming to well below 2°C (Stiglitz and Stern 2017). Most of the carbon pricing schemes have taken place in the OECD countries. The limited application of carbon pricing instruments in developing, and emerging economies may be due to political economy constraints (Campiglio 2016; Finon 2019). Carbon pricing had a sizeable impact on emissions – for example, the EU ETS impacts emissions from electricity in Germany (Schäfer 2019) and manufacturing in France (Colmer et al. 2020), respectively. Emissions reductions could be increased with higher carbon prices and without free allocation of allowances.

In the absence of a global comprehensive carbon price, regional regulatory policies for fossil fuels supply and key demand sectors like transport, industry and buildings (Chapters 9–11), coupled with regional carbon pricing instruments, were implemented to help initiate the climate actions consistent with the Paris Agreement (Kriegler et al. 2018). However, differences in the stringency of climate regulation have triggered fear that regulation reduces the competitiveness of industries in regulated countries and leads to industry relocation and ‘carbon leakage‘ (Schenker et al. 2018). In recent years, however, there is little evidence of carbon leakage (Naegele and Zaklan 2019; Schäfer 2019), and even positive effects of carbon pricing on efficiency have been observed (e.g., Löschel et al. 2019, for German manufacturing firms, and Germeshausen 2020 for German power plants). However, with asymmetric rising carbon prices, discussions about specific policy mechanisms to address carbon leakage like carbon border adjustments (Cosbey et al. 2019) were amplified. Furthermore, multiple policies – often implemented by different governmental levels (national vs sub-national) – interacted with each other and thereby affected their environmental and economic effectiveness. Recent examples include interactions of ETS with renewable support policies (e.g. Boehringer and Behrens 2015; Del Rio 2017), energy efficiency policies (e.g. Wiese et al. 2018) or electricity market reform (e.g. Teng et al. 2017), respectively.

Apart from explicit carbon pricing, various implicit carbon pricing mechanisms, such as fossil fuel taxes and removal of fossil fuel subsidies (Box 6.3) and regulatory instruments, are used by many countries as part of their climate policies. In addition, public provision and procurement of low-carbon infrastructure and technologies such as energy-efficient devices, renewable energy, and upgrades in electricity grids through state-sponsored institutions and public-private partnerships have played an important role in low-carbon development (e.g., Baron 2016).

Box 6.3 | Energy Subsidies

Energy subsidies continue to be widely applied. Global fossil fuel subsidies represent more than half of total energy subsidies with predominantly adverse environmental, economic, and social effects ( high confidence).

Energy subsidies can be defined as policy measures in the energy sector to lower the prices for consumers, raise the prices for producers, or reduce energy production costs (IEA 1999). There are subsidies for fossil fuels, renewables, and energy efficiency measures. The majority of the renewable subsidies are generation-based incentives for solar, wind or biomass in the form of feed-in-tariffs (Chapter 13), with total annual renewable subsidy estimates of about USD150 billion yr –1 globally (IEA 2018b). Estimates of fossil fuel subsidies can vary by an order of magnitude. For the year 2017, the IEA estimated fossil fuel subsidies of USD300 billion using IEA’s pre-tax, price-gap method (IEA 2018b), while the International Monetary Fund (IMF) included unpriced externalities in calculating subsidies of USD5.2 trillion or 6.5% of global GDP (Coady et al. 2017, 2019; World Bank 2019). It has been estimated that the amount spent on fossil fuel subsidies was around double the amount of subsidies spent on renewables (IEA 2018b). There are adverse environmental, economic and social consequences of fossil fuel subsidies (Rentschler and Bazilian 2017). More than 75% of the distortions created by fossil fuel subsidies are domestic, and studies indicate that reforming them can have substantial in-country benefits (Coady et al. 2017, 2019). Some of the G20 countries have implemented subsidy reforms based on low oil prices (Jewell et al. 2018).

Fossil fuel subsidies most commonly pursue non-climate objectives, for example, enhanced access to energy sources ( high confidence). In some cases, these energy access subsidies have helped extend modern energy sources to the poor (Kimemia and Annegarn 2016) and thereby contribute to SDG 7. However, the subsidies have proven to be regressive in most cases, with little benefit reaching the poor (Lockwood 2015). For example, Indonesia has introduced LPG subsidies for cooking. The kerosene-to-LPG conversion programme (‘Zero Kero’) was launched in 2007 and provided mainly households with free initial LPG equipment and LPG at a low subsidised price (Imelda et al. 2018 b; Thoday et al. 2018). Besides the national government, provincial governments and industry played a crucial role in implementation. Overall, the LPG conversion programme in Indonesia reduced cooking kerosene use (Andadari et al. 2014; Imelda et al. 2018 b) and GHG emissions (Permadi et al. 2017) with positive health effects (Imelda et al. 2018 b; Thoday et al. 2018). However, the programme is generally viewed as regressive and has failed to reduce traditional solid fuel use (Andadari et al. 2014; Toft 2016; Thoday et al. 2018). Furthermore, even if the programme decreased GHG emissions relative to continued kerosene use, these subsidies are still targeted at fossil fuels and contribute to GHG emissions.

India started a large LPG programme in 2015 that provided a capital cost subsidy to poor households (e.g., Gould 2018; Jose et al. 2018; Kar et al. 2019). While the programme has increased adoption of LPG in India (e.g., Sharma et al. 2019), it has not yet achieved a sustained use of LPG and replacement of solid fuels for cooking, amplifying the need for complementary policy measures (Gould 2018; Kar et al. 2019; Mani et al. 2020). The climate impacts of switching from biomass to LPG depend on the degree of biomass combustion in stoves and the extent to which biomass originates from non-renewable sources (Singh and Rao 2015; Jose et al. 2018). Barriers to increasing LPG use for cooking further included abundance of solid fuels at zero (monetary) costs (Mani et al. 2020) as well as benefits of solid fuels, such as maintaining the traditional taste of food and space heating in colder seasons (Gould 2018; Sharma et al. 2020).

6.4Mitigation Options

6.4.1Elements of Characterisation

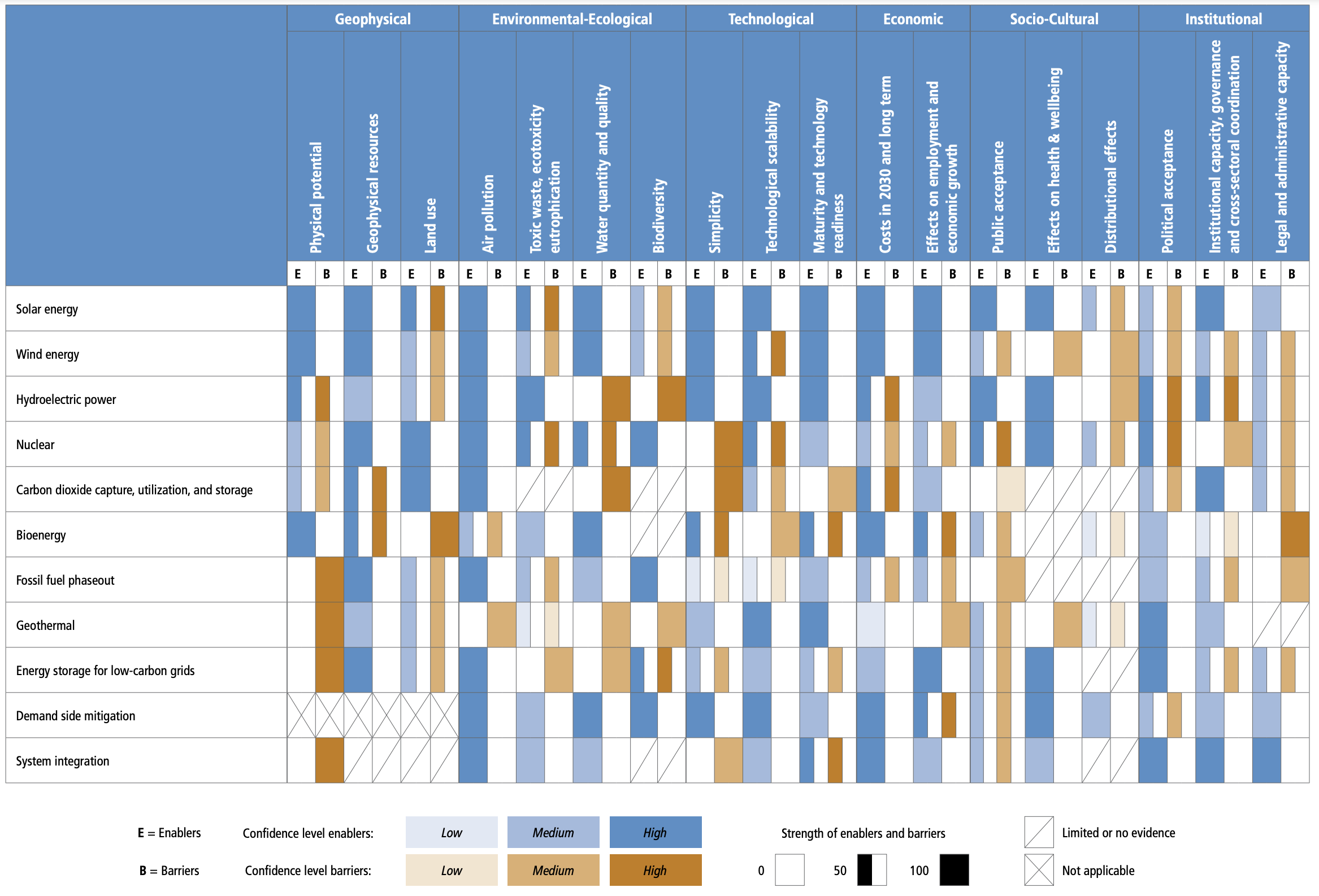

This section characterises energy system mitigation options and discusses which factors enable and inhibit their implementation. We touch on a broad range of factors that may enable and inhibit the implementation of mitigation options by considering six dimensions that affect their feasibility (Table 6.1 and Annex II.11). The assessment aims to identify which mitigation options can be readily implemented and which face barriers that would need to be overcome before they can be deployed at scale.

Table 6.1 | Dimensions and indicators to assess the barriers and enablers of implementing mitigation options in low-carbon energy systems.

Metric | Indicators |

Geophysical: Are the required resources available? | –Physical potential: physical constraints to implementation –Geophysical resources (including geological storage capacity): availability of resources needed for implementation –Land use: claims on land where an option would be implemented |

Environmental-ecological: What are the wider environmental and ecological impacts of the option? | –Air pollution: increase or decrease in air pollutants, such as NH4, CH4 and fine dust –Toxic waste, ecotoxicity and eutrophication –Water quantity and quality: changes in the amount of water available for other uses –Biodiversity: changes in conserved primary forest or grassland that affect biodiversity, and management to conserve and maintain land carbon stocks |

Technological: Can the required technology be upscaled soon? | – Simplicity: is the option technically simple to operate, maintain and integrate? –Technology scalability: can the option be scaled up technically? –Maturity and technology readiness: research and development (R&D) and time needed to implement the option |

Economic: What economic conditions can support or inhibit the implementation of the option? | –Costs in 2030 and in the long term: investment costs, costs in USD tCO2-eq –1 –Employment effects and economic growth: decrease or increase in jobs and economic welfare |

Socio-cultural: What social conditions could support or inhibit acceptance, adoption, and use of the option before 2030? | –Public acceptance: the extent to which the public supports the option and will change their behaviour accordingly –Effects on health and well-being –Distributional effects: equity and justice across groups, regions, and generations, including energy, water, and food security and poverty |

Institutional: What institutional conditions could support or inhibit the implementation of the option? | –Political acceptance: the extent to which politicians support the option –Institutional capacity and governance, cross-sectoral coordination: capability of institutions to implement and handle the option –Legal and administrative capacity |

6.4.2Energy Sources and Energy Conversion

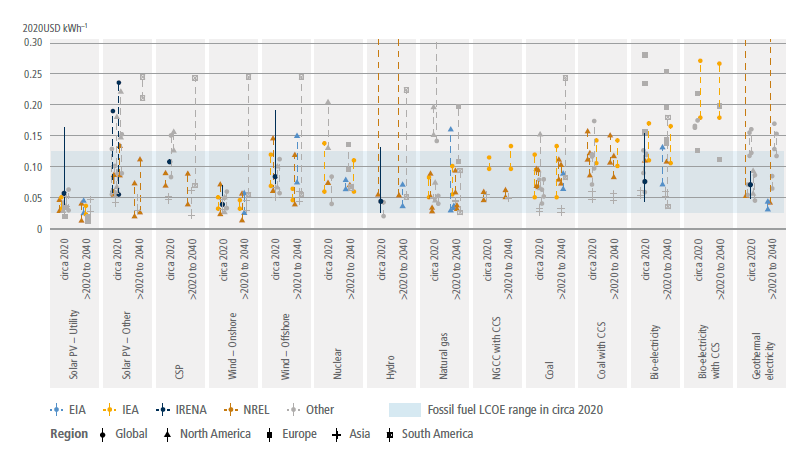

6.4.2.1 Solar Energy

Solar photovoltaic (PV) is increasingly competitive with other forms of electricity generation, and is the low-cost option in many applications ( high confidence). Costs have declined by 62% since 2015 ( high confidence) and are anticipated to decline by an additional 16% by 2030 if current trends continue (low confidence, medium evidence). Key areas for continued improvement are grid integration and non-module costs for rooftop systems ( high confidence). Most deployment is now utility-scale ( high confidence). Global future potential is not limited by solar irradiation, but by grid integration needed to address its variability, as well as access to finance, particularly in developing countries ( high confidence).

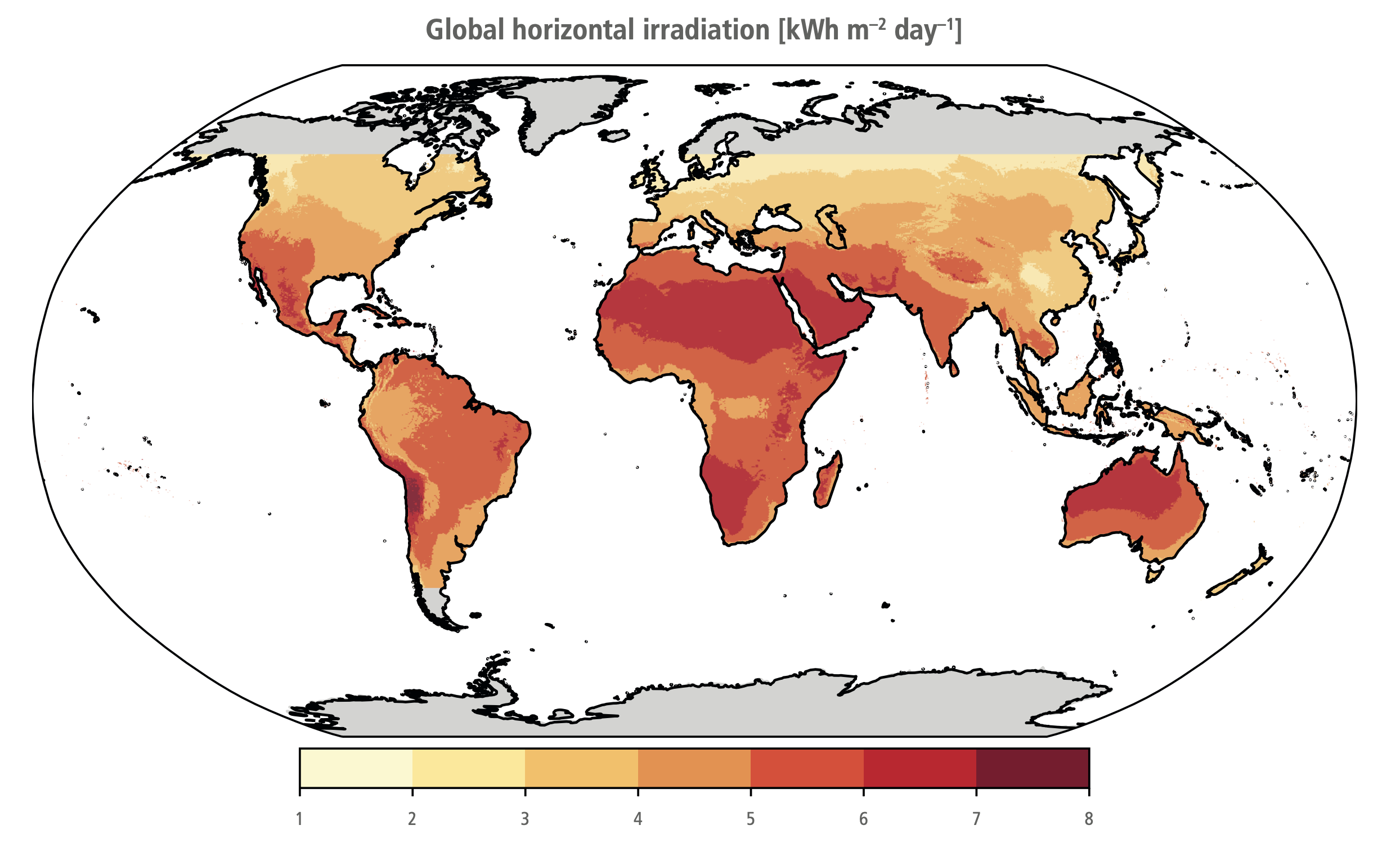

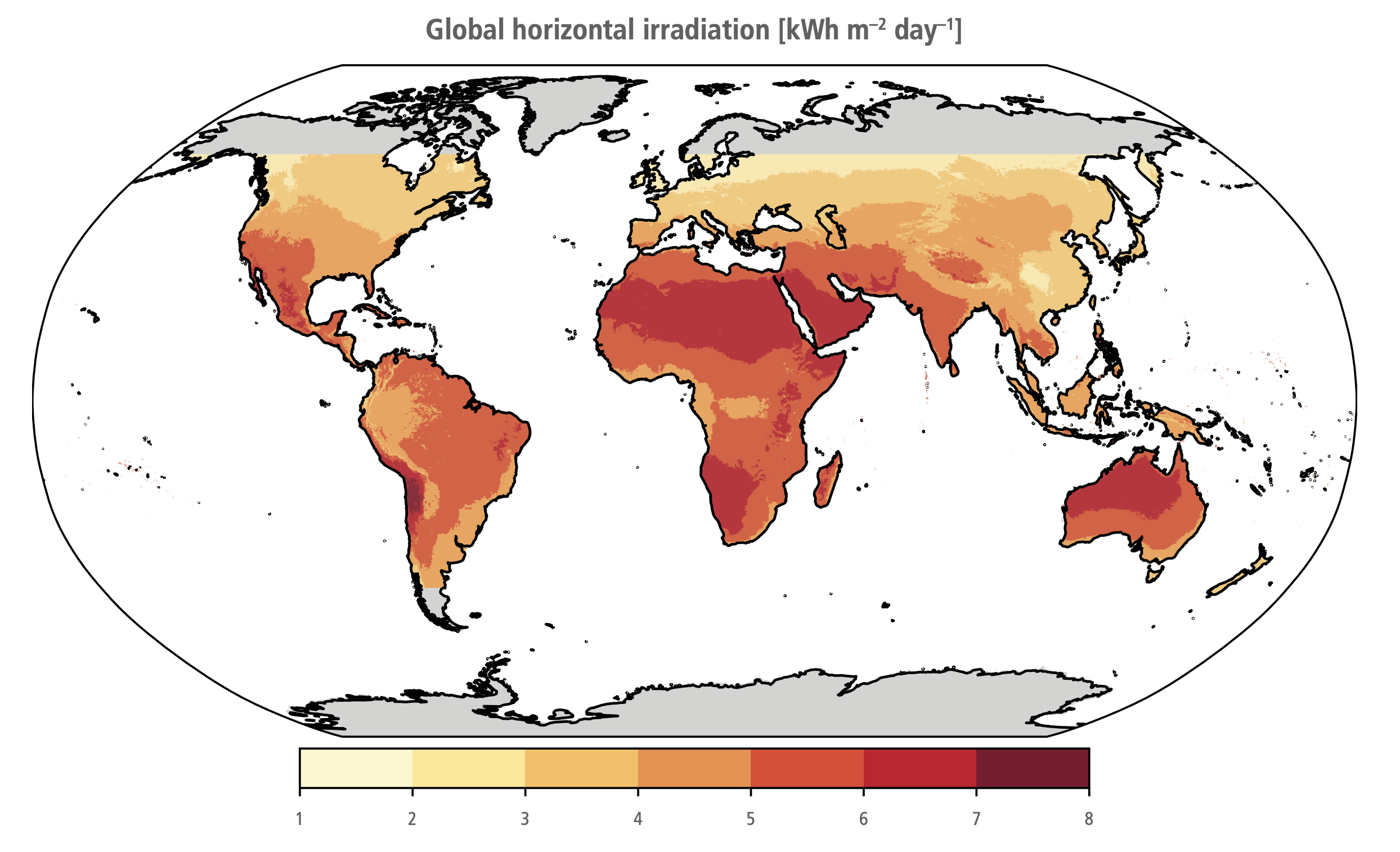

The global technical potential of direct solar energy far exceeds that of any other renewable energy resource and is well beyond the total amount of energy needed to support ambitious mitigation over the current century ( high confidence). Estimates of global solar resources have not changed since the IPCC’s Fifth Assessment Report (AR5) (Lewis 2007; Besharat et al. 2013) even as precision and near-term forecasting have improved (Diagne et al. 2013; Abreu et al. 2018). Approximately 120,000TW of sunlight reaches the Earth’s surface continuously, almost 10,000 times average world energy consumption; factoring in competition for land use leaves a technical potential of about 300 PWh yr –1 (1080 EJ yr –1) for solar PV, roughly double current consumption (Dupont et al. 2020). The technical potential for concentrating solar power (CSP) is estimated to be 45–82 PWh yr –1 (162–295 EJ yr –1) (Dupont et al. 2020). Areas with the highest solar irradiation are: western South America; northern, eastern and southwestern Africa; and the Middle East and Australia (Figure 6.7) (Prăvălie et al. 2019).

Figure 6.7 |Distribution of the daily mean global horizontal irradiation (GHI, kWh m–2day–1). Source: Global Solar Atlas (ESMAP 2019).

In many parts of the world, the cost of electricity from PV is below the cost of electricity generated from fossil fuels; in some, it is below the operating costs of electricity generated from fossil fuels ( high confidence). The weighted average cost of PV in 2019 was USD68 MWh –1, near the bottom of the range of fossil fuel prices (IRENA 2019b). The cost of electricity from PV has fallen by 89% since 2000 and 69% since AR5, at a rate of –16% per year. The 5:95 percentile range for PV in 2019 was USD52–190 MWh –1 (IRENA 2021b). Differences in solar insolation, financing costs, equipment acquisition, installation labour, and other sources of price dispersion explain this range (Nemet et al. 2016; Vartiainen et al. 2020) and scale. For example, in India, rooftop installations cost 41% more than utility-scale installations, and commercial-scale costs are 39% higher than utility-scale. Significant differences in regional cost persist (Kazhamiaka et al. 2017; Vartiainen et al. 2020), with particularly low prices in China, India, and parts of Europe. Globally, the range of global PV costs is quite similar to the range of coal and natural gas prices.

PV costs (Figure 6.8) have fallen for various reasons: lower silicon costs, automation, lower margins, automation, higher efficiency, and a variety of incremental improvements (Fu et al. 2018; Green 2019) (Chapter 16). Increasingly, the costs of PV electricity are concentrated in the installation and related ‘soft costs’ (marketing, permitting) associated with the technology rather than in the modules themselves, which now account for only 30% of installed costs of rooftop systems (O’Shaughnessy et al. 2019; IRENA 2021b). Financing costs are a significant barrier in developing countries (Ondraczek et al. 2015) and growth there depends on access to low-cost finance (Creutzig et al. 2017).

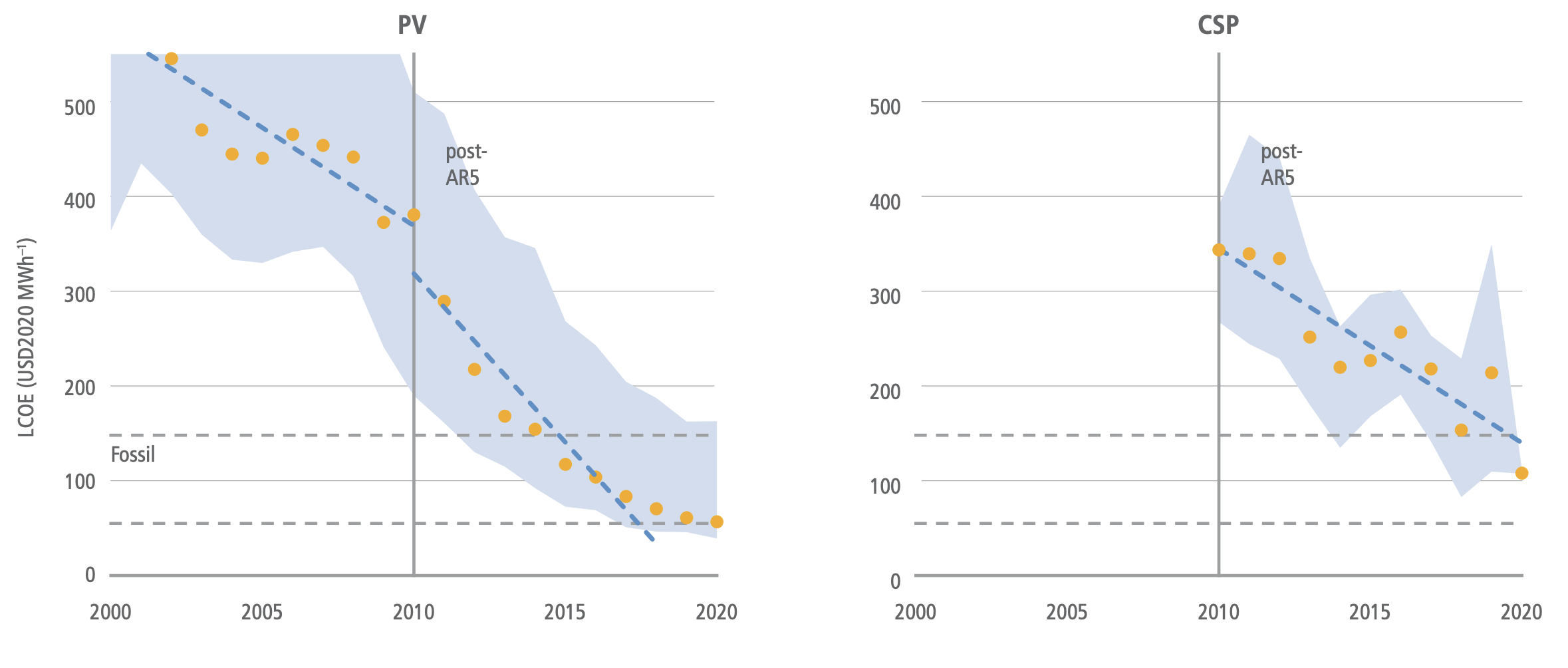

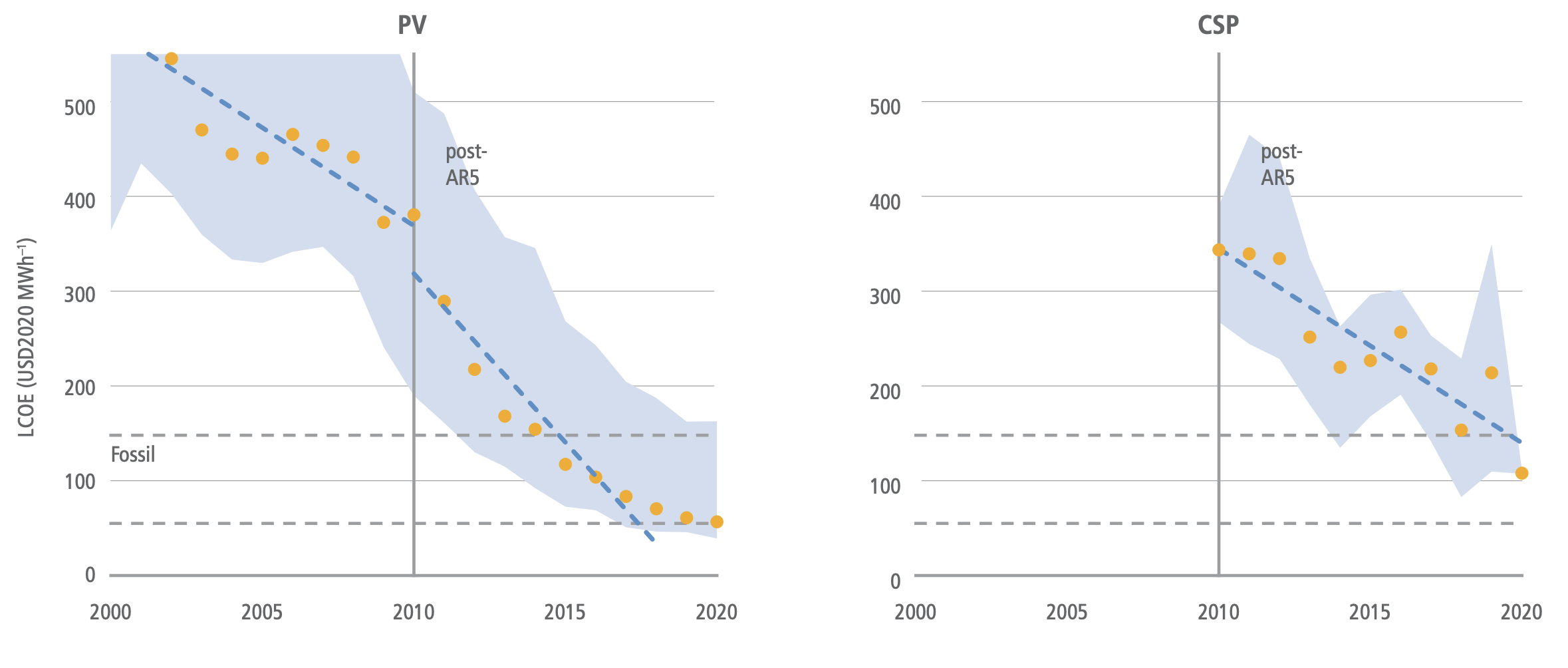

Figure 6.8 | Levelised costs of electricity (LCOE) of solar energy technologies 2000–2020. Range of fossil fuel LCOE indicated as dashed lines USD50–177 MWh –1. Linear fit lines were applied to data for AR4–AR5 and post-AR5 (2012). Yellow dots are capacity-weighted global averages for utility-scale installations. The blue area shows the range between the 5th and 95th percentile in each year. Data: IRENA (2021b).

CSP costs have also fallen, albeit at about half the rate of PV: –9% yr –1 since AR5. The lowest prices for CSP are now competitive with more expensive fossil fuels, although the average CSP cost is above the range for fossil-based power generation. Other data sources put recent CSP costs at USD120 MWh –1, in the middle of the fossil range (Lilliestam et al. 2020). Continuing the pace of change since AR5 will make CSP competitive with fossil fuels in sunny locations, although it will be difficult for CSP to compete with PV and even hybrid PV-battery systems. CSP electricity can be more valuable, however, because CSP systems can store heat longer than PV battery systems.

The share of total costs of PV-intensive electricity systems attributed to integration costs has been increasing but can be reduced by enhancing grid flexibility ( high confidence) (Sections 6.4.3 and 6.6, and Box 6.8). The total costs of PV include grid integration, which varies tremendously depending on PV’s share of electricity, other supply sources like wind, availability of storage, transmission capacity, and demand flexibility (Heptonstall and Gross 2020). Transmission costs can add USD1–10 MWh –1 or 3–33% to the cost of utility-scale PV (Gorman et al. 2019). Distributed (rooftop) PV involves a broader set of grid integration costs – including grid reinforcement, voltage balancing and control, and impacts on other generations – and has a larger range of integration costs from USD2–25 MWh –1, which is –3% to +37% (Hirth et al. 2015; Wu et al. 2015; Gorman et al. 2019). Other meta-analyses put the range at USD1–7 MWh –1 in the USA (Luckow et al. 2015.; Wiser et al. 2017), while a comprehensive study put the range at USD12–18 MWh –1 for up to 35% renewables and USD25–46 MWh –1 above 35% renewables (Heptonstall and Gross 2020). Increased system flexibility can reduce integration costs of solar energy (Wu et al. 2015) including storage, demand response, sector-coupling (Brown et al. 2018; Bogdanov et al. 2019), and increase complementarity between wind and solar (Heide et al. 2010) (Sections 6.4.3 and 6.4.4).

Since solar PV panels have very low operating costs, they can, at high penetrations and in the absence of adequate incentives to shift demand, depress prices in wholesale electricity markets, making it difficult to recoup investment, and potentially reducing incentives for new installations (Hirth 2013; Millstein et al. 2021). Continued cost reductions help address this issue of value deflation, but only partially. Comprehensive solutions depend on adding transmission and storage (Das et al. 2020) and, more fundamentally, adjustments to electricity market design (Roques and Finon 2017; Bistline and Young 2019).

The most important ways to minimise PV’s impact on the environment lie in recycling materials at end of life and making smart land-use decisions (medium confidence). A comprehensive assessment of PV’s environmental impacts requires lifecycle analysis (LCA) of resource depletion, land-use, ecotoxicity, eutrophication, acidification, ozone, and particulates, among other things (Mahmud et al. 2018). LCA studies show that solar PVs produce far less CO2 per unit of electricity than fossil generation, but PV CO2 emissions vary due to the carbon intensity of manufacturing energy and offset electricity (Grant and Hicks 2020). Concerns about systemic impacts, such as reducing the Earth’s albedo by covering surfaces with dark panels, have shown to be trivial compared to the mitigation benefits (Nemet 2009) (Box 6.7). Even though GHG LCA estimates span a considerable range of 9–250 gCO2 kWh –1 (de Wild-Scholten 2013; Kommalapati et al. 2017), recent studies that reflect higher efficiencies and manufacturing improvements find lower lifecycle emissions, including a range of 18–60 gCO2 kWh –1 (Wetzel and Borchers 2015) and central estimates of 80 gCO2 kWh –1 (Hou et al. 2016), 50 gCO2 kWh –1 (Nugent and Sovacool 2014), and 20 gCO2 kWh –1 (Louwen et al. 2016). These recent values are an order of magnitude lower than coal, and natural gas and further decarbonisation of the energy system will make them lower still. Thin films and organics produce half the lifecycle emissions of silicon wafer PV, mainly because they use less material (Lizin et al. 2013; Hou et al. 2016). Novel materials promise even lower environmental impacts, especially with improvements to their performance ratios and reliability (Gong et al. 2015; Muteri et al. 2020). Higher efficiencies, longer lifetimes, sunny locations, less carbon-intensive manufacturing inputs, and shifting to thin films could reduce future lifecycle impacts.

Another environmental concern with large PV power plants is the conversion of land to collect solar energy (Hernandez et al. 2015). Approximately 2 hectares of land are needed for 1 MW of solar electricity capacity (Perpiña Castillo et al. 2016; Kabir et al. 2018); at 20% efficiency, a square of PV panels of 550 km by 550 km, comprising 0.2% of Earth’s land area, could meet global energy demand. Land conversion can have local impacts, especially near cities and where land used for solar competes with alternative uses, such as agriculture. Large installations can also adversely impact biodiversity (Hernandez et al. 2014), especially where the above-ground vegetation is cleared and soils are typically graded. Landscape fragmentation creates barriers to the movement of species. However, a variety of means have emerged to mitigate land use issues. Substitution among renewables can reduce land conversion (Tröndle 2020). Solar can be integrated with other uses through ‘agrivoltaics’ (the use of land for both agriculture and solar production) (Dupraz et al. 2011) by, for example, using shade-tolerant crops (Dinesh and Pearce 2016). Combining solar and agriculture can also create income diversification, reduced drought stress, higher solar output due to radiative cooling, and other benefits (Elamri et al. 2018; Hassanpour Adeh et al. 2018; Barron-Gafford et al. 2019). PV installations floating on water also avoid land-use conflicts (Sahu et al. 2016; Lee et al. 2020), as does dual-use infrastructure, such as landfills (Jäger-Waldau 2020) and reservoirs where evaporation can also be reduced (Farfan and Breyer 2018).

Material demand for PV will likely increase substantially to limit warming to well below 2°C, but PV materials are widely available, have possible substitutes, and can be recycled (medium confidence) (Box 6.4). The primary materials for PV are silicon, copper, glass, aluminium, and silver – the costliest being silicon, and glass being the most essential by mass, at 70%. None of these materials is considered to be either critical or potentially scarce (IEA 2020e). Thin-film cells, such as amorphous silicon, cadmium telluride and copper indium gallium diselenide (CIGS), use far less material (though they use more glass), but account for less than 10% of the global solar market. Other thin-films, such as those based on perovskites, organic solar cells, or earth-abundant, non-toxic materials such as kesterites, either on their own, or layered on silicon, could further reduce material use per energy produced (Box 6.4).

After a typical lifetime of 30 years of use, PV modules can be recycled to prevent environmental contamination from the toxic materials within them, reusing valuable materials and avoiding waste accumulation. Recycling allows the reuse of nearly all – 83% in one study – of the components of PV modules, other than plastics (Ardente et al. 2019) and would add less than 1% to lifecycle GHG emissions (Latunussa et al. 2016). Glass accounts for 70% of the mass of a solar cell and is relatively easy to recycle. Recycling technology is advancing, but the scale and share of recycling is still small (Li et al. 2020d). By 2050, however, end-of-life PV could total 80 MT and comprise 10% of global electronic waste (Stolz and Frischknecht 2017), although most of it is glass. IEA runs a programme to enable PV recycling by sharing best practices to minimise recycling lifecycle impacts. Ensuring that a substantial amount of panels are recycled at end of life will likely require policy incentives, as the market value of the recovered materials, aside from aluminium and copper, is likely to be too low to justify recycling on its own (Deng et al. 2019). A near-term priority is maximising the recovery of silver, silicon, and aluminium, the most valuable PV material components (Heath et al. 2020).